Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690976

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690976

Europe Edible Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 266 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

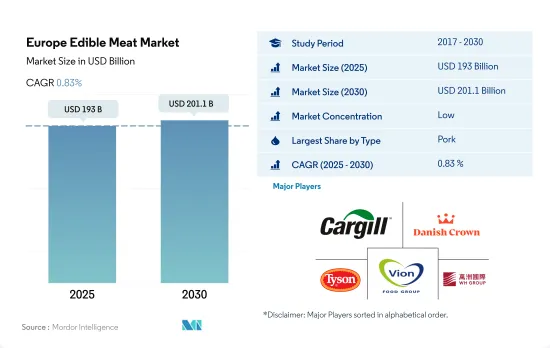

The Europe Edible Meat Market size is estimated at 193 billion USD in 2025, and is expected to reach 201.1 billion USD by 2030, growing at a CAGR of 0.83% during the forecast period (2025-2030).

The rise in demand for ready-to-eat meat favors the market

- Pork is the major type of meat consumed in Europe, and the sales of pork increased by 1.57% in 2022 compared to the previous year. In 2021, the European pork meat market experienced a major trend related to rising output. EU market leaders continuing to expand production are Spain, Denmark, and the Netherlands. The supply of pork in Europe was significantly greater than the demand in 2022. As a result, pork consumption increased across Europe, particularly in the south. However, lower carcass prices and the threat of additional African Swine Fever (ASF) outbreaks in Central Europe may hamper the growth of the market in the future.

- Beef consumption is mainly driven by the demand for ready-to-eat meat products across Europe. In Europe, the demand for processed beef is rising due to increased demand for convenient food like sandwiches, beef sticks, bacon, beef jerky, and pork rinds. Processed beef is projected to register a CAGR value of 1.68% during the forecast period. BRF SA, Cargill Inc., Danish Crown Amba, and Tyson Foods Inc. are the key players that offer processed beef in Europe.

- Mutton is the fastest-growing segment of meat in the region, and it is projected to record a CAGR value of 0.91% during the forecast period. There are over 70 million sheep and goats in the European Union (85% sheep and 15% goats). Greece, Spain, France, and Romania are the major mutton-producing areas in Europe. Around 20% of the mutton that is consumed in the region is imported. New Zealand supplies around 89% of the mutton requirement in all other European countries. The meat from lamb (sheep meat, less than one year) is more popular than regular mutton (sheep meat, less than three years) in Europe.

Poultry and pork meat consumption is driving the market

- Edible meat sales in Europe have seen stable growth over the years, increasing by 8.97% from 2018 to 2022. Russia, France, and Germany dominate the consumption trend. In 2022, these countries also dominated the livestock population count in the region, with Russia (18.56 million) leading the trend, followed by France (17.78 million), Germany (11.3 million), and Spain (6.63 million). Pork is the most consumed meat type in Europe.

- In Europe, Italy is the fastest-growing edible meat market. It is projected to register a CAGR of 1.20% by value during the forecast period. This increase was mainly due to the increased pork consumption in Italy. Italy accounted for about 41.96% by value of the pork market share in 2022 compared to other meat types. More than 70% of pigs grown in Italy are bred in the north, while 74% of farms in the center-south are in the industry due to the small size of the farms. The pork industry also increasingly utilizes data analytics and blockchain technology, utilizing sensors to enhance traceability, transparency, and food safety.

- The European edible meat market is projected to record a value CAGR of 0.32% during the forecast period. The lower progression can be attributed to reduced meat consumption in European countries. Nearly 46% of Europeans reported eating less meat in 2022 than the previous year. However, some other countries are yet to catch up with this trend due to their food cultures. Some cultures believe that plant-based meat lacks adequate flavor and nutrition. They consider meat as a proper meal and a good source of nutrition. Some people also believe plant-based foods are too expensive, difficult to prepare, or visually less appealing.

Europe Edible Meat Market Trends

Despite the Russia-Ukraine conflict, Russia remains a major beef producer in the region

- In 2022, beef production in Europe declined by 0.98% compared to the previous year, owing to reduced pricing and herd reductions. Russia, France, and Germany accounted for roughly 40% of the beef produced in Europe. The European Commission has plans to use public intervention to support beef prices if the average market price of beef in an EU country or region drops below USD 2,416 per ton over a selected period. The European Commission may provide grants for private storage aid if there is a drop in average prices or a substantial change in production costs, another factor that causes significant changes in margins damaging to the industry. The EU also supports beef farmers through specific exemptions for producer organizations in the beef industry.

- Russia was the major beef producer in the region in 2022, with a share of 15.96% in 2022. This growth was facilitated by exceptional measures taken by the state to support the industry. Some of the measures include reimbursing livestock breeders for the costs of their production, purchasing young animals, technological modernization of facilities, and improving work in the field of livestock breeding. Producers are offered loans for the purchase of fodder, equipment, veterinary drugs, and the construction and modernization of livestock facilities.

- The Netherlands had the lowest production of 429,640 tons in 2022. The Dutch national cattle inventory has constantly declined in the last three years due to the exceeding EU pasture phosphate limits. In 2022, beef cattle numbers declined by 8.4% to 3,690,000 heads. The government has been trying to reduce emissions through a decrease in livestock farming, which negatively impacts the country's beef industry.

Increasing cost of feed and decline in slaughter of variants of cows are leading to price fluctuations of beef in the region

- During 2019-2022, the price of beef grew by 5.34% due to supply chain disruptions that caused a rise in wholesale beef prices while cattle prices remained low. The whole service sale of beef recovered due to a rise in foodservice sales, even of premium cuts, leading to a 3% rise in total consumption. In 2021, the decline in suckler cows, which are bred for terminal beef, by 245,000 heads (-2.3%) led to increasing beef prices. Inadequate facilities, hygiene measures, and improper handling of the animals at the slaughterhouses further aggravate the microbial contamination of beef, which can result in the transmission of foodborne pathogens to humans

- The rising feed costs also contributed to the increase in beef prices by 26% during the first quarter of 2022. High input costs, particularly for feed, may result in additional slaughtering and lower carcass weights, primarily on intensive cattle farms where feed costs will have a greater impact on farm profitability. Due to the rising food and meat prices, the region's beef consumption decreased to 10.3 kg per capita in 2022 (-0.3%). This trend was likely to continue in 2022, reaching -0.9% in the overall context.

- Owing to very high food price inflation during 2021-2023 in Europe, consumer demand for meat has been consistently declining, coupled with higher awareness about individual health and the environment. Due to the high prices and declining demand, beef production across many countries in Europe observed a decline. For instance, in 2022, Italy saw a production slump of 20%, followed by Spain and Germany reporting falls of 6% and 1%, respectively. France recorded a 1% increase in production, while the Netherlands recorded an increase in beef production by 9%.

Europe Edible Meat Industry Overview

The Europe Edible Meat Market is fragmented, with the top five companies occupying 10.15%. The major players in this market are Cargill Inc., Danish Crown AmbA, Tyson Foods Inc., Vion Group and WH Group Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90079

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Beef

- 3.1.2 Mutton

- 3.1.3 Pork

- 3.1.4 Poultry

- 3.2 Production Trends

- 3.2.1 Beef

- 3.2.2 Mutton

- 3.2.3 Pork

- 3.2.4 Poultry

- 3.3 Regulatory Framework

- 3.3.1 France

- 3.3.2 Germany

- 3.3.3 Italy

- 3.3.4 United Kingdom

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Type

- 4.1.1 Beef

- 4.1.2 Mutton

- 4.1.3 Pork

- 4.1.4 Poultry

- 4.1.5 Other Meat

- 4.2 Form

- 4.2.1 Canned

- 4.2.2 Fresh / Chilled

- 4.2.3 Frozen

- 4.2.4 Processed

- 4.3 Distribution Channel

- 4.3.1 Off-Trade

- 4.3.1.1 Convenience Stores

- 4.3.1.2 Online Channel

- 4.3.1.3 Supermarkets and Hypermarkets

- 4.3.1.4 Others

- 4.3.2 On-Trade

- 4.3.1 Off-Trade

- 4.4 Country

- 4.4.1 France

- 4.4.2 Germany

- 4.4.3 Italy

- 4.4.4 Netherlands

- 4.4.5 Russia

- 4.4.6 Spain

- 4.4.7 United Kingdom

- 4.4.8 Rest of Europe

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 BRF S.A.

- 5.4.2 Cargill Inc.

- 5.4.3 Danish Crown AmbA

- 5.4.4 Dawn Meats

- 5.4.5 Gruppa Cherkizovo, PAO

- 5.4.6 Heck! Food Ltd

- 5.4.7 Hormel Foods Corporation

- 5.4.8 JBS SA

- 5.4.9 Mitsubishi Corporation

- 5.4.10 NH Foods Ltd

- 5.4.11 Nomad Foods Limited

- 5.4.12 Tyson Foods Inc.

- 5.4.13 Vion Group

- 5.4.14 WH Group Limited

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.