Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636481

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636481

China Electric Vehicle Battery Manufacturing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 95 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

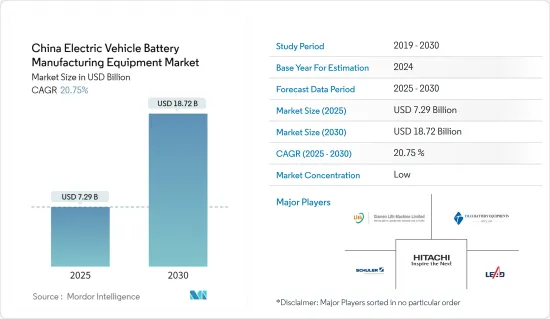

The China Electric Vehicle Battery Manufacturing Equipment Market size is estimated at USD 7.29 billion in 2025, and is expected to reach USD 18.72 billion by 2030, at a CAGR of 20.75% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, government policies and investments towards battery manufacturing, and a decline in the cost of battery raw materials, especially lithium-ion, are expected to drive the market in the forecast period.

- On the other hand, other countries striving to establish manufacturing facilities are expected to hamper the market in the future.

- Nevertheless, long-term ambitious targets for electric vehicles in China are expected to create a significant opportunity in the forecast period.

China Electric Vehicle Battery Manufacturing Equipment Market Trends

Lithium-ion Battery is Expected to have a Major Share

- Lithium-ion battery manufacturing equipment includes specialized machines and tools tailored for producing lithium-ion batteries. China stands as a global frontrunner in lithium-ion battery production, hosting a multitude of companies that manufacture a diverse array of industry-specific equipment. Bolstered by robust infrastructure, governmental backing, and a wealth of expertise, China has solidified its status as a central hub for lithium-ion battery production.

- Moreover, due to technological advancements and economies of scale, lithium-ion battery packs are becoming more affordable in China, leading to a rise in electric vehicle (EV) demand. As EVs become more accessible, the parallel surge in demand for lithium-ion battery manufacturing equipment becomes evident.

- In 2023, lithium-ion battery pack prices dropped by 14% from the previous year, settling at USD 139/kWh. Beyond these market dynamics, ongoing research and development efforts aim to create more efficient lithium battery materials for EVs, further amplifying the demand for battery manufacturing equipment.

- Moreover, as technology advances, EV battery manufacturers are crafting superior lithium-ion batteries, intensifying the need for advanced EV battery manufacturing equipment.

- For example, in April 2024, CATL, a prominent Chinese EV battery manufacturer, introduced its cutting-edge lithium iron phosphate battery, achieving a remarkable driving range exceeding 1,000 kilometers on a single charge. Such breakthroughs are poised to bolster the demand for lithium-ion battery manufacturing equipment.

- Additionally, in May 2024, CATL, in collaboration with six other firms, announced a substantial investment of nearly USD 845 million aimed at developing all-solid-state batteries (ASSBs), a next-gen evolution of conventional lithium-ion batteries, set to power future EVs.

- Given the declining prices and continuous innovations in EV lithium-ion batteries, this segment is projected to command a significant share in the coming years.

Government Policies and Investments Towards Battery Manufacturing is Expected to Drive the Market

- China's EV battery manufacturing equipment market is propelled by supportive government policies and substantial investments in battery production. The government provides direct financial support, tax incentives, and subsidies, effectively lowering costs for manufacturers and promoting investments in cutting-edge equipment.

- National initiatives, such as "Made in China 2025" and the New Energy Vehicle mandate, champion the growth of high-tech sectors, notably battery technology, thus fueling the demand for specialized manufacturing tools. Moreover, the nation is channeling investments into pioneering battery technologies for electric vehicles.

- For example, in May 2024, China unveiled plans to invest USD 845 million into next-gen battery tech for EVs. Notably, six firms, including CATL, alongside major automakers BYD and Geely, are poised to benefit from government support in developing all-solid-state batteries.

- Additionally, surging EV sales are prompting battery manufacturers to ramp up investments, further driving the demand for EV battery manufacturing tools. The International Energy Agency reported that in 2023, China's EV car sales reached 8.1 million, a jump from 5.9 million in 2022. As the nation accelerates its EV production and bolsters investments in battery manufacturing, the demand for related equipment is projected to rise.

- China holds a commanding position in the global EV landscape, representing 69% of new EV sales in December 2023, with an optimistic growth trajectory ahead. The previous year witnessed a 37% surge in sales, totaling around 9 million new EVs and capturing a 34% market share. Furthermore, the nation has revised its EV penetration ambitions, targeting a 45% market share by 2027, up from the earlier goal of 40% by 2030.

- In conclusion, with robust government backing and strategic investments in battery production, the market is poised for continued growth.

China Electric Vehicle Battery Manufacturing Equipment Industry Overview

The china electric vehicle battery manufacturing equipment market is semi-fragmented. Some of the major players in the market (in no particular order) include Xiamen Lith Machine Limited, Wuxi Lead Intelligent Equipment Co Ltd, Schuler AG, Hitachi Ltd, and Xiamen Tmax Battery Equipments Limited., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50003749

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Policies and Investments Towards Battery Manufacturing

- 4.5.1.2 Decline in Cost of Battery Raw Materials

- 4.5.2 Restraints

- 4.5.2.1 Other Countries Striving Towards Establishing Manufacturing Facilities

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Process

- 5.1.1 Mixing

- 5.1.2 Coating

- 5.1.3 Calendering

- 5.1.4 Slitting and Electrode Making

- 5.1.5 Other Process

- 5.2 Battery

- 5.2.1 Lithium-ion

- 5.2.2 Lead-Acid

- 5.2.3 Nickel Metal Hydride Battery

- 5.2.4 Other Batteries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Xiamen Lith Machine Limited

- 6.3.2 Wuxi Lead Intelligent Equipment Co Ltd

- 6.3.3 Schuler AG

- 6.3.4 Hitachi Ltd

- 6.3.5 Xiamen Tmax Battery Equipments Limited

- 6.3.6 Durr AG

- 6.3.7 Xiamen ACEY New Energy Technology

- 6.3.8 Xiamen TOB New Energy Technology Co., Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Long-term ambitious targets for electric vehicles

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.