Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636467

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636467

China Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 95 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

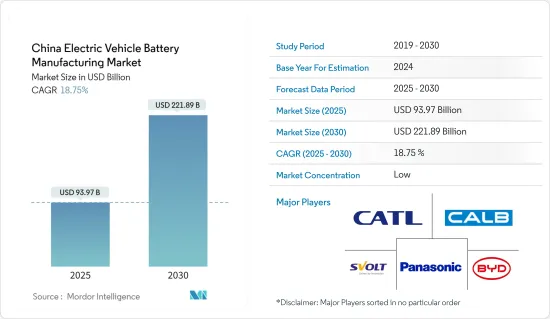

The China Electric Vehicle Battery Manufacturing Market size is estimated at USD 93.97 billion in 2025, and is expected to reach USD 221.89 billion by 2030, at a CAGR of 18.75% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as investments to enhance the battery production capacity and a decline in the cost of battery raw materials are expected to be among the most significant drivers for the China Electric Vehicle Battery Manufacturing Market during the forecast period.

- On the other hand, import dependency for key battery materials leaves the industry vulnerable to price fluctuations and imbalanced development. This poses a threat to the China Electric Vehicle Battery Manufacturing Market during the forecast period.

- Nevertheless, continued Long-term ambitious targets for electric vehicles. This factor is expected to create several opportunities for the market in the future.

China Electric Vehicle Battery Manufacturing Market Trends

Lithium-ion Battery Type to Dominate the Market

- Li-ion batteries, known for their high energy density and long life cycles, have become the go-to choice for EV manufacturers. This technology not only ensures the production of efficient electric vehicles but also meets both consumer expectations and industry benchmarks.

- To bolster EV adoption and domestic battery production, the Chinese government has rolled out a series of robust policies. Initiatives like the New Energy Vehicle (NEV) mandate, alongside subsidies and tax incentives, are fueling the rapid expansion of the EV sector. Furthermore, the "Made in China 2025" initiative underscores China's ambition to cement its status as a global frontrunner in advanced manufacturing.

- China's drive to cut carbon emissions and tackle air pollution is a pivotal force behind its booming EV market. With policies championing clean energy vehicles, the nation is witnessing a swift transition from internal combustion engines to electric mobility. As the globe's largest EV market, China's surging demand is propelled by urbanization, heightened environmental consciousness, and stringent vehicle emission regulations, all of which amplify the need for domestically produced batteries.

- In May 2024, China is set to channel approximately CNY 6 billion (USD 845 million) into pioneering next-generation battery technologies for electric vehicles (EVs). All Solid State Batteries (ASSBs), a cutting-edge advancement over traditional lithium-ion batteries (LIBs), utilize a solid conductive electrolyte, enhancing safety and energy density. Recognizing their potential, EV battery titan CATL is poised to receive government backing for this technological leap.

- China's expansive charging infrastructure development is pivotal for the country's electric vehicle adoption. This strategic investment guarantees EV users easy access to efficient charging solutions, further amplifying the demand for EV batteries. Concurrently, Chinese firms are pouring resources into R&D, aiming to refine battery technologies and curtail production costs. Collaborations with international tech giants and research entities are catalyzing innovations in battery manufacturing.

- For example, in May 2024, state-owned SAIC announced plans to integrate full solid-state batteries into its EV brands by 2025, with mass production slated for 2026. Boasting an energy density exceeding 400Wh/kg, this battery promises a driving range of at least 1,000km. Last June, domestic EV maker Nio successfully tested a solid-state battery achieving a 360Wh/kg energy density and a remarkable 1,044km range. Additionally, IM Motors, partially owned by SAIC, revealed in April its IM L6 EV model, featuring an ultra-fast charging solid-state battery with 130kWh power, supporting a 1,000km range and 900V ultra-fast charging capability.

- China dominates the global battery landscape, boasting a manufacturing capacity nearing 900 gigawatt-hours, which translates to a commanding 77% share of the worldwide total. Furthermore, six of the top ten battery manufacturers globally hail from China. This dominance is further reinforced by China's holistic control over the entire EV supply chain, from metal mining to vehicle production. With more than half of the world's electric vehicle fleet residing in China, the nation's lithium-ion battery cell manufacturing capacity, recorded at 1705 GWh in 2023, is projected to skyrocket to 6197 GWh by 2027.

- Given these developments and investments, a surge in EV battery production across the region is anticipated, alongside a growing demand for lithium-ion batteries in the coming years.

Investments to Enhance the Battery Production Capacity

- China is strategically ramping up its battery manufacturing capacity to cater to the surging demand for electric vehicles (EVs). Government initiatives, including subsidies and investment incentives, are spurring domestic companies to bolster their production capabilities. This concerted effort seeks to cement China's status as a global frontrunner in EV battery manufacturing, guaranteeing a consistent supply of premium batteries for the expanding EV market.

- The establishment of new battery production plants throughout China is propelling the EV battery manufacturing market. Industry giants like CATL and BYD are rolling out cutting-edge facilities to amplify their production. These state-of-the-art plants, outfitted with advanced technologies, promise heightened output and efficiency-key factors in satisfying the surging domestic and international appetite for EV batteries.

- Floating tenders for slurry mixers play a pivotal role in refining the battery production process. These mixers ensure uniformity in battery material blending, directly influencing the quality and performance of lithium-ion batteries. By soliciting tenders for these crucial mixers, China is not only enhancing its battery manufacturing technology but also bolstering the overall growth and efficiency of the EV battery market, fueling the industry's swift expansion.

- For example, in June 2024, Gotion High-tech, a Chinese battery cell manufacturer, unveiled a groundbreaking electric vehicle battery capable of charging in under 10 minutes, positioning it as a formidable competitor to global leader CATL. This swift-charging innovation directly addresses consumer concerns about charging durations. Gotion has commenced mass production of its G-Current batteries, tailored for extended-range hybrids. Meanwhile, production lines for all-electric vehicle batteries are under construction, with mass production slated to kick off by year's end.

- China's government remains steadfast in its support for the EV sector, rolling out measures like tax incentives, subsidies for manufacturers and consumers, and bolstering charging infrastructure. Such initiatives aim to enhance the affordability and convenience of EVs, driving up adoption rates and, in turn, amplifying the demand for battery materials. Battery technology innovations are also reshaping the landscape. For instance, BYD is pioneering new chemistries like lithium iron phosphate (LFP) batteries-safer and more economical, albeit with a marginally lower energy density than conventional lithium-ion counterparts. These breakthroughs are pivotal in making EVs more accessible to the broader market.

- Looking ahead, China's EV battery manufacturing market is poised for a bullish trajectory. With unwavering government backing, technological strides, and strategic industry collaborations, China is set to uphold its dominance in the global EV arena. The relentless expansion of production capacities by leading battery manufacturers, coupled with a focus on sustainable practices, bodes well for a consistent demand for essential materials, propelling the swift ascent of the EV battery manufacturing sector.

- China's lithium-ion battery manufacturing capacity stands at a staggering 1.2 terawatt hours (TWh), commanding a robust 76 percent share of the global landscape. With more than half of the world's electric vehicles gracing Chinese roads, projections indicate this capacity will surge to 4.65 TWh by 2030.

- Such investments and production expansions are set to amplify the demand for lithium-ion battery capacity.

China Electric Vehicle Battery Manufacturing Industry Overview

The China Electric Vehicle Battery Manufacturing Market is semi-fragmented. Some of the key players in this market (in no particular order) are BYD Co. Ltd., Contemporary Amperex Technology Co. Limited, Panasonic Corporation, CALB (China Aviation Lithium Battery), and SVOLT Energy Technology.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50003734

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Investments to Enhance the battery production capacity

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 Import Dependency for Key Battery Material

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Nickel Metal Hydride Battery

- 5.1.4 Others

- 5.2 Battery Form

- 5.2.1 Prismatic

- 5.2.2 Pouch

- 5.2.3 Cylindrical

- 5.3 Vehicle

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Others

- 5.4 Propulsion

- 5.4.1 Battery Electric Vehicle

- 5.4.2 Hybrid Electric Vehicle

- 5.4.3 Plug-in Hybrid Electric Vehicle

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 EnerSys

- 6.3.4 GS Yuasa Corporation

- 6.3.5 LG Chem Ltd

- 6.3.6 Exide Industries

- 6.3.7 Panasonic Corporation

- 6.3.8 CALB (China Aviation Lithium Battery)

- 6.3.9 SVOLT Energy Technology

- 6.3.10 EVE Energy

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Long-term ambitious targets for electric vehicles

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.