Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636276

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636276

Germany Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 100 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

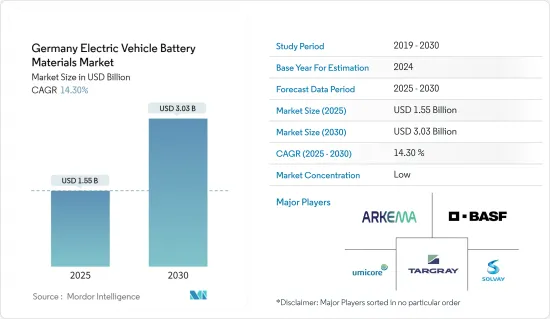

The Germany Electric Vehicle Battery Materials Market size is estimated at USD 1.55 billion in 2025, and is expected to reach USD 3.03 billion by 2030, at a CAGR of 14.3% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, growing electric vehicle (EV) sales and supportive government policies and regulations are expected to drive the demand for electric vehicle battery materials during the forecast period.

- On the other hand, issues related to the raw material supply chain and price fluctuations are likely to negatively impact the market studied.

- Nevertheless, technological advancements in batteries like higher energy density, faster charging times, improved safety, and longer lifespan are expected to create significant opportunities for electric vehicle battery materials market players in the near future.

Germany Electric Vehicle Battery Materials Market Trends

Growing Electric Vehicle (EVs) Sales Drives the Market

- Rising electric vehicle (EV) sales in Germany are driving up the demand for EV battery materials in the region. As the country sees a surge in EV sales, the need for key battery materials like lithium, cobalt, nickel, and graphite is also escalating. This heightened demand is spurring local production and investment in these materials, bolstering the growth of Germany's battery material supply chain.

- Germany is pivoting towards clean energy, with electric vehicles taking center stage. Over recent years, EV sales in the country have skyrocketed. For example, the International Energy Agency (IEA) reported that in 2023, Germany sold 0.7 million electric vehicles. While this figure remained steady from 2022, it marked a 5.5-fold increase from 2019. With numerous projects and initiatives recently unveiled by the European government, EV sales are poised for significant growth, further amplifying the demand for battery materials.

- The German government actively champions the EV market's expansion, offering subsidies, tax incentives, and enforcing stricter emission regulations. These supportive measures not only bolster the EV market but also extend to the battery material industry. Recently, the government unveiled ambitious incentives, aiming for a fourfold increase in EV sales in the coming years.

- As part of its 2023 initiatives, the government rolled out a substantial subsidy scheme to bolster electric vehicle adoption. New EV buyers were entitled to a subsidy of up to EUR 6,000 (approximately USD 6,500), while those opting for plug-in hybrids could avail up to EUR 4,500 (around USD 4,900). Such measures are anticipated to not only boost EV production and sales but also elevate the demand for battery materials in the years ahead.

- Germany's vibrant EV market is a hotbed for battery technology innovation. Major German corporations, alongside research institutions, are channeling investments into pioneering materials that promise enhanced energy density, extended lifespan, and superior safety. Collaborations among leading regional companies are paving the way for advanced battery technologies, setting the stage for heightened EV battery demand.

- In a notable development, a consortium of 15 companies and academic researchers, spearheaded by battery firm VARTA, unveiled a cutting-edge sodium-ion battery technology in May 2024. This next-gen battery promises high performance, cost-effectiveness, and environmental friendliness, catering to EVs and other applications. The consortium has earmarked mid-2027 for the project's culmination. Such breakthroughs are set to not only accelerate the demand for sophisticated EV batteries but also amplify the region's appetite for battery materials in the foreseeable future.

- Given these dynamics, the trajectory of EV demand and the corresponding surge in battery material requirements appear robust and promising.

Lithium-Ion Battery Type Dominate the Market

- The growing production of lithium-ion batteries for electric vehicles (EVs) is reshaping the battery materials market. In Germany, as lithium-ion battery production has surged, so too has the demand for lithium. Discoveries of lithium in the region are notably influencing raw material costs.

- Key market players are channeling investments into lithium reserves and R&D, aiming to boost lithium-ion battery production and meet the escalating demand for battery raw materials. As these reserves are continuously discovered, the prices of lithium-ion batteries have seen a downward trend over time.

- For instance, battery prices in 2023 fell to USD 139/kWh, marking a decline of over 13%. With ongoing technological innovations and manufacturing improvements, projections suggest battery pack prices could drop to USD 113/kWh by 2025 and further to USD 80/kWh by 2030.

- Moreover, European governments are actively championing lithium-ion battery production for EVs, spurred by mounting environmental concerns. With a keen focus on achieving net-zero carbon emissions, these governments have launched multiple initiatives to boost lithium-ion battery production, aiming to meet the region's growing EV demand.

- For instance, in January 2024, Northvolt, a Swedish lithium-ion battery manufacturer, secured EU approval for a significant EUR 902 million (USD 986.43 million) state aid package from Germany. This funding is earmarked for establishing an EV battery production facility in Heide, Germany. Such endorsements not only bolster Germany's efforts but also align with the broader EU's net-zero ambitions. These initiatives are poised to bolster the adoption of lithium-ion batteries as a clean energy solution, subsequently driving up the demand for battery materials in the years ahead.

- In recent years, Germany has emerged as a leader in pioneering advanced recycling technologies for lithium-ion batteries. Collaborations between companies and research institutions are focused on efficiently reclaiming valuable materials, including lithium, cobalt, and nickel, from spent batteries.

- For instance, in May 2024, Elemental Strategic Metals (ESM), a Polish entity, in collaboration with Ascend Elements, a US start-up, unveiled plans for a lithium-ion battery recycling facility. With a projected capacity of 25,000 tonnes annually, construction is set to commence in autumn 2024, aiming for operational status by 2026. Such endeavors are anticipated to boost raw material production and elevate the output of EV battery materials in the future.

- Given these developments, it's evident that ongoing projects and initiatives are set to bolster EV battery production and significantly heighten the demand for EV battery materials in the coming years.

Germany Electric Vehicle Battery Materials Industry Overview

Germany's electric vehicle battery materials market is semi-fragmented. Some key players (not in particular order) are Targray Technology International Inc., BASF SE, Arkema SA, Solvay SA, Umicore SA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50003563

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Raw Material Demand Supply Gap

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Targray Technology International Inc

- 6.3.2 BASF SE

- 6.3.3 Arkema SA

- 6.3.4 Solvay SA

- 6.3.5 Umicore SA

- 6.3.6 Mitsubishi Chemical Group Corporation

- 6.3.7 UBE Corporation

- 6.3.8 Johnson Matthey

- 6.3.9 Henkel Adhesive Technologies

- 6.3.10 Heraeus Group

- 6.3.11 Wacker Chemie AG

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.