Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636271

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636271

South America Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 110 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

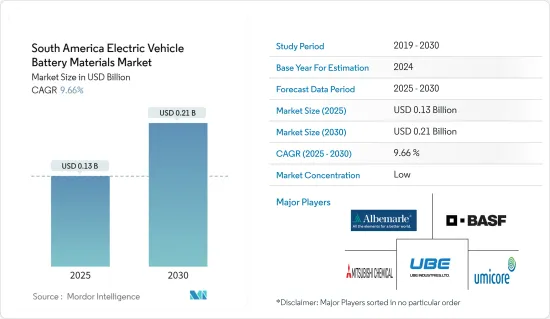

The South America Electric Vehicle Battery Materials Market size is estimated at USD 0.13 billion in 2025, and is expected to reach USD 0.21 billion by 2030, at a CAGR of 9.66% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising growth in electric vehicle sales and supportive government policies and regulations are expected to be among the most significant drivers for the South America Electric Vehicle Battery Materials Market during the forecast period.

- On the other hand, the lack of battery material production facilities, leading to heavy reliance on imports, poses a threat to the South America Electric Vehicle Battery Materials Market during the forecast period.

- Nevertheless, continued efforts are being made to develop advanced battery technology. This factor is expected to create several opportunities for the market in the future.

- Brazil is expected to witness significant growth and will likely register the highest growth during the forecast period. This is due to the presence of a significant vehicle manufacturing and sales industry in the region.

South America Electric Vehicle Battery Materials Market Trends

Lithium-ion Batteries to Dominate the Market

- The South American electric vehicle (EV) battery materials market hinges significantly on lithium-ion batteries. These batteries, being the most prevalent in the electric vehicle realm, stand out for their blend of energy density, efficiency, and durability, making them a linchpin in modern electric vehicle technology.

- Over the past decade, strides in battery technology and manufacturing have not only cut costs but also amplified performance and reliability, heightening the appeal of lithium-ion batteries to manufacturers and consumers.

- In recent years, there has been a downward trend in lithium-ion battery and cell pack prices, enhancing their allure to end-users. After a slight uptick in 2022, prices dipped again in 2023, with lithium-ion battery packs hitting a historic low of USD 139/kWh, marking a 14% drop.

- This battery segment comprises a range of materials, each playing a vital role in the battery's overall performance. These materials are selected for their ability to boost energy density, cycle life, and thermal stability, which are crucial factors for the automotive sector. Notably, nickel-rich cathode materials are favored for their high energy capacity, directly translating to extended driving ranges-a key selling point for consumers and market competitiveness.

- The region's growing electric vehicle appetite has triggered a surge in lithium-ion battery demand, prompting battery manufacturers to invest in material production facilities. This strategic shift aims to meet the rising demand for lithium batteries, both domestically and globally. Coupled with ongoing battery tech advancements, the market is poised for sustained growth as electric vehicle adoption climbs.

- For instance, in April 2023, China's BYD Co Ltd, the world's leading electric vehicle (EV) manufacturer, is set to construct a lithium cathode factory in Chile's Antofagasta region with an investment of USD 290 million. This announcement was made by Chile's economic development agency, CORFO. BYD Chile has been designated as a recognized lithium producer by the Chilean government, as confirmed by CORFO. This recognition grants the company privileged access to preferential rates for lithium carbonate allocations.

- Given these factors, the dominance of the lithium-ion battery segment in the market is projected for the forecast period.

Brazil to Witness Significant Growth

- Brazil plays a pivotal role in the South American electric vehicle (EV) battery materials market, leveraging its abundant natural resources and growing industrial capabilities. The country's vast reserves of critical battery materials, particularly lithium, nickel, and graphite, position it as a potential powerhouse in the regional and global supply chain for electric vehicle components.

- Brazil's lithium deposits, concentrated in the states of Minas Gerais and Ceara, have attracted significant attention from both domestic and international mining companies seeking to capitalize on the growing demand for this crucial battery metal.

- The Energy Institute Statistical Review of World Energy reported that in 2023, the country's lithium reserves stood at 4.9 thousand tonnes of lithium content. This marked a significant increase from the 2.6 thousand tonnes recorded in 2022, reflecting an impressive growth rate of 88.5%. Such a surge underscores the nation's substantial lithium reserves, a factor that bodes well for the burgeoning battery material market, especially in the context of electric vehicles.

- The country's nickel reserves, primarily found in the state of Goias, further enhance its strategic importance in the electric vehicle battery materials landscape. Additionally, Brazil boasts substantial graphite resources, with significant deposits located in Minas Gerais, Bahia, and Ceara, positioning the country as a critical player in the production of anode materials for lithium-ion batteries.

- The Brazilian government has recognized the strategic importance of the electric vehicle battery materials sector and has implemented various initiatives to foster its development. These efforts include investment incentives, research and development support, and regulatory frameworks aimed at promoting sustainable mining practices and local value addition.

- For instance, in April 2024, Sigma Lithium, in a strategic move, has greenlit a USD 100 million capital expenditure for Phase 2 of its Greentech Industrial Plant in Brazil. By 2025, this investment aims to ramp up the annual production capacity of its Quintuple Zero Green Lithium from 270,000 tons to an impressive 520,000 tons. With the expansion, sanctioned by Sigma's board, the company is poised to churn out sufficient lithium concentrate to fuel an estimated 1.8 million electric vehicles (EVs).

- The National Mining Agency (ANM) has streamlined licensing processes for battery material projects. At the same time, the Brazilian Development Bank (BNDES) has established financing programs to support companies involved in the electric vehicle supply chain. These measures have begun to attract both domestic and foreign investments, with several major mining companies and battery manufacturers exploring opportunities in the country.

- Therefore, Brazil is expected to witness significant growth during the forecast period, as mentioned above.

South America Electric Vehicle Battery Materials Industry Overview

The South America Electric Vehicle Battery Materials Market is semi-fragmented. Some of the key players in this market (in no particular order) are BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, Albemarle Corporation, and Umicore SA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50003558

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Lack of Battery Material Production Facility

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Colombia

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BASF SE

- 6.3.2 Mitsubishi Chemical Group Corporation

- 6.3.3 UBE Corporation

- 6.3.4 Umicore SA

- 6.3.5 Sumitomo Chemical Co., Ltd.

- 6.3.6 Albemarle Corporation

- 6.3.7 YOUME

- 6.3.8 BYD Co., Ltd.

- 6.3.9 Arkema SA

- 6.3.10 Nichia Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.