Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636274

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636274

Europe Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 110 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

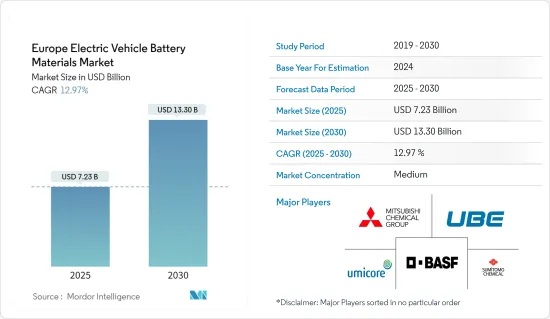

The Europe Electric Vehicle Battery Materials Market size is estimated at USD 7.23 billion in 2025, and is expected to reach USD 13.30 billion by 2030, at a CAGR of 12.97% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, growing electric vehicle (EV) sales and supportive government policies and regulations are expected to drive the demand for electric vehicle battery materials during the forecast period.

- On the other hand, the high import dependency on battery materials and the impact on the supply chain are likely to negatively impact the market.

- However, as batteries evolve with advancements like enhanced energy density, quicker charging, heightened safety, and extended lifespans, significant opportunities emerge for players in the electric vehicle battery materials market.

- Driven by a surge in electric vehicle adoption, Germany is poised to lead as the fastest-growing region in Europe's electric vehicle battery materials market.

Europe Electric Vehicle Battery Materials Market Trends

Lithium-Ion Battery Type Dominate the Market

- The production of lithium-ion batteries for electric vehicles (EVs) is on the rise, significantly influencing the battery materials market. This surge in production has driven up the demand for lithium, and discoveries of lithium in the region are notably affecting raw material costs.

- Key market players are channeling investments into lithium reserves and R&D, aiming to boost lithium-ion battery production and meet the growing demand for battery raw materials. As new reserves are discovered, the prices of lithium-ion batteries have seen a downward trend over time.

- For instance, in 2023, battery prices for electric vehicles (EVs) and battery energy storage systems (BESS) dropped to USD 139/kWh, marking a decline of over 13%. With ongoing technological innovations and manufacturing improvements, projections suggest prices will further dip to USD 113/kWh by 2025 and reach USD 80/kWh by 2030.

- Moreover, European governments are actively promoting lithium-ion battery production for EVs, driven by mounting environmental concerns. With a keen focus on achieving net-zero carbon emissions, these governments have launched multiple initiatives to boost lithium-ion battery production, aiming to meet the surging EV demand.

- For instance, in November 2023, the United Kingdom government unveiled a GBP 50 million (USD 63 million) investment to fortify its battery supply chain, including lithium-ion batteries, aligning with the nation's future EV production goals. The Battery Strategy promises focused support for zero-emission vehicles and their supply chains, with new capital and R&D funding extending to 2030. Such initiatives are poised to bolster the adoption of lithium-ion batteries as a clean energy source, subsequently driving up the demand for battery materials.

- Additionally, as lithium-ion battery prices decline and demand surges, the establishment of new production plants further fuels the need for battery raw materials. Recent years have witnessed a significant uptick in investments aimed at boosting lithium-ion battery production.

- For instance, in February 2024, France unveiled a EUR 10 billion (USD 10.84 billion) investment, sourced from both public and private entities, to establish four gigafactories for electric vehicle batteries, including lithium-ion variants, across the nation in the upcoming years. Such strategic investments are set to amplify battery production in France, subsequently heightening the demand for lithium-ion battery materials.

- Given these advancements and initiatives, a marked increase in lithium-ion battery production and a surge in demand for EV battery materials are anticipated during the forecast period.

Germany to Witness Significant Growth

- Germany plays a significant role in the electric vehicle (EV) battery materials sector, driven by its automotive industry and commitment to sustainable mobility. In the past few years, the country has become one of the leading EV producers across the region.

- According to the International Energy Agency (IEA), Electric vehicle (EV) sales in Germany reached 0.7 million units in 2023, consistent with 2022 figures but marking a 5.5-fold increase since 2019. With numerous projects and initiatives recently launched by the European government, EV sales are poised for significant growth in the coming years.

- Germany plays a pivotal role in the European Battery Alliance, which aims to establish a competitive and sustainable battery cell manufacturing value chain in Europe. Collaborating closely with leading EV companies, the German government is making substantial investments in domestic battery cell production facilities.

- In January 2024, Northvolt, a Swedish lithium-ion battery manufacturer, secured European Union approval for a significant EUR 902 million (USD 986.43 million) state aid package. This funding is earmarked for establishing an EV and hybrid vehicle battery production plant in Heide, Germany. Such moves are set to boost battery production in the region, driving up demand for EV battery materials.

- Germany is leading the charge in advanced battery recycling technologies. Both companies and research institutions are innovating efficient methods to extract valuable materials, such as lithium, cobalt, and nickel, from used batteries.

- In May 2024, Elemental Strategic Metals (ESM), a Polish firm, in collaboration with its US start-up partner Ascend Elements, unveiled plans for a lithium-ion battery recycling plant. With a capacity of 25,000 tonnes per year, construction is slated for autumn 2024, aiming for operational status by 2026. Such ventures are set to boost raw material production, further elevating the output of EV battery materials.

- Given these developments, the trajectory points towards heightened battery production for EVs and a marked surge in demand for EV battery materials in the forecast period.

Europe Electric Vehicle Battery Materials Industry Overview

Europe's electric vehicle battery materials market is moderately fragmented. Some key players (not in particular order) are BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, Umicore, Sumitomo Chemical Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50003561

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Dependency on Imported Raw Material Supply

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 France

- 5.3.3 United Kingdom

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Russia

- 5.3.7 Turkey

- 5.3.8 NORDIC

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Sumitomo Chemical Co., Ltd.

- 6.3.2 BASF SE

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 UBE Corporation

- 6.3.5 Umicore SA

- 6.3.6 Contemporary Amperex Technology Co. Limited

- 6.3.7 Johnson Matthey

- 6.3.8 ENTEK International LLC

- 6.3.9 Northvolt

- 6.3.10 SGL Carbon

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.