Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636273

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636273

China Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 95 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

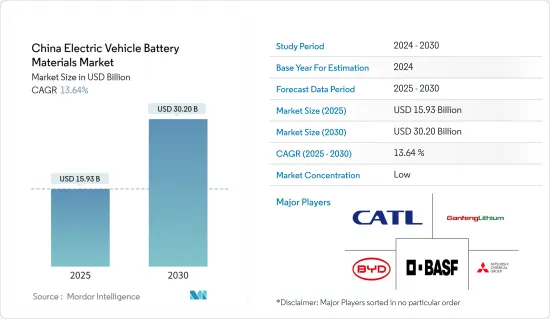

The China Electric Vehicle Battery Materials Market size is estimated at USD 15.93 billion in 2025, and is expected to reach USD 30.20 billion by 2030, at a CAGR of 13.64% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as growing electric vehicle sales and supportive government policies and regulations are expected to be among the most significant drivers for the China Electric Vehicle Battery Materials Market during the forecast period.

- On the other hand, the country's reliance on imported raw materials makes the industry vulnerable to price fluctuation, which is expected to negatively impact the market studied.

- Nevertheless, there is continued growing demand for advancements in battery technology. This factor is expected to create several opportunities for the market in the future.

China Electric Vehicle Battery Materials Market Trends

Lithium-ion Battery Type to Dominate the Market

- The global lithium-ion electric vehicle battery market is a dynamic arena, teeming with both opportunities and challenges. Lithium-ion rechargeable batteries are outpacing other battery technologies in popularity, primarily due to their advantageous capacity-to-weight ratio. Their adoption is further fueled by superior performance attributes, such as longevity, low maintenance, an extended shelf life, and a notable decrease in price.

- While lithium-ion batteries traditionally commanded a higher price point than their counterparts, leading market players have been channeling investments into achieving economies of scale and bolstering R&D efforts. This intensified competition has not only enhanced battery performance but also driven down lithium-ion battery prices.

- Recent trends show a consistent decline in the prices of lithium-ion batteries and cell packs, making them increasingly attractive to end-user industries. After a brief uptick in 2022, battery prices continued their downward trajectory in 2023. A significant highlight was the 14% drop in lithium-ion battery pack costs, reaching a record low of USD 139/kWh.

- Amid rising environmental concerns, the Chinese government is fervently championing electric vehicles, aligning its efforts with ambitious net-zero carbon emission targets. Lithium, a crucial component for EV storage capacity, is in high demand, prompting leading global companies to ramp up lithium extraction.

- In July 2024, Shandong province in eastern China unveiled plans for a substantial 100 billion yuan (USD 13.8 billion) investment. The ambitious blueprint encompasses an industrial chain spanning electrode materials, electrolytes, battery cells, and assembly. Shandong's strategy not only aims to diversify and enhance the quality of consumer batteries but also emphasizes bolstering R&D. The provincial government is backing Jinan and Qingdao cities to nurture companies in raw material production and battery assembly, catering to the demands of local new energy vehicle manufacturers.

- In February 2024, CATL introduced a groundbreaking lithium iron phosphate (LFP) battery boasting an impressive driving range of over 1,000 kilometers (621 miles) on a single charge. This innovation is poised to amplify raw material demand in China.

- Given these developments, the demand for lithium-ion batteries is set to surge, subsequently driving up the need for various raw materials in the coming years.

Growing Electric Vehicle Sales

- China's electric vehicle (EV) battery materials market is expanding rapidly, fueled by soaring EV sales and a national commitment to sustainable transportation. As the global leader in EV adoption, China's appetite for essential battery materials-lithium, nickel, cobalt, and manganese-has surged. These materials are pivotal for crafting lithium-ion batteries, the primary technology for EV power storage.

- China's booming EV sales are a primary catalyst for its battery materials market. In recent years, bolstered by generous government incentives, subsidies, and a robust policy framework targeting carbon emission reductions and air pollution combat, China has witnessed a meteoric rise in EV adoption. The government's New Energy Vehicle (NEV) mandate, compelling automakers to produce a specific percentage of EVs, further amplifies this momentum.

- Contemporary Amperex Technology Co. Limited (CATL), a frontrunner in battery manufacturing, is ramping up its production capacity to cater to the surging demand for EV batteries. Additionally, CATL is channeling substantial investments into research and development, aiming to boost battery performance while curtailing costs.

- In a notable move, CATL forged a strategic alliance with Tesla in June 2024, committing to supply lithium-ion batteries for Tesla's Shanghai Gigafactory. This partnership highlights the deepening ties between Chinese battery producers and international EV manufacturers.

- In 2023, China's electric vehicle sector grew by approximately 22.7% year-on-year, with battery EV sales soaring to about 5.4 million, a significant leap from 0.83 million in 2019.

- The Chinese government continues to support the EV sector through various measures, including tax incentives, subsidies for both manufacturers and consumers and investments in charging infrastructure. These policies are designed to make EVs more affordable and convenient, thereby driving higher adoption rates and, consequently, increasing the demand for battery materials. Innovations in battery technology are also shaping the market. Companies like BYD are developing new battery chemistries, such as lithium iron phosphate (LFP) batteries, which are safer and cheaper, although with slightly lower energy density than traditional lithium-ion batteries. These advancements are crucial for making EVs more accessible to the mass market.

- The outlook for the EV battery materials market in China is highly positive. With continued support from the government, technological advancements, and strategic industry partnerships, China is well-positioned to maintain its leadership in the global EV market. The ongoing expansion of production capacities by major battery manufacturers and the emphasis on sustainable practices will likely ensure a steady supply of essential materials, supporting the rapid growth of the EV sector.

China Electric Vehicle Battery Materials Industry Overview

The China Electric Vehicle Battery Materials Market is semi-fragmented. Some of the key players in this market (in no particular order) are Contemporary Amperex Technology Co., Limited, BYD Auto Co., Ltd, Ganfeng Lithium, BASF SE, and Mitsubishi Chemical Group Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50003560

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Dependence on Raw Material Supply

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted byr Leading Players

- 6.3 Company Profiles

- 6.3.1 Contemporary Amperex Technology Co., Limited

- 6.3.2 BYD Auto Co., Ltd.

- 6.3.3 Ganfeng Lithium

- 6.3.4 BASF SE

- 6.3.5 Mitsubishi Chemical Group Corporation

- 6.3.6 UBE Corporation

- 6.3.7 Umicore SA

- 6.3.8 Sumitomo Chemical Co., Ltd.

- 6.3.9 BTR New Material Group Co. Ltd.

- 6.3.10 Shanshan Co.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.