Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692567

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692567

Frozen and Canned Seafood - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 392 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

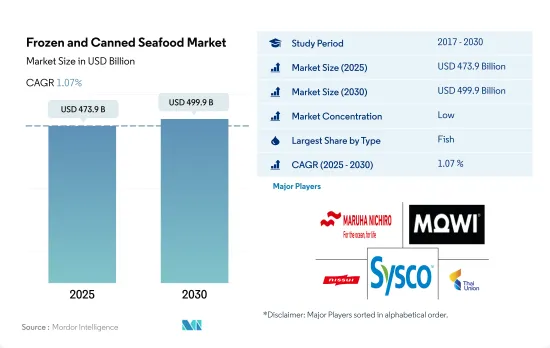

The Frozen and Canned Seafood Market size is estimated at 473.9 billion USD in 2025, and is expected to reach 499.9 billion USD by 2030, growing at a CAGR of 1.07% during the forecast period (2025-2030).

Convenience and portion control are among the major factors propelling the market's growth

- The global frozen and canned seafood market registered a CAGR of 2.44% from 2017 to 2022, owing to changing lifestyles, rising preference for seafood with growing health consciousness, rising disposable incomes, increased demand for quick meals, and the emergence of private labels. A change in consumers' preferences prompted a shift toward seafood products with a longer shelf life, like canned and frozen products. Canned seafood is growing in popularity and is associated with fairly low levels of food loss and waste. Portion control also takes place while canning since seafood is canned in small servings. Canned fish held the major share in the market, i.e., 70.69% by value in 2022. Canned tuna is the most popular canned fish consumed across the world.

- The frozen seafood marketing landscape in grocery stores has changed significantly due to the introduction of added value and convenience. Frozen fish is the major type of seafood consumed across the world. The overall sales value of frozen fish increased by 12.47% from 2017 to 2022. Retail supermarkets steadily expanded seafood offerings in their freezer cases over the last few years, and more are adding premium frozen seafood cases near fresh seafood counters. Retailers are responding to the changing purchasing behavior of consumers by providing more seafood options.

- Frozen shrimp is the fastest-growing segment, registering an estimated CAGR of 1.18% during the forecast period. Frozen shrimp has become increasingly popular due to the rapid growth of shrimps in the aquaculture industry and the growing awareness of frozen shrimp online.

Extensive fish and shrimp farming lead to extensive investments.

- The overall growth rate of frozen and canned seafood sales increased to 21.5%, by value, from 2017 to 2022. People started consuming frozen and canned seafood and meat products to fulfill their nutrient requirements as prices for fish and shrimp increased by 9% and 6.5%, respectively, from 2017 to 2022. China is heavily dependent on fish and shrimp farming and has made large-scale investments in the sector.

- In 2022, Asia-Pacific dominated frozen and canned seafood consumption with a market share of 47.4% more than Europe, 52.4% more than Africa, 54.4% more than North America, and 57.4% more than South America. This was a result of the rising demand for seafood in countries like India, where imports rose by 180% from 2019 to 2021. Malaysia is one of the biggest seafood consumers, and it saw an increase in frozen/canned fish and seafood imports by 15% from 2019 to 2021. While in South Korea, due to a rise in demand for Korean seafood dishes, frozen or canned seafood imports climbed by 10-15% between 2019 and 2021.

- Out of all the regions, Africa is predicted to be the fastest-growing frozen seafood country, with an anticipated CAGR of 2.65% in value during the forecast period. This is due to the rising personal disposable income in Africa, which increased by 2% to 3% between 2020 and 2021. The regional trend fits in with the continental trend of rising personal incomes brought on by increased urbanization, which further encouraged customer preferences for seafood that is ready to eat. Fish is a significant dietary source in Egypt, making up 25.3% of the typical household's protein consumption. According to estimates, each Egyptian consumes 23.5 kg of fish per year.

Global Frozen and Canned Seafood Market Trends

Fish production across the world is experiencing a recovery

- The demand for fish is growing across regions due to the rising awareness about its health benefits. The production of fish rose by 4.29% between 2017 and 2022. In 2022, production and trade grew slightly, and fish consumption recovered to 2018 levels due to increasing demand. Aquaculture production was anticipated to grow by 2.6% in 2023, slightly below its long-term growth rate of 3.3% between 2015 and 2020. High fuel prices, lower quotas for key stocks, and inclement weather in key fishing grounds all contributed to a slowdown in capture fisheries.

- Fish production in Asia-Pacific witnessed a growth rate of 7.37% in 2022 compared to 2021. In China, production growth continues to be driven by aquaculture production, estimated at 54.6 MMT in 2022, an increase of 1.2%. In 2021, the output value ratio of marine products to freshwater products was 45.8:54.2. In 2021, the national aquaculture area was 7009.38 thousand hectares, down by 0.38% from the previous year. Among them, the area of marine aquaculture in 2025 was 51 thousand hectares, an increase of 1.50% from 2021. The area of freshwater aquaculture was 4983.87 thousand hectares. The ratio of marine to freshwater aquaculture was 28.9:71.1.

- In 2021, about 59% of the total fish consumed in Europe came from Russia. Russia is a key market in Europe as it is one of the leading producers of cod in the world. Due to restrictions imposed on Russia's export of fish and other seafood as a result of its conflict with Ukraine, the entire region is experiencing a fish shortage. EU aquaculture accounts for around 20% of EU fish and shellfish supply. In the EU, more than 45% of aquaculture production is shellfish, more than 30% is marine fish, and more than 20% is freshwater fish.

Fish prices are increasing across the world owing to rising production as well as production disruptions

- Unusual weather and rising fuel prices have impacted the supply of fish in all markets. At the same time, increasing global demand has led to rising fish prices. Salmon prices in 2023 started on an upward trend in both Norway and Chile, while a more erratic trend was observed in Scotland. Wholesale and consumer prices rose to record highs in some markets. However, Norwegian fresh, head-on gutted Atlantic salmon sold at USD 9.69/kg in week 13 of 2023, falling for two consecutive weeks.

- In Europe, fish prices ranged from USD 0.13/kg to USD 62/kg, where Grey Gurnard was the cheapest, and European Hake was the costliest during the first quarter of 2023. The Russian-Ukrainian conflict had a significant impact on some exports from Norway, such as fresh salmon to Asia, as the closed Russian airspace had a volume impact on shipments to countries such as South Korea (-18%) and Japan (-20%). Price hikes also distorted the flow of goods from countries where salmon is largely destined for smoking before re-export. For instance, the volume of exports to Poland fell by 18% in 2022.

- Chinese producer prices for whole tilapia hit a five-year high in 2023. In Guangdong, which accounts for nearly 40% of China's tilapia production, live tilapia weighing 500-800 g was sold at USD 1.47/kg, up by 14% from 2022. In the US domestic market, above-average inflation in the seafood category led to a jump in the price of fresh and frozen seafood sales, with the average cost of tilapias rising by over 20% in the first half of 2022. In addition to the North American market, demand in the European Union also recovered, with buyer interest in tilapia products increasing due to rising prices of other seafood species in the global market.

Frozen and Canned Seafood Industry Overview

The Frozen and Canned Seafood Market is fragmented, with the top five companies occupying 3.02%. The major players in this market are Maruha Nichiro Corporation, Mowi ASA, Nippon Suisan Kaisha Ltd, Sysco Corporation and Thai Union Group PCL (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92390

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Fish

- 3.1.2 Shrimp

- 3.2 Production Trends

- 3.2.1 Fish

- 3.2.2 Shrimp

- 3.3 Regulatory Framework

- 3.3.1 Australia

- 3.3.2 Canada

- 3.3.3 China

- 3.3.4 France

- 3.3.5 Germany

- 3.3.6 India

- 3.3.7 Italy

- 3.3.8 Japan

- 3.3.9 Mexico

- 3.3.10 Saudi Arabia

- 3.3.11 United Arab Emirates

- 3.3.12 United Kingdom

- 3.3.13 United States

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Type

- 4.1.1 Fish

- 4.1.2 Shrimp

- 4.1.3 Other Seafood

- 4.2 Distribution Channel

- 4.2.1 Off-Trade

- 4.2.1.1 Convenience Stores

- 4.2.1.2 Online Channel

- 4.2.1.3 Supermarkets and Hypermarkets

- 4.2.1.4 Others

- 4.2.2 On-Trade

- 4.2.1 Off-Trade

- 4.3 Region

- 4.3.1 Africa

- 4.3.1.1 By Type

- 4.3.1.2 By Distribution Channel

- 4.3.1.3 By Country

- 4.3.1.3.1 Egypt

- 4.3.1.3.2 Nigeria

- 4.3.1.3.3 South Africa

- 4.3.1.3.4 Rest of Africa

- 4.3.2 Asia-Pacific

- 4.3.2.1 By Type

- 4.3.2.2 By Distribution Channel

- 4.3.2.3 By Country

- 4.3.2.3.1 Australia

- 4.3.2.3.2 China

- 4.3.2.3.3 India

- 4.3.2.3.4 Indonesia

- 4.3.2.3.5 Japan

- 4.3.2.3.6 Malaysia

- 4.3.2.3.7 South Korea

- 4.3.2.3.8 Rest of Asia-Pacific

- 4.3.3 Europe

- 4.3.3.1 By Type

- 4.3.3.2 By Distribution Channel

- 4.3.3.3 By Country

- 4.3.3.3.1 France

- 4.3.3.3.2 Germany

- 4.3.3.3.3 Italy

- 4.3.3.3.4 Netherlands

- 4.3.3.3.5 Russia

- 4.3.3.3.6 Spain

- 4.3.3.3.7 United Kingdom

- 4.3.3.3.8 Rest of Europe

- 4.3.4 Middle East

- 4.3.4.1 By Type

- 4.3.4.2 By Distribution Channel

- 4.3.4.3 By Country

- 4.3.4.3.1 Bahrain

- 4.3.4.3.2 Kuwait

- 4.3.4.3.3 Oman

- 4.3.4.3.4 Qatar

- 4.3.4.3.5 Saudi Arabia

- 4.3.4.3.6 United Arab Emirates

- 4.3.4.3.7 Rest of Middle East

- 4.3.5 North America

- 4.3.5.1 By Type

- 4.3.5.2 By Distribution Channel

- 4.3.5.3 By Country

- 4.3.5.3.1 Canada

- 4.3.5.3.2 Mexico

- 4.3.5.3.3 United States

- 4.3.5.3.4 Rest of North America

- 4.3.6 South America

- 4.3.6.1 By Type

- 4.3.6.2 By Distribution Channel

- 4.3.6.3 By Country

- 4.3.6.3.1 Argentina

- 4.3.6.3.2 Brazil

- 4.3.6.3.3 Rest of South America

- 4.3.1 Africa

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Admiralty Island Fisheries Inc.

- 5.4.2 Bolton Group SRL

- 5.4.3 FCF CO. Ltd

- 5.4.4 Golden Prize Canning Company Limited

- 5.4.5 High Liner Foods Inc.

- 5.4.6 Maruha Nichiro Corporation

- 5.4.7 Mowi ASA

- 5.4.8 Nippon Suisan Kaisha Ltd

- 5.4.9 Sysco Corporation

- 5.4.10 Thai Union Group PCL

- 5.4.11 Trident Seafood Corporation

6 KEY STRATEGIC QUESTIONS FOR SEAFOOD INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.