Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692052

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692052

Asia-Pacific Seafood - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 227 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

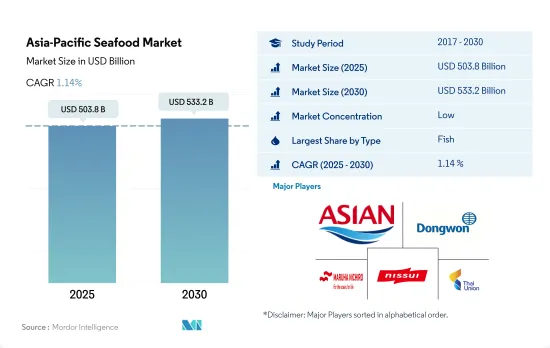

The Asia-Pacific Seafood Market size is estimated at 503.8 billion USD in 2025, and is expected to reach 533.2 billion USD by 2030, growing at a CAGR of 1.14% during the forecast period (2025-2030).

Increasing in food establishments in the region is boosting the market's growth

- In 2022, the fish type segment occupied a 61% higher market share than the other seafood type segment and a 68.4% higher market share than the shrimp segment. The fish type segment registered a growth of 21.2% by value from 2016 to 2021, mainly due to an increase in the population, which led to an increase in consumer preference for fish due to its affordable cost compared to shrimp and other seafood. In 2022, each person consumed twice as much fish as 50 years ago on average.

- Shrimp is expected to be the fastest-growing seafood type consumed in Asia-Pacific, registering a CAGR of 2.07% by value during the forecast period. China accounts for around 60% of total shrimp sales in the Asia-Pacific region. The increase in HRI players like food establishments rose to 1.2% from 2021, reaching 9.7 million restaurants by 2022 after the COVID-19 pandemic. Food establishments are attracting customers through the change in menus, such as the addition of seafood menus like shrimps and varied tastes of seafood across the Asia Pacific region, which is expected to drive sales and increase market share.

- The COVID-19 pandemic disrupted seafood supply chains through factors such as a shortage of workers and lack of automation, which impacted all stakeholders from 2020 to 2021. To mitigate the risk associated with this type of outbreak, the industry saw increased investments in logistics, packaging, and automation of seafood in countries like China and India. Big companies like Thai Union started using satellite technology for advanced traceability and increased their online presence through food and home deliveries, which further boosted company sales. The industry witnessed around 70 million people shopping online in Southeast Asia from 2019 to 2021.

The market is primarily driven by rising health awareness

- In the Asia-Pacific market, seafood sales increased by 12.99% by value from 2017 to 2022. Non-vegetarian consumers in the region are gradually adopting a more pescatarian lifestyle. Due to customers' growing inclination toward a healthy diet, this movement has been noticed. Asia accounted for 73% of the seafood sales worldwide in 2022 and consumed more than two-thirds of the available seafood supply.

- In 2022, China accounted for a significant share of 49.64% by value in the Asia-Pacific seafood market. The high domestic demand for seafood in China is because of growing consumer perceptions that seafood is a healthy source of protein, along with a rising preference for seafood products among middle-class consumers owing to increasing disposable incomes. With growing spending on seafood in the country, the market is anticipated to experience a growth in demand for high-quality, value-added fish and seafood products.

- Indonesia accounted for the second-highest share in the Asia-Pacific fish market, with 10.44% by value in 2022. The country's government is taking initiatives to protect local fisheries as most of Indonesia's fisheries are over-exploited or fully exploited, with illegal fishing practices being common. Organizations such as The Nature Conservancy are transforming fishery practices in Indonesia by monitoring fish stocks, tracking fishing vessels, developing species identification technology, promoting rights-based management in small near-shore fisheries, and other initiatives. Japan is one of the other major markets where the government's Fisheries Agency is working to increase the number of fish caught by improving resource management policies. Such initiatives are increasing the food self-sufficiency rate across Asia-Pacific countries.

Asia-Pacific Seafood Market Trends

Southeast Asian countries account for the major production share

- Fish production in the region grew by 3.99% from 2017 to 2022. Asia has dominated the aquaculture industry for the past 20 years, with Southeast Asia leading the segment. Indonesia is Southeast Asia's top producer of aquaculture, accounting for around 50% of regional aquaculture production in general. Vietnam, the Philippines, and Thailand are also major producers of aquaculture in the region. Indonesia is also the regional leader when it comes to brackish water and mariculture culture, particularly in shrimp production. When it comes to fresh-water aquaculture culture, Vietnam leads the way, followed by Indonesia.

- In 2022, China's fish production grew by 6.86% compared to 2021. Pond production accounted for more than half of all aquaculture production in China, with reservoirs that house cage systems making up 28.8% of the total and rivers making up 3.49% in 2022. In 2022, the Chinese government launched its 14th five-year National Fisheries Development Plan (NFDP), which aims to produce 69 million tons of aquatic products by 2025. This indicates that China's vast fishing sector will continue to grow.

- India's fish production reached a new record high of 8990 million tons in 2022. Inland fish production, mainly in the form of aquaculture, saw a dramatic increase. In 2000-2001, inland fish production was 28.23 lakh tons, and in 2021-2022, it increased to 121.21 lakh tons, increasing by 400%. The increase in inland fish production is a result of concerted efforts by fisheries scientists and central and state governments, as well as the commitment of fishermen, fish farmers, and entrepreneurs.

Price growth can majorly be attributed to rising supply chain costs

- The price of fish experienced significant changes in the Asia-Pacific region, growing by 6.53% in 2022 compared to 2017. In China, the fish segment increased its share of the overall category as it is widely popular among Chinese households and can be easily cooked at home, unlike crustaceans, mollusks, and cephalopods. Consumers are willing to pay a premium price for fish and seafood products that they perceive to be of good quality, natural, safe, and healthy. In 2022, the prices of silver carp fish started from USD 0.9/kg, and turbot fish prices started from USD 12/kg. Common species like tilapia also saw a growth in prices. The prices were raised to encourage fish sales, allowing farmers to repay loans for feed costs. Some farmers also expected a higher price in the future and held the stocks, pushing the price higher.

- In India, seafood is considered an important part of a healthy and balanced diet by most consumers. During the 2nd quarter of 2022 in India, fish-catching activities were reduced due to an increase in sea temperature, coupled with a rise in fuel prices. Thus, the supply of fresh fish reduced drastically, leading to a 20-30% rise in prices for both premium and common species. In India, the prices of major species during the 2nd quarter of 2022 were USD 2.64/kg for mackerel and sardine, USD 13.21/kg for white pomfret, and USD 14.53/kg for seer. Australian seafood prices climbed to record highs due to the continued effects of supply chain issues and labor shortages. In 2022, the price of salmon increased by as much as 30%, reaching USD 34.05/kg compared to the previous year. Queensland fish prices remained competitive and had good value, with wild-caught Queensland northern kingfish at USD 18.18/kg and large wild-caught tigerfish at USD 23.60/kg in 2022.

Asia-Pacific Seafood Industry Overview

The Asia-Pacific Seafood Market is fragmented, with the top five companies occupying 1.82%. The major players in this market are Asian Sea Corporation Public Company Limited, Dongwon Industries Ltd, Maruha Nichiro Corporation, Nippon Suisan Kaisha Ltd and Thai Union Group PCL (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90348

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Fish

- 3.1.2 Shrimp

- 3.2 Production Trends

- 3.2.1 Fish

- 3.2.2 Shrimp

- 3.3 Regulatory Framework

- 3.3.1 Australia

- 3.3.2 China

- 3.3.3 India

- 3.3.4 Japan

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Type

- 4.1.1 Fish

- 4.1.2 Shrimp

- 4.1.3 Other Seafood

- 4.2 Form

- 4.2.1 Canned

- 4.2.2 Fresh / Chilled

- 4.2.3 Frozen

- 4.2.4 Processed

- 4.3 Distribution Channel

- 4.3.1 Off-Trade

- 4.3.1.1 Convenience Stores

- 4.3.1.2 Online Channel

- 4.3.1.3 Supermarkets and Hypermarkets

- 4.3.1.4 Others

- 4.3.2 On-Trade

- 4.3.1 Off-Trade

- 4.4 Country

- 4.4.1 Australia

- 4.4.2 China

- 4.4.3 India

- 4.4.4 Indonesia

- 4.4.5 Japan

- 4.4.6 Malaysia

- 4.4.7 South Korea

- 4.4.8 Rest of Asia-Pacific

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 American Seafoods Company LLC

- 5.4.2 Asian Sea Corporation Public Company Limited

- 5.4.3 Blue Snow Food Co. Ltd

- 5.4.4 Dongwon Industries Ltd

- 5.4.5 Maruha Nichiro Corporation

- 5.4.6 Millennium Ocean Star Corporation

- 5.4.7 Nippon Suisan Kaisha Ltd

- 5.4.8 Thai Union Group PCL

- 5.4.9 Wynntech Star Sdn Bhd

6 KEY STRATEGIC QUESTIONS FOR SEAFOOD INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.