Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692082

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692082

GCC Seafood - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 214 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

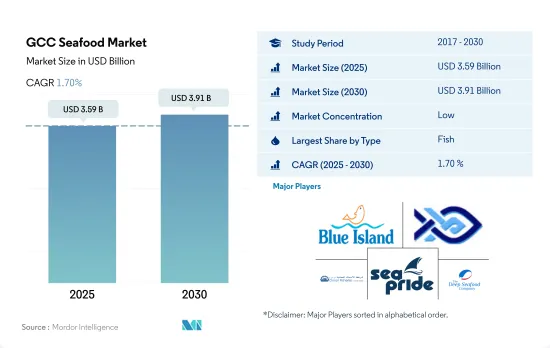

The GCC Seafood Market size is estimated at 3.59 billion USD in 2025, and is expected to reach 3.91 billion USD by 2030, growing at a CAGR of 1.70% during the forecast period (2025-2030).

Saudi Arabia dominates the regional market with the assistance of strategic investments and partnerships

- In 2022, fish occupied the largest share among all other seafood variants in the market. The sales value grew at a CAGR of 2.37% over 2017-22. The increasing health consciousness among the population and preference toward a nutrient and protein-rich diet without added cholesterol components is leading consumers to spend more on different varieties of fish like sardines, salmon, and tuna. The region of the GCC, apart from hosting extensive desert lands, comprises miles of coastline that assist in the growth of local fisheries.

- Shrimp is estimated to be the fastest-growing seafood segment in the Middle East over the forecast period. Most shrimp in the region are imported from Asian countries like India, Pakistan, and China. Shrimps are an ideal choice for consumers opting for a protein-rich weight loss diet. Obesity is a pressing issue in GCC, with Kuwait, Jordan, and Saudi Arabia having more than 25% of their population identified as obese as of 2023, expanding the opportunity for the shrimp industry to flourish in the region.

- Saudi Arabia is one of the significant countries in the region, occupying one of the highest shares in the market over the study period. The country launched the National Fisheries Development Program as a part of its Vision 2030 to raise a fund of USD 4 billion in 2022. This fund is expected to increase infrastructure and develop the workforce for inland fisheries cultivation. The United Arab Emirates proposed fuel subsidies to its fishing sector to reduce operating costs in 2022 in partnership with the UAE Ministry of Climate Change and the Environment, Abu Dhabi National Oil Company, and Emirates National Oil Company.

Increasing private sector investments in seafood production are driving the demand

- The United Arab Emirates is the leader in the Middle Eastern seafood market. The seafood consumption per person increased, reaching 25.50 kg in 2021, ranking second only to Oman's 29.01 kg. The demand for seafood products is driven by an expanding population with rising income levels and a growing appetite for fish. Nearly 90% of the Emirati population is made up of immigrants, and the typical meals in the region often include seafood products. Indians make up over 40% of the total population in the United Arab Emirates, followed by Indonesians and Bangladeshis.

- Saudi Arabia intends to produce 300,000 metric tons of fish by 2025 and 600,000 metric tons by 2030. Private sector investments in the pre-harvest, production, and post-harvest segments of the aquaculture sector witnessed a sharp increase as a result of the initiative. Saudi Arabia's partnership with the Network of Aquaculture Centers in Asia-Pacific (NASA) also aims to increase the nation's seafood production. The higher availability of seafood is expected to increase local demand further.

- Bahrain is projected to register the fastest CAGR of 5.11% during the forecast period. Fish farming is a crucial sector that the government is relying on to ensure food security, as marine products are a key food item in Bahrain. In 2021, six plots of land were identified as candidates to boost agricultural production and fish farming as part of efforts to ensure the country's food security. The move is expected to achieve 50-62% self-sufficiency in fish. Investing in fish farming has many benefits, such as reducing pressure on natural resources and releasing fish fingerlings raised on the farm into the wild to restock Bahrain's marine population.

GCC Seafood Market Trends

Self-sufficiency initiatives implemented by governments are anticipated to grow with production

- Saudi Arabia is the largest fish producer in the Middle East, producing 446,977 tons of fish in 2022. Fish production in Saudi Arabia increased by 6.48% from 2017 to 2022, followed by the United Arab Emirates, with 287091.9747 tons in 2022. Fish production increased gradually from 2021 to 2022, mainly due to the government's focus on fisheries. Governments are boosting opportunities to involve the private sector in fisheries. A unique program, the National Fisheries Development Program, aims to enhance the fisheries sector's contribution to GDP and increase the productivity of the aquaculture sector to 600 thousand tons in stages from 15 years to 2030. Regional centers for fishing academies have also been established to support fisheries. Over USD 80 million was invested in the research activities of fish to enhance production capabilities.

- Countries like the UAE have the highest annual per capita fish consumption in the Gulf Cooperation Council (GCC), which is nearly 50% higher than the global average. Despite rapid economic growth, the UAE's local fisheries are overfished, and local fish account for only 8% of UAE consumption.

- Fish production is projected to increase sustainably from 2023 to 2029. Support from the private sector and identification of fisheries for enhanced development, new partnerships with stakeholders and subsidies for fisheries, and the development of 3,000 fisheries with resource persons may help increase the production and productivity of fisheries from 2022. For instance, in 2021, NEOM Company and Tabuk Fish Company signed a memorandum of understanding to expand local aquaculture production and apply the new generation of aquaculture technologies in the NEOM region of Saudi Arabia.

High dependency on imports raises prices

- In 2022, the United Arab Emirates had the highest fish prices compared to Saudi Arabia and the Rest of Middle East, with the price difference being around USD 4,022 per ton. The difference was mainly due to more subsidies on fuel, infrastructure, and other associated costs by the Saudi Arabian government. The country has the added advantage of a 2,640 km coastline. The retail price range for fish in the United Arab Emirates in June 2023 was between USD 4 and USD 20 per kilogram or between USD 1.81 and USD 9.07 per pound (lb).

- The prices in the Middle East increased due to high demand, which exceeded the supply. The local fish supply decreased, and local production was hampered due to unfavorable climatic conditions in 2020 and 2021. The daily auctions for fish sales by fishermen enable buyers to strike good deals and resell their goods at higher prices, thus directly increasing retail consumer fish prices.

- From 2021 to 2022, fish prices increased by around 0.96%, from USD 3,043 to USD 3,072. The rising fish prices are due to increasing oil prices and rising inflation. To curb this increase, the governments are launching relief measures. For instance, in 2022, the UAE government doubled the budget to support low-income families in the country. Another instance is when the king of Saudi Arabia announced USD 5.33 billion for direct cash transfers and stockpiling in 2022.

- Fish prices are expected to record a sustainable growth rate during the forecast period (2023-2029). Several public and private partnerships are undertaken to enhance the production of fisheries in the Middle East. Saudi Arabia spent USD 80 million on research and planning to develop fish cultivation inland with master trainers to increase production, which is anticipated to help with constant prices.

GCC Seafood Industry Overview

The GCC Seafood Market is fragmented, with the top five companies occupying 4.16%. The major players in this market are Blue Island PLC, National Fishing Company K.S.C., Oman Fisheries Co. SAOG, Sea Pride LLC and The Deep Seafood Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90390

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Fish

- 3.1.2 Shrimp

- 3.2 Production Trends

- 3.2.1 Fish

- 3.3 Regulatory Framework

- 3.3.1 Saudi Arabia

- 3.3.2 United Arab Emirates

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Type

- 4.1.1 Fish

- 4.1.2 Shrimp

- 4.1.3 Other Seafood

- 4.2 Form

- 4.2.1 Canned

- 4.2.2 Fresh / Chilled

- 4.2.3 Frozen

- 4.2.4 Processed

- 4.3 Distribution Channel

- 4.3.1 Off-Trade

- 4.3.1.1 Convenience Stores

- 4.3.1.2 Online Channel

- 4.3.1.3 Supermarkets and Hypermarkets

- 4.3.1.4 Others

- 4.3.2 On-Trade

- 4.3.1 Off-Trade

- 4.4 Country

- 4.4.1 Bahrain

- 4.4.2 Kuwait

- 4.4.3 Oman

- 4.4.4 Qatar

- 4.4.5 Saudi Arabia

- 4.4.6 United Arab Emirates

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Albatha Group

- 5.4.2 Almunajem Foods

- 5.4.3 Blue Island PLC

- 5.4.4 Enhance Group Holding Company Limited

- 5.4.5 National Fishing Company K.S.C.

- 5.4.6 Oman Fisheries Co. SAOG

- 5.4.7 Sea Pride LLC

- 5.4.8 The Deep Seafood Company

- 5.4.9 Thomsun Group

- 5.4.10 Yamama Al-Baida Gen. Trading & Cont. Est.

6 KEY STRATEGIC QUESTIONS FOR SEAFOOD INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.