Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692050

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692050

North America Seafood - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 229 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

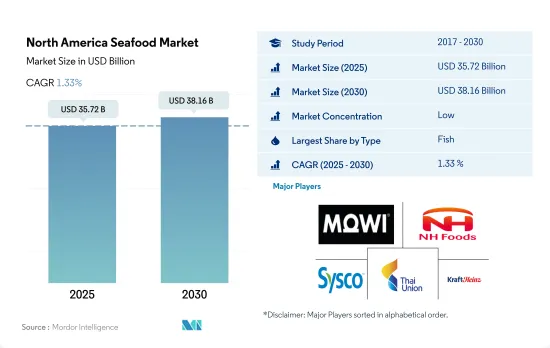

The North America Seafood Market size is estimated at 35.72 billion USD in 2025, and is expected to reach 38.16 billion USD by 2030, growing at a CAGR of 1.33% during the forecast period (2025-2030).

Improving freezing technologies are boosting sales in the region

- The overall North American seafood market is expected to register a CAGR value of 0.77% during the forecast period. People spent over USD 180-200 on seafood in the United States as of 2021. The US President signed an executive order to promote American seafood in May 2020 to boost competitiveness in the seafood industry. It also urges the expansion of sustainably produced seafood in the United States. For competitive expansion, major corporations, including Marine Harvest, Starkist, and Nippon Suisan, are concentrating on the market's numerous product innovations.

- In North America, shrimp is the fastest-growing segment in the seafood market, with a projected CAGR value of 1.33% during the forecast period. The shrimp sector is gaining traction as shrimp are being widely used in dietary supplements to overcome the lack of protein intake among consumers. The major shrimp-producing brands are SeaPak, Wild Gulf Shrimp, and Sam's Choice.

- In the United States, regulators implemented season-length restrictions, total allowable catch limits, and gear and vessel power restrictions to combat overfishing. As a result, fishermen adopted new technologies and methods to work around these controls, and the prices of fish increased. The United States witnessed a price of 2.4 per kg in 2022 from 19.3 per kg in 2017. Improving infrastructure, freezing storage facilities, and ensuring the availability of high-quality fish commodities for domestic consumers are critical components of an efficient and profitable supply chain. Thus, there will also be growth in the importance of organizations that support sustainable fishing, such as the Global Seafood Alliance, the Global Sustainable Seafood Initiative, and the Sustainable Fisheries Partnership.

Sustainability is highly implemented and promoted, significantly driving the market

- The seafood market in the region observed a steady growth during the study period. The market grew by 27.37% in value from 2017 to 2022. The consumption is increasing in the region due to the growing interest in the health benefits of seafood consumption, which is boosted by various awareness campaigns such as 'Eat Seafood America.' Similarly, NOAA (NATIONAL OCEANIC AND ATMOSPHERIC ADMINISTRATION) offers the public with simple, scientifically based information to aid in making informed, sustainable seafood decisions. FishWatch, an online platform by NOAA, provides constantly updated information on how seafood in the United States is gathered in accordance with laws that maintain a healthy environment and ensure growing fish populations.

- The United States accounted for the major share of the North American seafood market and recorded a Y-o-Y growth rate of 2.16% by value from 2021 to 2022. The on-trade sales of seafood in the country are growing with the growing foodservice industry and the increasing number of seafood dishes on the menu. Sushi, shrimp tempura, and crab rangoon are among the 15 dishes that diners most want to order when eating away from home in the United States.

- Canada is projected to record the highest CAGR value of 1.68% during the forecast period, primarily driven by processed shrimp. The market has seen a growth in demand for label-friendly products like sustainable seafood and locally produced seafood. Manufacturers and regulatory agencies are taking steps to guarantee that when customers shop for seafood at the market, they may be confident that it has been sustainably fished or farmed if the species is harvested in the region.

North America Seafood Market Trends

Rising demand and advancements in technologies are helping production growth

- The US is the leading fish producer in North America, followed by Mexico. Salmon is the most produced in the region. However, advances in technology, aquaculture feeds, and management techniques are making more species available. Marine aquaculture accounts for 7% of total domestic seafood production by weight. However, the focus on high-value products has resulted in growth in aquaculture, contributing 24% of the value of domestic seafood products.

- In Canada, the production value grew from USD 234 million to USD 1.3 billion, while the production volume grew from roughly 50,000 tons to 191,000 tons from 1991 to 2021. Industry production is primarily represented by finfish, which accounted for 78% of total volume and 91% by value in 2021. The majority of finfish production, by both volume and value, is salmon. In 2021, salmon production alone accounted for 63% of the total volume and 74% of total value. British Columbia remains the largest producer of salmon, accounting for 50% of total volume and 55% of total value in 2021. British Columbia is followed by New Brunswick (16% of volume and 19% of value), Prince-Edward-Island (13% of volume and 4% of value), and Newfoundland and Labrador (10% of volume and 11% of value).

- Mexico has enormous potential in the fisheries sector, as it has 11,592 km of coastline, of which 76% is on the Pacific coast, and 24% is in the Gulf of Mexico and the Caribbean coast and islands. Its continental shelf is approximately 394 000 km2, being larger in the Gulf of Mexico. It also has 12 500 km2 of coastal lagoons and estuaries and 6 500 km2 of inland waters such as lakes, lagoons, reservoirs, and rivers. The tuna fisheries in the Pacific are significant, with around 150,000 tons per year. Yellowfin is the main species in the tuna family.

Supply shortage and economic instability are impacting the prices in Canada and Mexico

- The average fish prices in the region grew by 0.96% in 2022 compared to the previous year. In the United States, the price of seafood was the highest, accounting for around USD 2443/ton in 2022. Average seafood prices generally increased over the study period; however, the rate showed a decreasing trend in the years before the pandemic. For fish products sold with weight information, prices increased by more than 2.2% in 2021 and another 5% in 2022. For products sold without weight information, the trend in prices and percentage changes in price was similar, but with lower average prices and a wider range of growth rate values. Tuna and catfish saw the highest growth in price from 2016 to 2021. In the United States, catfish saw a growth of 21% in prices, costing around USD 12.38/kg, while tuna experienced 18% price growth in the same period with a retail price of USD 13/kg.

- In Canada, fish prices increased by 14.63% from 2017 to 2022. Due to overfishing and bycatch, the supply of fish fell, and fish prices increased. Canada produces some of the most popular seafood globally, and a majority of fish is exported. Fish prices in Canada increased due to supply shortages due to the increasing demand from international trade.

- According to the OECD-FAO Agricultural Outlook, average nominal fish prices will increase over 2022-2031, starting from a high level in 2022, reflecting a strong price recovery in 2022 from COVID-driven declines in 2020 and 2021. In late 2021 and early 2022, fish prices started to increase, with a negative impact on consumption due to an unstable economic and geopolitical situation in the region.

North America Seafood Industry Overview

The North America Seafood Market is fragmented, with the top five companies occupying 14.17%. The major players in this market are Mowi ASA, NH Foods Ltd, Sysco Corporation, Thai Union Group PCL and The Kraft Heinz Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90346

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Fish

- 3.1.2 Shrimp

- 3.2 Production Trends

- 3.2.1 Fish

- 3.2.2 Shrimp

- 3.3 Regulatory Framework

- 3.3.1 Canada

- 3.3.2 Mexico

- 3.3.3 United States

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Type

- 4.1.1 Fish

- 4.1.2 Shrimp

- 4.1.3 Other Seafood

- 4.2 Form

- 4.2.1 Canned

- 4.2.2 Fresh / Chilled

- 4.2.3 Frozen

- 4.2.4 Processed

- 4.3 Distribution Channel

- 4.3.1 Off-Trade

- 4.3.1.1 Convenience Stores

- 4.3.1.2 Online Channel

- 4.3.1.3 Supermarkets and Hypermarkets

- 4.3.1.4 Others

- 4.3.2 On-Trade

- 4.3.1 Off-Trade

- 4.4 Country

- 4.4.1 Canada

- 4.4.2 Mexico

- 4.4.3 United States

- 4.4.4 Rest of North America

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Beaver Street Fisheries

- 5.4.2 Cooke Inc.

- 5.4.3 Dulcich Inc.

- 5.4.4 FCF Co. Ltd

- 5.4.5 Gulf Shrimp Co. LLC

- 5.4.6 High Liner Foods Inc.

- 5.4.7 Mowi ASA

- 5.4.8 NaturalShrimp Inc.

- 5.4.9 NH Foods Ltd

- 5.4.10 Pacific American Fish Company Inc.

- 5.4.11 Sysco Corporation

- 5.4.12 Thai Union Group PCL

- 5.4.13 The Kraft Heinz Company

6 KEY STRATEGIC QUESTIONS FOR SEAFOOD INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.