Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692054

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692054

United States Seafood - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 197 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

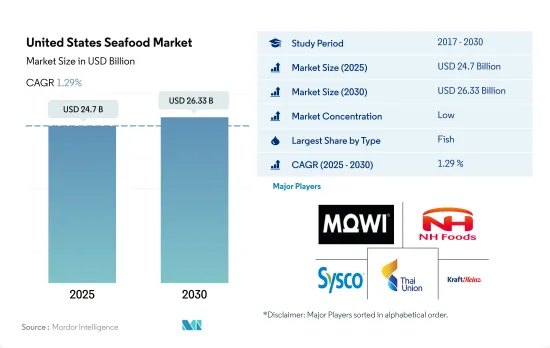

The United States Seafood Market size is estimated at 24.7 billion USD in 2025, and is expected to reach 26.33 billion USD by 2030, growing at a CAGR of 1.29% during the forecast period (2025-2030).

Hiking production potential to mitigate increasing demand for leaner protein sources and reduce import dependency is driving market growth

- The United States produced 7.8 million tons of fish (including mollusks and crustaceans) in 2022, with a value of USD 9,065.5 million. About 17% of this value came from aquaculture and 83% from fisheries. An important factor at play here is that the United States is a net importer of fish and fish products. To promote local production, the government has shown its support through many policies and ventures. The major seafood type consumed in the United States is the other seafood segment, while the fastest-moving segment is shrimp, which is projected to record a CAGR of 2.3% during the forecast period.

- In the United States, regulators implemented season-length restrictions, total allowable catch limits, and gear and vessel power restrictions to combat overfishing. As a result, fishermen adopted new technologies and methods to work around these controls. The United States witnessed a price hike of 2.4 per kg in 2022 from 19.3 per kg in 2017. The production of seafood from local aquaculture in the country has also been increasing, with the average value of production per employee in aquaculture seeing an increase of 28% compared to the previous decade.

- The market is poised to record a CAGR of 5.46% during the forecast period. The seafood industry is a major contributor to the country's economy. The United States is a key player in global aquaculture and the world's top importer of fish and fishery products. It also provides other producers worldwide with a range of cutting-edge technology, feed, equipment, and investment capital. Most of the seafood consumed in the United States, between 70 and 85%, is imported, and aquaculture is used to generate over half of it. The seafood trade deficit reached USD 17 billion in 2020.

United States Seafood Market Trends

Overfishing, high cost of fuel, and labor shortages had a negative impact on the production of captured fish

- Based on value, bivalve mollusks, including oysters, clams, and mussels, make up more than 80% of marine aquaculture production in the United States in 2022. Fish is the largest sector of aquaculture in the United States, which accounted for 66% of the market in 2022, followed by crustaceans and mollusks. The most popular types of fish farmed internationally are salmon, shrimp, trout, and sea bass, but new developments in technology, aquaculture feeds, and management strategies are making other species available. By weight, marine aquaculture makes up 7% of all domestic seafood production. However, because of the emphasis on high-value items, aquaculture now accounts for 24% of the value of domestic seafood.

- Overfishing, high fuel costs, and labor shortages have negatively impacted the production of captured fish, with fish production decreasing by 15% in 2022. Additionally, illegal fishing by foreign nationals has also impacted fish output. However, the overall drop in the actual value of fisheries production has been tempered by growth in the real value of aquaculture.

- In order to support producers and encourage fish production in the country, government assistance has come into play to aid the market's growth and development over the years. By assisting them through laws and investments, the US government has demonstrated its determination to encourage local and independent seafood producers. For instance, in February 2022, the US Department of Agriculture (USDA) invested approximately USD 50 million in grants to support seafood processors, processing facilities, and processing vessels through the Seafood Processors Pandemic Response and Safety Block Grant Program (SBRS).

Disruption in supply chain increased the price fluctuations

- Fish prices in the country witnessed standard growth in the review period and registered an average growth of 30.6% from 2017 to 2022. It is estimated that demand will outpace supply moving forward. Fish prices followed an upward trend in recent years due to limitations on supply growth, particularly for capturing fisheries, and continued registering strong demand. For fish products sold with weight information, the prices increased by more than 2.2% in 2021 and another 5% in 2022. For products sold without weight information, the trend in prices and percentage change in price was similar, but with lower average prices and a wider range of growth rate values. However, in 2021, international fish prices were, on average, just 6-8% higher than the previous year. This was primarily due to price declines for many important farmed species, including shrimp, salmon, pangasius, catfish, tilapia, and canned tuna, as a consequence of supply outpacing demand.

- On the supply side, stable production of capture fisheries, slowing growth in aquaculture production, and increased costs for inputs such as feed, energy, and oil are expected to play a role in the segment. Due to strong global demand, the prices of fishmeal and fish oil are expected to increase by 30% and 13%, respectively, by 2030.

- In 2022, the United States was one of the largest fish-importing markets, following the European Union, and accounted for an import value of around 18%. Urbanization and expansion of the fish-consuming middle class have fueled demand and growth in the country. The US seafood imports destined for retail support the largest share of the total economic contributions, which was USD 26 billion in industry output (37.0%) and USD 15 billion in value-added (39.7%) in 2022.

United States Seafood Industry Overview

The United States Seafood Market is fragmented, with the top five companies occupying 17.64%. The major players in this market are Mowi ASA, NH Foods Ltd, Sysco Corporation, Thai Union Group PCL and The Kraft Heinz Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90350

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Fish

- 3.1.2 Shrimp

- 3.2 Production Trends

- 3.2.1 Fish

- 3.2.2 Shrimp

- 3.3 Regulatory Framework

- 3.3.1 United States

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Type

- 4.1.1 Fish

- 4.1.2 Shrimp

- 4.1.3 Other Seafood

- 4.2 Form

- 4.2.1 Canned

- 4.2.2 Fresh / Chilled

- 4.2.3 Frozen

- 4.2.4 Processed

- 4.3 Distribution Channel

- 4.3.1 Off-Trade

- 4.3.1.1 Convenience Stores

- 4.3.1.2 Online Channel

- 4.3.1.3 Supermarkets and Hypermarkets

- 4.3.1.4 Others

- 4.3.2 On-Trade

- 4.3.1 Off-Trade

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Admiralty Island Fisheries Inc.

- 5.4.2 Beaver Street Fisheries

- 5.4.3 High Liner Foods Inc.

- 5.4.4 Inland Seafood Inc.

- 5.4.5 Mowi ASA

- 5.4.6 NH Foods Ltd

- 5.4.7 Sysco Corporation

- 5.4.8 Thai Union Group PCL

- 5.4.9 The Kraft Heinz Company

- 5.4.10 Trident Seafood Corporation

6 KEY STRATEGIC QUESTIONS FOR SEAFOOD INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.