Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692033

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692033

Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 537 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

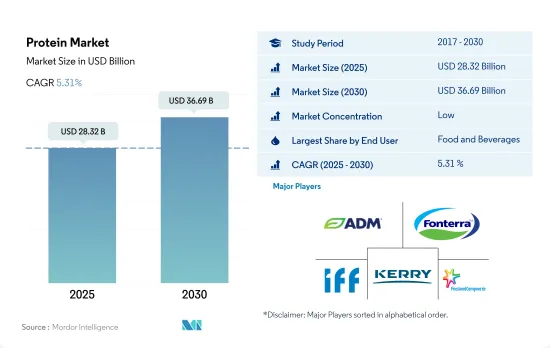

The Protein Market size is estimated at 28.32 billion USD in 2025, and is expected to reach 36.69 billion USD by 2030, growing at a CAGR of 5.31% during the forecast period (2025-2030).

Sustainable alternative protein sources boosting market demand with applications mostly in the food and beverages segment

- Both in terms of value and volume, food and beverages remained the dominant end-user segment of the market in 2023. The demand was mainly led by dairy and meat alternative applications, with consumers demanding plant-based protein-rich alternatives. In 2023, the meat and dairy alternatives industries together held a share of 40.74% by value. The high preference for plant protein has consumers shifting away from meat, which is a major driving factor for the demand. As of 2023, 2.6 million people in Europe were vegan, representing 3.2% of the European population. They were seeking meat and dairy alternatives with higher protein content.

- The food and beverage segment was closely followed by the animal feed segment in terms of applications of plant protein types. The plant protein type holds an 89% share by value among all other proteins used in the animal feed segment. It offers numerous advantages over milk substitutes and fish meals, like better protein digestibility, a favorable amino acid profile, and long shelf life. The segment is anticipated to register a value CAGR of 4.64% from 2024 to 2029.

- In terms of growth, the personal care and cosmetics segment outpaced other segments and is expected to record a CAGR of 6.41% by value from 2024 to 2029 due to increased interest in clean and natural personal care products. Proteins are used in a range of cosmetics products, including gels, shampoos, conditioners, and creams. Proteins naturally found in the body, such as collagen, elastin, and keratin, are also gaining popularity, considering their higher efficacy in naturally strengthening skin and hair. Protein ingredients have proven effects on skin and hair, which is boosting their demand in the personal care and cosmetics segment.

The increasing demand for plant-based meats is fueling the consumption of protein in North America

- Consumers are looking for healthier snack alternatives, giving a larger landscape for the growth of protein-fortified foods. Around 60% of global consumers were more aware of mindful snacking in 2023 (up 4% points from the prior year), while 61% always looked for healthier alternatives to snacks (up 7% points). Across North America, Latin America, Europe, and Asia, a healthier lifestyle is the predominant reason for opting for better-for-you snacks.

- North America remained the largest consumer of protein across the world, largely driven by the United States. The rising production of various raw materials for protein ingredients and changing consumer perceptions impact the market. For instance, the United States produced about 226.6 billion pounds of milk for human consumption in 2023.

- Asia-Pacific was the second-largest market in 2023, driven by consumer demand for diverse protein sources. The shift in consumer preferences toward plant-based options had a significant impact. It had an abundant supply of raw materials required for plant protein production, making it a relatively cost-effective option for manufacturers and consumers. Asia-Pacific is projected to register a value CAGR of 5.42% during 2024-2029.

- The Middle East is projected to be the fastest-growing market, as the demand for natural and sustainable ingredients is rapidly growing due to the rise in health consciousness. The region is set to record a CAGR of 5.57% by volume during 2024-2029. This is attributed to shifting consumer preferences toward more health-, immunity-boosting, less processed, and 'free-from' food products. In 2022, approximately 25% of Arab millennials sought convenient and easily accessible food products.

Global Protein Market Trends

Consumption and usage of animal protein in cosmetics and nutricosmetics are supporting the market's growth globally

- Global consumption of animal protein is experiencing substantial growth, with dairy products representing a significant and expanding segment. Increasing awareness about the health benefits of dairy proteins, especially among athletes, is fueling global per capita animal protein consumption. For instance, in India, from 2022 to 2023, a considerable population of 37% of Indian consumers reported an average daily milk intake of 1.5 to 2 liters, while a further 10% consumed over 3 liters per day. These figures highlight the high per capita consumption levels in certain regions and underscore the substantial demand for animal protein globally.

- Further, the global consumption of animal protein remains significant, with poultry representing a major component. For instance, protein availability from beef, pork, poultry, and sheep meat is projected to grow by 5.9%, 13.1%, 17.8%, and 15.7%, respectively, by 2030. This substantial volume growth highlights the scale of global demand for animal-based protein sources and the poultry industry's considerable role in meeting this demand. Furthermore, beef, pork, and poultry are substantially consumed, highlighting animal protein consumption patterns.

- Beyond traditional food applications, the increasing demand for animal-derived proteins, like collagen and gelatin, from the pharmaceutical, personal care, and nutraceutical industries is significantly boosting the market's growth. For instance, proteins like collagen and gelatin are extensively used in cosmetics and nutraceuticals. Owing to the rising demand for collagen and gelatin animal proteins in different applications, they are anticipated to register a CAGR of 6.07% and 4.70%, respectively, during the forecast period.

Dairy ingredients play a significant role in supplying animal protein raw materials

- Whey and casein protein production primarily hinges on supply from cheese production plants, as these proteins are major byproducts of cheese. For caseins and caseinates, a price point of approximately USD 2.40 per pound is essential to motivate domestic plants to shift fluid skim milk from non-fat dry milk production to casein production. Between 2023 and 2024, global cheese production reached 22.2 million metric tons, influencing the production landscape for dairy proteins like casein, caseinates, and whey proteins. The United States produced 5,584,857 tons of cheese annually, leading the world.

- In the United States, milk ingredient manufacturers have increasingly specialized in milk protein production and witnessed a doubling in production in 2023, spurred by the introduction of micellar casein concentrate ingredients. Micellar casein, with its 90% undenatured protein content and elevated bioavailable calcium levels, is expected to achieve notable market penetration between 2019-2029. The rising demand for dairy-based proteins is largely attributed to the search for ingredients with higher protein concentrations.

- Pork, known for its amino acid profile, is the raw material for gelatin production. France, with an annual production of 23 million pigs, plays a pivotal role. The nation's meat processing industry, employing over 100,000 professionals, ranks as Europe's second-largest. Following pork, buffalo and cattle emerge as key raw materials, bolstering gelatin and collagen protein production. India has the global lead in cattle and buffalo numbers and reported its national cattle herd at 307.6 million head in 2023, a slight increase from the USDA's estimate of 307.5 million head.

Protein Industry Overview

The Protein Market is fragmented, with the top five companies occupying 23.09%. The major players in this market are Archer Daniels Midland Company, Fonterra Co-operative Group Limited, International Flavors & Fragrances Inc., Kerry Group PLC and Royal FrieslandCampina N.V (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90237

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.2.2 Plant

- 3.3 Production Trends

- 3.3.1 Animal

- 3.3.2 Plant

- 3.4 Regulatory Framework

- 3.4.1 Australia

- 3.4.2 Brazil and Argentina

- 3.4.3 Canada

- 3.4.4 China

- 3.4.5 France

- 3.4.6 Germany

- 3.4.7 India

- 3.4.8 Italy

- 3.4.9 Japan

- 3.4.10 South Africa

- 3.4.11 UAE and Saudi Arabia

- 3.4.12 United Kingdom

- 3.4.13 United States

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Source

- 4.1.1 Animal

- 4.1.1.1 By Protein Type

- 4.1.1.1.1 Casein and Caseinates

- 4.1.1.1.2 Collagen

- 4.1.1.1.3 Egg Protein

- 4.1.1.1.4 Gelatin

- 4.1.1.1.5 Insect Protein

- 4.1.1.1.6 Milk Protein

- 4.1.1.1.7 Whey Protein

- 4.1.1.1.8 Other Animal Protein

- 4.1.2 Microbial

- 4.1.2.1 By Protein Type

- 4.1.2.1.1 Algae Protein

- 4.1.2.1.2 Mycoprotein

- 4.1.3 Plant

- 4.1.3.1 By Protein Type

- 4.1.3.1.1 Hemp Protein

- 4.1.3.1.2 Pea Protein

- 4.1.3.1.3 Potato Protein

- 4.1.3.1.4 Rice Protein

- 4.1.3.1.5 Soy Protein

- 4.1.3.1.6 Wheat Protein

- 4.1.3.1.7 Other Plant Protein

- 4.1.1 Animal

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Region

- 4.3.1 Africa

- 4.3.1.1 By Source

- 4.3.1.2 By End User

- 4.3.1.3 By Country

- 4.3.1.3.1 Nigeria

- 4.3.1.3.2 South Africa

- 4.3.1.3.3 Rest of Africa

- 4.3.2 Asia-Pacific

- 4.3.2.1 By Source

- 4.3.2.2 By End User

- 4.3.2.3 By Country

- 4.3.2.3.1 Australia

- 4.3.2.3.2 China

- 4.3.2.3.3 India

- 4.3.2.3.4 Indonesia

- 4.3.2.3.5 Japan

- 4.3.2.3.6 Malaysia

- 4.3.2.3.7 New Zealand

- 4.3.2.3.8 South Korea

- 4.3.2.3.9 Thailand

- 4.3.2.3.10 Vietnam

- 4.3.2.3.11 Rest of Asia-Pacific

- 4.3.3 Europe

- 4.3.3.1 By Source

- 4.3.3.2 By End User

- 4.3.3.3 By Country

- 4.3.3.3.1 Belgium

- 4.3.3.3.2 France

- 4.3.3.3.3 Germany

- 4.3.3.3.4 Italy

- 4.3.3.3.5 Netherlands

- 4.3.3.3.6 Russia

- 4.3.3.3.7 Spain

- 4.3.3.3.8 Turkey

- 4.3.3.3.9 United Kingdom

- 4.3.3.3.10 Rest of Europe

- 4.3.4 Middle East

- 4.3.4.1 By Source

- 4.3.4.2 By End User

- 4.3.4.3 By Country

- 4.3.4.3.1 Iran

- 4.3.4.3.2 Saudi Arabia

- 4.3.4.3.3 United Arab Emirates

- 4.3.4.3.4 Rest of Middle East

- 4.3.5 North America

- 4.3.5.1 By Source

- 4.3.5.2 By End User

- 4.3.5.3 By Country

- 4.3.5.3.1 Canada

- 4.3.5.3.2 Mexico

- 4.3.5.3.3 United States

- 4.3.5.3.4 Rest of North America

- 4.3.6 South America

- 4.3.6.1 By Source

- 4.3.6.2 By End User

- 4.3.6.3 By Country

- 4.3.6.3.1 Argentina

- 4.3.6.3.2 Brazil

- 4.3.6.3.3 Rest of South America

- 4.3.1 Africa

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Archer Daniels Midland Company

- 5.4.2 Arla Foods amba

- 5.4.3 Bunge Limited

- 5.4.4 Cargill Incorporated

- 5.4.5 Corbion Biotech, Inc.

- 5.4.6 Darling Ingredients Inc.

- 5.4.7 Fonterra Co-operative Group Limited

- 5.4.8 FUJI OIL HOLDINGS INC.

- 5.4.9 Gelita AG

- 5.4.10 Glanbia PLC

- 5.4.11 Groupe LACTALIS

- 5.4.12 Hilmar Cheese Company, Inc.

- 5.4.13 Ingredion Incorporated

- 5.4.14 International Flavors & Fragrances Inc.

- 5.4.15 Kerry Group PLC

- 5.4.16 Roquette Frere

- 5.4.17 Royal FrieslandCampina N.V

- 5.4.18 Sudzucker AG

- 5.4.19 Wilmar International Ltd

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.