Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690964

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690964

North America Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 335 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

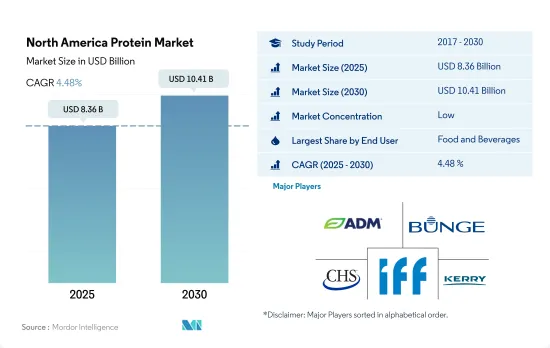

The North America Protein Market size is estimated at 8.36 billion USD in 2025, and is expected to reach 10.41 billion USD by 2030, growing at a CAGR of 4.48% during the forecast period (2025-2030).

The food and beverage segment dominates due to a strong demand from the dairy and dairy alternatives and supplements sub-segments

- The food and beverage segment dominates the market due to the growing need for whey, wheat, and pea proteins in food and beverage products. Due to the extensive use of soy-based plant protein, the dairy and meat alternatives sub-segments continued to hold leading positions. Together, the two sub-segments made up around 60% of the total volume of the food and beverage segment in the region in 2022. Since soy can replicate muscle texture when stacked into linear fibers, soy protein leads the protein market. Due to this property, it is highly used for high-moisture extrusion, gelling, and protein fortification. To produce the requisite anisotropic product structure, these meat analogs are extruded at high moisture contents (>40%) and elevated temperatures above 100 °C.

- Animal feed is the second-largest segment due to the expansion of livestock production and the adoption of advanced animal nutrition technologies. The market potential for animal feed is further expanded by the introduction of sustainable alternative protein sources like insect protein. In 2022, North America held the highest share in the global compound feed production, i.e., approximately 261 million ton and a share of 20.6%.

- Personal care and cosmetics is the fastest-growing segment, and it is projected to register a CAGR of 6.42% by value during 2024-2029. In the United States, 6.8 million people suffer from hair problems such as alopecia areata. Collagen peptides, which are the hydrolyzed form of collagen, nourish the hair bulbs and strengthen the hair follicles by fostering the ideal conditions for healthy hair growth. OGX Biotin & Collagen Shampoo, Salcoll Collagen Hair Mist, Hair La Vie Foundation Collagen Elixir, etc., are a few examples of hair care products containing collagen.

The United States holds a majority share of the market due to the strong presence of various food manufacturing units

- The North American protein market witnessed a favorable growth rate of 10.49% in terms of sales value from 2020 to 2023. The United States led the market due to high product consolidation and an active competitive landscape. Companies are strengthening their presence in the country by acquiring small firms, ramping up protein production units, and expanding their product portfolios. Companies such as Agropur, Anchor Ingredients, and Hilmar Cheese boosted their production capabilities over the review period. Thus, constant product developments and differentiation in the market further resulted in additional sales by volume.

- Canada remained the second-largest market in 2023, driven by consumers pushing for diversification of protein sources. Animal proteins are being replaced by new functional foods and value-added products that are created by the booming plant-protein industry. In 2021, more than 40% of people in Canada actively strived to increase their consumption of plant-based foods. The popularity of plant-based protein sources recently increased due to their suitability for vegetarian, vegan, and "flexitarian" lifestyles.

- Mexico is likely to be the fastest-growing market, with a projected volume CAGR of 6.31% from 2024 to 2029. The Mexican market is dominated by the demand for plant proteins in the country, and it is anticipated to register a CAGR of 6.51% by volume from 2024 to 2029. Due to the rising awareness among Mexican consumers about food safety, environmental sustainability, and animal welfare aspects of meat, a significant portion of the country observed a shift from animal protein products to plant-based protein products.

North America Protein Market Trends

The consumption growth of animal protein is fueling opportunities for key players in the ingredients segment

- Despite the rising vegan population, the demand for animal protein has been steady in the United States. The majority of protein in the American diet comes from beef and poultry, followed by dairy. In 2022, 80% of US adult consumers preferred pork, beef, poultry, and fish as their main protein sources. Due to its water-binding properties, the market is majorly driven by the growing usage of gelatin in the functional food industry.

- Consumers continue to demand traditional protein options, but they are signaling an expectation of the animal protein industry to do more to address environmental concerns. With a wide range of applications and consumer preferences toward a healthy lifestyle, many US ingredient manufacturers are trying to enter the collagen market, which is the major reason for the increase in per capita consumption patterns. From 2019 to 2021, the unadjusted prevalence of doctor-diagnosed arthritis in the United States was 24.2% among women and 17.9% among men. Owing to the prevalence of arthritis in the region, there is an increasing demand for collagen-based supplements for bone and joint health.

- Value-added dairy products drive the per capita consumption of milk protein in Canada. Fluid milk, cheese, cream, and yogurt are the dairy products mainly consumed in the country. In 2022, domestic cow milk consumption amounted to 10,243 thousand MT. The marketing year 2022-2023 sales data indicated that Canadians spent more on whole milk (3.25 % butterfat), less skim milk (0% butterfat), and reduced-fat milk. Canadians eat a moderate amount of red meat. Per capita consumption of beef and poultry is high in Canada compared to pig meat and sheep meat.

Meat and milk production contribute majorly as raw materials for animal protein ingredients

- The graph given depicts the production data for raw materials such as meat of cattle, pigs, and chicken (with bone, fresh or chilled), raw milk from cattle and goats, skim milk from cows, and dry whey powder. In 2023, 2,408,7 pounds of milk was produced per cow, an increase of 1.30% from 23,777 pounds in 2020. As of 2022, the average number of milk cows in the United States was 9,402. Milk is usually separated through various processes into components and processed into fluid beverage milk or the manufacture of other dairy products.

- The United States is the world's largest producer of chicken meat and accounted for a 20% share of global chicken meat production in 2023. Cattle meat is one of the most common sources of collagen, providing a significant amount of this unique protein. With the largest fed-cattle industry in the world, the United States is also the world's largest producer of cattle meat, primarily high-quality, grain-fed cattle meat for domestic and export use.

- Nearly 70% of Canada's milk production is concentrated in Quebec and Ontario. Milk produced in Canada supplies two markets: the fluid milk market, which includes fluid milk for direct consumption, creams, and flavored milk, and the industrial milk market. FAS/Canada forecasts total milk production to reach 10.310 million metric tons (MMT) in 2024, a modest increase from the 2023 estimate of 10.265 MMT. Canada's meat processing companies manufacture a wide variety of meat products, ranging from fresh and frozen meat to processed, smoked, canned, and cooked meats. About 70% of processed meats in Canada, such as sausages or cold cuts, are made with pork.

North America Protein Industry Overview

The North America Protein Market is fragmented, with the top five companies occupying 34.85%. The major players in this market are Archer Daniels Midland Company, Bunge Limited, CHS Inc., International Flavors & Fragrances, Inc. and Kerry Group PLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90056

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.2.2 Plant

- 3.3 Production Trends

- 3.3.1 Animal

- 3.3.2 Plant

- 3.4 Regulatory Framework

- 3.4.1 Canada

- 3.4.2 United States

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Source

- 4.1.1 Animal

- 4.1.1.1 By Protein Type

- 4.1.1.1.1 Casein and Caseinates

- 4.1.1.1.2 Collagen

- 4.1.1.1.3 Egg Protein

- 4.1.1.1.4 Gelatin

- 4.1.1.1.5 Insect Protein

- 4.1.1.1.6 Milk Protein

- 4.1.1.1.7 Whey Protein

- 4.1.1.1.8 Other Animal Protein

- 4.1.2 Microbial

- 4.1.2.1 By Protein Type

- 4.1.2.1.1 Algae Protein

- 4.1.2.1.2 Mycoprotein

- 4.1.3 Plant

- 4.1.3.1 By Protein Type

- 4.1.3.1.1 Hemp Protein

- 4.1.3.1.2 Pea Protein

- 4.1.3.1.3 Potato Protein

- 4.1.3.1.4 Rice Protein

- 4.1.3.1.5 Soy Protein

- 4.1.3.1.6 Wheat Protein

- 4.1.3.1.7 Other Plant Protein

- 4.1.1 Animal

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.3.4 Rest of North America

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Agropur Dairy Cooperative

- 5.4.2 Archer Daniels Midland Company

- 5.4.3 Arla Foods amba

- 5.4.4 Bunge Limited

- 5.4.5 CHS Inc.

- 5.4.6 Darling Ingredients Inc.

- 5.4.7 Farbest-Tallman Foods Corporation

- 5.4.8 Fonterra Co-operative Group Limited

- 5.4.9 Gelita AG

- 5.4.10 Glanbia PLC

- 5.4.11 Groupe Lactalis

- 5.4.12 International Flavors & Fragrances, Inc.

- 5.4.13 Kerry Group PLC

- 5.4.14 MGP

- 5.4.15 Milk Specialties Global

- 5.4.16 Roquette Freres

- 5.4.17 Sudzucker Group

- 5.4.18 Tessenderlo Group

- 5.4.19 The Scoular Company

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.