Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683503

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683503

Middle East Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 286 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

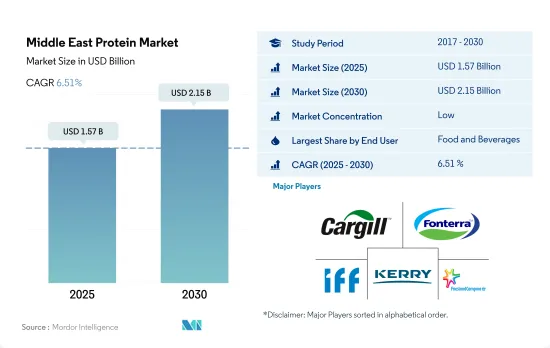

The Middle East Protein Market size is estimated at 1.57 billion USD in 2025, and is expected to reach 2.15 billion USD by 2030, growing at a CAGR of 6.51% during the forecast period (2025-2030).

The rising number of flexitarian consumers drives demand for proteins from the F&B segment

- The food and beverage segment led the application of proteins in the region, accounting for major volume and value shares. The shares were highly influenced by the dairy, beverages, and bakery industries, which together accounted for more than 40% of the value share of the overall proteins consumed in the Middle East in 2023. This share was primarily driven by the rising demand for functional ingredients, particularly protein, in the food and beverage segment.

- The food and beverage segment is followed by the animal feed segment, which is largely driven by the application of plant proteins. The inclusion of sustainable plant protein sources, mainly soy and wheat proteins, drives the segment significantly due to their health benefits, excellent digestibility, and neutral flavor profile. Hence, pea protein has opportunities for wide applications in animal feed and is anticipated to be the fastest-growing plant protein type in the animal feed segment, with a CAGR of 5.46% by value during 2024-2029.

- The personal care and cosmetics segment is the fastest-growing, with a projected CAGR of 7.03% by value during 2024-2029. Proteins are used in a range of cosmetics products, including emulsions, gels, shampoos, conditioners, and creams. Proteins such as collagen, elastin, and keratin are also gaining popularity due to their higher efficacy in naturally strengthening the skin and hair texture. Companies like Estee Lauder, Neu Cosmetics DMCC, and Guerlain are increasingly investing in R&D to develop more effective and sustainable alternative protein sources. Such factors are boosting the ingredient scope and applications of protein in personal care products, which may aid the growth of the market in the future.

With more than half of its population consuming protein supplements, Saudi Arabia held the maximum share of the region's protein market

- One of the region's most important dietary and consumer trends is the shift toward plant-based, flexitarian, or reducetarian diets, resulting in the highest share of plant proteins. Plant proteins accounted for an applicational volume of around 82% in 2023.

- Saudi Arabia led the market in 2023. The food and beverage and animal feed segments held volume shares of 53% and 40%, respectively, in 2023, contributing to the market's growth. This growth was due to Saudi Arabia's high level of product integration and fiercely competitive environment. Companies are strengthening their domestic presence by acquiring small businesses, thereby expanding their protein production units and product portfolios.

- The rise in active lifestyles in Saudi Arabia is anticipated to increase protein consumption. In 2021, 48.2% of people across Saudi Arabia engaged in physical and sporting activities for at least 30 minutes per day. About 50% of physically active people consumed protein supplements in 2020. About 56.1% of active people consume protein supplements to gain muscles, followed by 28.6% of people using protein supplements to compensate for protein deficiency.

- Iran is also one of the prominent protein markets in the region. It is projected to register the fastest CAGR of 8.61% in terms of value during 2024-2029. Plant protein dominated the Iranian market, driven by the demand from the food and beverage and animal feed segments.

- The United Arab Emirates is another key protein market in the region, led by soy protein. Soy protein accounted for 53.97% of the value share of the UAE protein market in 2023. Soy protein is primarily driven by the animal feed and food and beverage segments.

Middle East Protein Market Trends

The inclination toward a protein-rich diet supports growing consumption

- In the Middle East, Saudi Arabia emerged as the dominant player, commanding over 70% of the region's dairy market. This stronghold is propelled by a confluence of factors: a surging appetite for dairy products, a growing health-conscious consumer base, and a heightened interest in sports and nutrition, especially among the younger demographic. Whey snacks, with their diverse flavors, nutritional benefits, portability, and longer shelf life, are carving a niche as a favored snack choice. They appeal not only to millennials seeking quick bites but also to seniors eyeing protein-rich diets.

- Across the Middle East, a rising emphasis on sports nutrition and supplements is evident. The proliferation of fitness centers, equipped with cutting-edge facilities and personalized training, is luring in more consumers. In the UAE, obesity rates are strikingly high, with approximately 70% of men and 67% of women over 15 falling into this category. The region's heightened focus on sports nutrition, which now constitutes 70% of the market, is a direct response to combatting this obesity trend.

- The UAE stands out for its robust appetite for collagen-infused functional foods and beverages. Energy and beauty drinks, enriched with high-protein collagen peptides, are gaining traction, not just in the UAE but also in neighboring markets like Tunisia and Algeria. These beverages are increasingly viewed as alternatives to traditional leisure drinks, thanks to their elevated caffeine content. Noteworthy is the UAE's reliance on imports, sourcing collagen predominantly from Japan and Australia, with a notable preference for sheep-based variants. Meanwhile, in Saudi Arabia, a rising trend is observed: a surge in supplement consumption, especially among those frequenting fitness centers.

GCC countries to focus more on increasing production capabilities of milk and meat

- In the Middle East, the production of various raw materials, including fresh or chilled meat of chickens, pigs, and cattle, along with raw milk from cattle and goats, skim milk from cows, and derivatives like whey, was depicted in the graph. Specifically, the United Arab Emirates stood out, producing 164,934 TT of milk in 2020. The country's milk output saw a significant uptick, hitting 164,934 TT in 2020. Notably, its annual growth rate, which peaked at 22.05% in 2009, tapered off to 1.06% by 2020. Challenges like harsh climates and nascent cold chain technology in the region hamper this segment's growth.

- Overcoming these hurdles requires not only embracing cutting-edge dairy farming tech but also implementing key herd and farm management practices. Bulk orders secure the best prices for dairy products. In 2020, the growth rate of animal protein surged to 10%, doubling the historical 5-year average of 5%. Additionally, by utilizing meat and marine industry waste, animal proteins like collagen and gelatin are produced. However, it's worth noting that slaughterhouses in the Middle East have garnered a poor reputation among animal welfare advocates.

- Live animal exports to the Middle East have seen a steady climb over the last two decades, with Europe and Australia being notable contributors. For instance, in 2019, Western Australia shipped 1.0 million live sheep to nine countries, predominantly in the Middle East, fetching a value of AUD 136 million. Among these, Kuwait, Qatar, and Jordan emerged as the top importers, accounting for 35%, 25%, and 19% of the volume, respectively. This surge in demand is largely attributed to the region's increasing appetite for meat and dairy, coupled with the mounting pressure from a warming climate in these water-stressed nations.

Middle East Protein Industry Overview

The Middle East Protein Market is fragmented, with the top five companies occupying 15.13%. The major players in this market are Cargill, Incorporated, Fonterra Co-operative Group Limited, International Flavors & Fragrances Inc., Kerry Group PLC and Royal FrieslandCampina NV (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90217

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.2.2 Plant

- 3.3 Production Trends

- 3.3.1 Animal

- 3.3.2 Plant

- 3.4 Regulatory Framework

- 3.4.1 UAE and Saudi Arabia

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Source

- 4.1.1 Animal

- 4.1.1.1 By Protein Type

- 4.1.1.1.1 Casein and Caseinates

- 4.1.1.1.2 Collagen

- 4.1.1.1.3 Egg Protein

- 4.1.1.1.4 Gelatin

- 4.1.1.1.5 Insect Protein

- 4.1.1.1.6 Milk Protein

- 4.1.1.1.7 Whey Protein

- 4.1.1.1.8 Other Animal Protein

- 4.1.2 Microbial

- 4.1.2.1 By Protein Type

- 4.1.2.1.1 Algae Protein

- 4.1.2.1.2 Mycoprotein

- 4.1.3 Plant

- 4.1.3.1 By Protein Type

- 4.1.3.1.1 Hemp Protein

- 4.1.3.1.2 Pea Protein

- 4.1.3.1.3 Potato Protein

- 4.1.3.1.4 Rice Protein

- 4.1.3.1.5 Soy Protein

- 4.1.3.1.6 Wheat Protein

- 4.1.3.1.7 Other Plant Protein

- 4.1.1 Animal

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Iran

- 4.3.2 Saudi Arabia

- 4.3.3 United Arab Emirates

- 4.3.4 Rest of Middle East

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Cargill, Incorporated

- 5.4.2 Croda International Plc

- 5.4.3 Fonterra Co-operative Group Limited

- 5.4.4 Hilmar Cheese Company Inc.

- 5.4.5 International Flavors & Fragrances Inc.

- 5.4.6 Kerry Group PLC

- 5.4.7 Lactoprot Deutschland GmbH

- 5.4.8 MEGGLE GmbH & Co.KG

- 5.4.9 Prolactal

- 5.4.10 Royal FrieslandCampina NV

- 5.4.11 Wilmar International Ltd

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.