Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683505

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683505

Africa Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 271 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

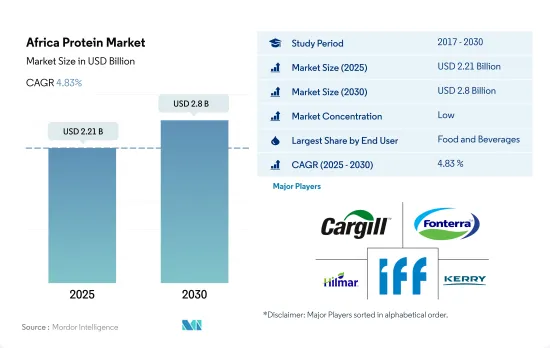

The Africa Protein Market size is estimated at 2.21 billion USD in 2025, and is expected to reach 2.8 billion USD by 2030, growing at a CAGR of 4.83% during the forecast period (2025-2030).

Sustainable alternative protein sources are boosting market demand, with applications mostly in the food and beverages segment

- In 2023, plant proteins accounted for the highest end-user application share (63.35%) in the African protein market. Consumer awareness about global issues, such as climate change and the unsustainability of animal husbandry, is growing. Various celebrities' influence on social media makes plant-based diets popular among the general public. Kenya and Nigeria were among the top 10 countries in the world in terms of growth in their vegetarian populations. Since consumers are actively choosing food and beverages that blur the lines between groceries and medicine, the nutritional quantity of protein in products is increasing. Sales of meat substitutes and milk substitutes are increasing in tandem.

- The animal feed segment accounted for the second-highest share of 48.67% in plant protein applications in 2023. Due to their low cost-in-use, excellent digestibility, and neutral flavor profile, the animal feed segment makes significant use of plant proteins, mainly soy and wheat. The production animal can function at its highest zootechnical level due to the utilization of novel plant protein sources, such as hydrolyzed plant proteins. The personal care and cosmetics segment is expected to grow most during 2019-2029, exhibiting a CAGR of 4.00% by value. Pea protein is the major contributor to this growth as it reduces TEWL and increases skin water content.

- Animal protein application ranks second after plant protein in the market. In 2023, the food and beverage segment emerged as the region's dominant end-use segment for animal protein. The bakery and beverages sub-segments accounted for the highest shares in the food and beverage segment, with 35.88% and 21.87%, respectively, in 2023.

With the rising popularity of plant proteins among Nigerians, the country was the second-largest market contributor to the African protein market

- In 2023, Nigeria emerged as the frontrunner in the African protein market, closely followed by South Africa. This surge in Nigeria's protein market can be attributed to the rising trend of veganism among its populace. Plant-based proteins, particularly soy protein, have gained traction in Nigeria due to their affordability and high protein content. Concurrently, Nigeria's disposable income is on the rise. The national disposable income (NDI) reached USD 136.70 billion in 2023, up from USD 116.72 billion in 2022, with projections indicating this trend will persist through 2029, bolstering the segment's growth.

- Meanwhile, the African market showcased a demand for animal proteins. In 2023, the food and beverage segment commanded a dominant value share of 48.51%. Animal proteins play a pivotal role in forming protein particles within Africa's food industry. Leading the charge in 2023, based on value-added, were Africa's food products, non-metallic mineral products, and beverages industries.

- Plant proteins, commanding a 63.35% value share in 2023, are anticipated to grow at a projected CAGR of 4.02% during 2024-2029, driven by the region's increasing vegetarian population. In 2024, with vegans, vegetarians, and flexitarians making up 10-12% of South Africa's consumer base, national fast-food chains are rapidly integrating plant-based alternatives into their offerings, propelling the segment's expansion.

- Industry players are also making concerted efforts to infuse proteins into a variety of foods, broadening their applications across Africa. For example, in 2023, Arla Foods Ingredients showcased how its whey solutions cater to Africa's surging demand for high-protein products.

Africa Protein Market Trends

Per capita consumption of animal protein to witness significant growth due to growing health awareness and healthy eating habits of consumers

- The graph illustrates Africa's per capita consumption of animal protein. This consumption is propelled by a rising health consciousness and a recent shift toward nutritious eating among consumers. The awareness among parents regarding the nutritional benefits of infant formulas, especially those derived from milk protein, is fueling their consumption. However, the market faces challenges from the increasing adoption of veganism and a notable prevalence of lactose intolerance. Since 2017, the market's growth has been sluggish, attributed in part to shifts in South African legislation, particularly around dietary supplements, which have led to additional certification costs for manufacturers.

- While Sub-Saharan Africa has seen a decline in per capita milk consumption over the past two decades, the consumption of animal protein rose from 88 g in 2017 to 105.7 g in 2022. Given Africa's projected population growth from 1.3 billion to 2.5 billion by 2050, the demand for animal protein is set to rise.

- South African manufacturers have embraced innovative production techniques to gain market cost leadership. Increasing demand from working women for high-quality protein infant formulas and the nutritional needs of athletes are driving growth rates. With a mature and organized retail sector, shelf space for protein products is expected to increase, maintaining a large share in the African region. As a result, consumers are increasingly buying protein bars and supplements to meet their nutritional needs and maintain their health. Changing consumer lifestyles and rising healthcare expenditures also play a vital role in the growth of the plant protein market in Africa.

Meat and milk production are primary sources of raw materials for manufacturers of animal protein ingredients

- The graph illustrates the production of various raw materials across Africa, including fresh or chilled cattle, chicken, and pig meat with bones, raw milk from cattle and goats, cow skim milk, and dry whey. Milk serves as the primary raw material for producing animal proteins like milk proteins, whey proteins, casein, and caseinates. Sudan, Egypt, Kenya, South Africa, and Algeria emerge as the top five milk-producing nations in Africa. West Africa saw a 50% surge in local milk production from 2000 to 2016, reaching approximately 4 billion liters by 2019. The region's growing fitness culture, exemplified by South Africa's 2019 figure of 2.26 million health club members, boosted whey protein production.

- Locally produced milk accounts for 65-70% of consumption, with imported milk powder filling the gap. In 2018, the European Union exported 92,620 tons of milk powder and 276,982 tons of fat-filled milk powder to West Africa. Kenya stands out as East Africa's primary milk producer, with the dairy industry leading the country's agricultural landscape, contributing 4% to its GDP and playing a pivotal role in income generation and employment.

- Based on the records of per capita animal product consumption, the feed required for South Africa was 13.3 million tons in 2021, which is projected to increase further during the forecast period due to the rising demand for insect proteins for animal feed in the region. In Africa, animal proteins like collagen and gelatin are typically sourced from animal and marine waste. Interestingly, pigs stand out by requiring less feed. This not only helps in managing the excess heat generated during digestion and metabolism but also influences their protein content.

Africa Protein Industry Overview

The Africa Protein Market is fragmented, with the top five companies occupying 6.15%. The major players in this market are Cargill Incorporated, Fonterra Co-operative Group Limited, Hilmar Cheese Company Inc., International Flavors & Fragrances, Inc. and Kerry Group plc (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90220

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.2.2 Plant

- 3.3 Production Trends

- 3.3.1 Animal

- 3.3.2 Plant

- 3.4 Regulatory Framework

- 3.4.1 South Africa

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Source

- 4.1.1 Animal

- 4.1.1.1 By Protein Type

- 4.1.1.1.1 Casein and Caseinates

- 4.1.1.1.2 Collagen

- 4.1.1.1.3 Egg Protein

- 4.1.1.1.4 Gelatin

- 4.1.1.1.5 Insect Protein

- 4.1.1.1.6 Milk Protein

- 4.1.1.1.7 Whey Protein

- 4.1.1.1.8 Other Animal Protein

- 4.1.2 Microbial

- 4.1.2.1 By Protein Type

- 4.1.2.1.1 Algae Protein

- 4.1.2.1.2 Mycoprotein

- 4.1.3 Plant

- 4.1.3.1 By Protein Type

- 4.1.3.1.1 Hemp Protein

- 4.1.3.1.2 Pea Protein

- 4.1.3.1.3 Potato Protein

- 4.1.3.1.4 Rice Protein

- 4.1.3.1.5 Soy Protein

- 4.1.3.1.6 Wheat Protein

- 4.1.3.1.7 Other Plant Protein

- 4.1.1 Animal

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Nigeria

- 4.3.2 South Africa

- 4.3.3 Rest of Africa

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Amesi Group

- 5.4.2 Cargill Incorporated

- 5.4.3 Fonterra Co-operative Group Limited

- 5.4.4 Hilmar Cheese Company Inc.

- 5.4.5 International Flavors & Fragrances, Inc.

- 5.4.6 Kerry Group plc

- 5.4.7 Lactoprot Deutschland GmbH

- 5.4.8 Prolactal

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.