Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683501

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683501

South America Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 277 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

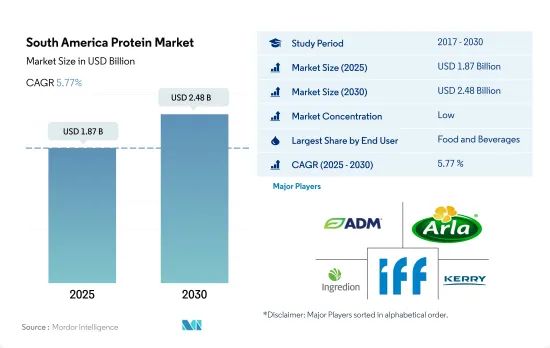

The South America Protein Market size is estimated at 1.87 billion USD in 2025, and is expected to reach 2.48 billion USD by 2030, growing at a CAGR of 5.77% during the forecast period (2025-2030).

With bakery and dairy/dairy alternative products seeing the largest application of protein, the food and beverage segment occupied the leading market share in the region

- In South America, the food and beverage segment stands out as the primary consumer of proteins. Within this segment, bakery, dairy, and dairy-alternative products are pivotal, jointly commanding over 46.8% of the protein market in 2023 within the food and beverages category. Gelatin, known for its protein content, is a transparent gelling and thickening agent, making it a staple in the bakery sub-segment.

- The dairy and dairy-alternative sub-segment is a significant player in the protein landscape, which saw a steady CAGR of 3.90% by value during the forecast period. This growth is fueled by the adoption of casein in cheese production and the prevailing trend of fortifying dairy desserts with proteins. Manufacturers are responding by introducing protein-enhanced versions of popular products like ice creams and yogurts, capitalizing on the "high protein" and "added protein" consumer demands. In this segment, whey protein and milk protein, following casein and caseinates, are the most utilized animal proteins. Their applications extend beyond nutrition, enhancing attributes like mouthfeel, viscosity, and structural integrity.

- Meanwhile, the animal feed segment is emerging as the second-largest consumer of proteins. Plant proteins, especially soy, are expected to witness a robust CAGR of 6.21% by value from 2024 to 2029. Soy's appeal lies in its consistent nutritional profile, making it a preferred choice in animal feed formulations. Soy concentrates, rich in easily digestible amino acids, are particularly favored for chicken pre-starter meals, given their benefits in lipid and water retention. With the region boasting significant soy production, manufacturers are finding it both convenient and cost-effective to pivot toward soy proteins in their animal feed formulations.

Brazil is dominating the South American protein market with growing consumer emphasis on sports nutrition and dietary supplements

- The South American protein market is poised for significant growth, registering a CAGR of 5.31% from 2024 to 2029 by value, primarily driven by increased government support to key application industries. Brazil saw a surge in market accessibility following the National Sanitary Surveillance Agency's (ANIVSA) 2018 regulations on dietary supplements. These changes not only facilitated easier market entry for brands but also fostered an environment for existing brands to thrive and innovate.

- Brazil stands out as the market leader, with a pronounced demand for plant proteins. This heightened demand is largely influenced by Brazil's aging population, which is projected to triple by 2050, encompassing approximately 66 million individuals. With rising health consciousness, consumers are pivoting toward healthier dietary choices. Consequently, the country is expected to outpace its South American counterparts, registering a CAGR of 5.95% from 2024 to 2029. In terms of applications, the food and beverage segment accounts for the most significant share, with bakery, meat/meat alternatives, and dairy/dairy alternatives sub-segments collectively accounting for 77.8% of the segment's demand in 2023.

- Argentina is the second-largest player in the protein market. In Argentina's protein market, plant protein emerged as the fastest-growing segment, capturing a 58.51% value share in 2023. While the country heavily relies on animal-based protein for consumption, the rising preference for diverse diets such as vegan, vegetarian, and flexitarian has led to increased demand for plant proteins in applications like dairy and meat alternatives. In Argentina, the plant-based trend has gained momentum in recent years, with 12% of the population identifying as vegan or vegetarian.

South America Protein Market Trends

Increasing preference for protein rich diet to influence consumption

- The graph illustrates the per capita consumption of animal protein across South American countries. Despite economic challenges, South America is witnessing a growing appetite for health and wellness products. Concerns over mobility-related health issues, such as osteoporosis and joint health, are paramount for consumers. Consequently, collagen manufacturers are increasingly targeting dietary supplement producers to meet this demand. In 2018, Brazil led the region, with health and wellness product consumption exceeding USD 21.7 billion. The region is also grappling with a surge in diseases like cardiovascular issues and diabetes, prompting a shift towards animal-based dietary supplements.

- South American consumers are becoming more cognizant of the link between diet and health, propelling the market's expansion. The sales of protein-rich foods are surging, driven by a heightened appetite for functional and fortified foods. Consumers are showing a clear preference for natural and organic options in their daily diets. Notably, by 2022, Argentina saw a staggering 125% rise in organic packaged food and beverage consumption from 2020.

- Brazilians exhibit a pronounced inclination towards cosmetics, prompting industry players to ramp up investments in collagen and gelatin peptides. These peptides find applications not just in dietary supplements but also in cosmetics. For optimal skin health, Brazilians are advised to consume 2.5 grams of collagen peptides. Alarming health statistics, such as a 16% rise in the mortality rate in 2020 due to issues like rheumatoid arthritis and osteoporosis, underscore the anticipated surge in demand for collagen peptide-based supplements in the coming years.

Milk and meat production contributes majorly as raw material for animal protein ingredients manufacturers

- The graph illustrates the production trends of key raw materials in South America, including cattle and pig meat with bone, fresh or chilled; raw milk from cattle and goats; skim milk from cows; and dry whey powder. Notably, while chicken meat production faced challenges, other animal proteins, like milk proteins, whey proteins, casein, and caseinates, rely heavily on milk as their primary raw material. After a dip in 2019, primarily due to adverse weather and economic conditions, milk production rebounded strongly in 2020. However, this positive momentum is now overshadowed by the uncertainties stemming from the ongoing COVID-19 pandemic. Argentina and Uruguay saw year-to-date growth rates of 8.7% and 3.9%, respectively, in the first half of 2020. Additionally, net importing nations on the Pacific coast, such as Colombia and Chile, also experienced notable production upticks.

- Argentina stands out as a significant milk producer in the region. Yet, the sector faces challenges due to government policies, marked by trade interventionism and a heavy tax burden, leading to operational complexities and reduced investments. Despite these hurdles, Argentina managed a 4% increase in total milk output in 2021 compared to 2020. The region also derives animal proteins like collagen and gelatin from its meat slaughtering activities. Brazil, on the other hand, continues to bolster its beef production, emphasizing investments in production efficiency, disease control, and supply chain transparency. Notably, Brazil's beef productivity surge is largely attributed to a substantial increase in its national herd, which grew by nearly 17 million heads over two decades.

South America Protein Industry Overview

The South America Protein Market is fragmented, with the top five companies occupying 26.67%. The major players in this market are Archer Daniels Midland Company, Arla Foods amba, Ingredion Incorporated, International Flavors & Fragrances, Inc. and Kerry Group plc (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90214

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.2.2 Plant

- 3.3 Production Trends

- 3.3.1 Animal

- 3.3.2 Plant

- 3.4 Regulatory Framework

- 3.4.1 Brazil and Argentina

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Source

- 4.1.1 Animal

- 4.1.1.1 By Protein Type

- 4.1.1.1.1 Casein and Caseinates

- 4.1.1.1.2 Collagen

- 4.1.1.1.3 Egg Protein

- 4.1.1.1.4 Gelatin

- 4.1.1.1.5 Insect Protein

- 4.1.1.1.6 Milk Protein

- 4.1.1.1.7 Whey Protein

- 4.1.1.1.8 Other Animal Protein

- 4.1.2 Microbial

- 4.1.2.1 By Protein Type

- 4.1.2.1.1 Algae Protein

- 4.1.2.1.2 Mycoprotein

- 4.1.3 Plant

- 4.1.3.1 By Protein Type

- 4.1.3.1.1 Hemp Protein

- 4.1.3.1.2 Pea Protein

- 4.1.3.1.3 Potato Protein

- 4.1.3.1.4 Rice Protein

- 4.1.3.1.5 Soy Protein

- 4.1.3.1.6 Wheat Protein

- 4.1.3.1.7 Other Plant Protein

- 4.1.1 Animal

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.3.3 Rest of South America

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Archer Daniels Midland Company

- 5.4.2 Arla Foods amba

- 5.4.3 Bremil Group

- 5.4.4 BRF S.A.

- 5.4.5 Gelnex

- 5.4.6 Ingredion Incorporated

- 5.4.7 International Flavors & Fragrances, Inc.

- 5.4.8 Kerry Group plc

- 5.4.9 Lactoprot Deutschland GmbH

- 5.4.10 Tereos SCA

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.