Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636503

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636503

United Kingdom Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 95 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

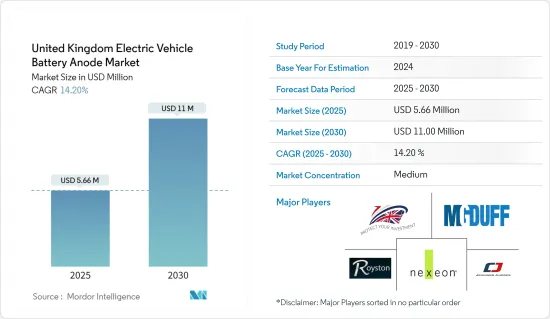

The United Kingdom Electric Vehicle Battery Anode Market size is estimated at USD 5.66 million in 2025, and is expected to reach USD 11.00 million by 2030, at a CAGR of 14.2% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing adoption of electric vehicles due to the government's In the medium term, the market is poised to benefit from the rising adoption of electric vehicles, spurred by the government's ambitious targets and corresponding investments.

- However, challenges such as land costs, logistics for raw materials, and the absence of subsidies for battery manufacturing may hinder the market's expansion.

- Ongoing research and development in anode materials present promising growth avenues for the market.

United Kingdom Electric Vehicle Battery Anode Market Trends

Lithium Ion Batteries to Dominate the Market

- Lithium-ion batteries are at the forefront of the electric vehicle (EV) revolution. Their superior energy density and extended life cycle make them pivotal as the automotive industry pivots towards sustainable energy solutions. In the United Kingdom, research and development in the lithium-ion battery sector is gaining momentum.

- In September 2023, the Faraday Institution, the United Kingdom's premier institute for electrochemical energy storage research, announced a USD 21 million investment spread across four key battery research projects, with a focus on lithium-ion initiatives. These investments are poised to bolster future demand for anode manufacturing.

- Furthermore, the United Kingdom is drawing in major players to tap into its lithium deposits, a move anticipated to bolster domestic lithium-ion battery production. For example, in June 2023, French multinational Imerys S.A., a leader in industrial minerals, secured an 80% stake in British Lithium. This private firm is at the forefront of sustainably extracting battery-grade lithium from mica granite. Their collaboration aims to set up the UK's first integrated producer of battery-grade lithium carbonate.

- Historically, as the prices of lithium-ion batteries have plummeted, the demand for related components, notably anodes, has surged. Bloomberg NEF reported that in 2023, the average price of lithium-ion batteries was USD 139 USD/KWh, marking a staggering fivefold price drop since 2014. This swift adoption, driven by falling prices, bodes well for the anode market's growth.

- Given these trends in lithium-ion batteries and anode production, India's electric vehicle battery anode market is poised for growth in the coming years.

Government Support to Raise Adoption of Electric Vehicles

- The United Kingdom government has set an ambitious goal to achieve net-zero carbon emissions by 2050, with a particular focus on reducing emissions from the transportation sector. According to the Department for Energy Security & Net-Zero, domestic transport accounted for approximately 29.1% of greenhouse gas emissions, making it the largest contributor among various sectors. In light of this, the UK's push for electric vehicles is anticipated to drive up the demand for battery components, especially anodes, in the coming years.

- For instance, in January 2024, the government introduced a zero-emission vehicle (ZEV) mandate aimed at car manufacturers. This initiative seeks to provide manufacturers with greater certainty while broadening the selection of electric vehicles for consumers.

- Furthermore, the mandate stipulates a gradual increase in the sales proportion of zero-emission vehicles (ZEVs) for manufacturers. Beginning with a target of 22% in 2024, the goal rises to 80% by 2030 and reaches a complete 100% by 2035. Meeting these phased targets is set to significantly boost the demand for electric vehicle batteries and their components, like anodes, during the forecast period.

- Additionally, the trend of rising electric vehicle adoption in the United Kingdom is evident. Data from the International Energy Agency reveals that in 2023, the country's electric car sales hit 450,000 units, marking a substantial 21.62% increase from the prior year. Given this trajectory, the demand for electric vehicles in the country is poised for further growth, which in turn is likely to elevate the anode market.

- In conclusion, given the current trends and projections, the UK Electric Vehicle Battery Anode Market is set for an upswing in the foreseeable future.

United Kingdom Electric Vehicle Battery Anode Industry Overview

The United Kingdom electric vehicle battery anode market is semi-consolidated. Some of the major players (not in particular order) include UK Anodes LTD, Jennings Anodes, MG Duff International Ltd, Royston Lead, and Nexeon.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50003832

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government policies supporting adoption of electric vehicles

- 4.5.1.2 Declining Lithium-ion Battery Prices

- 4.5.2 Restraints

- 4.5.2.1 Lack of raw materials and associated resources on the European continent for manufacturing batteries

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lead Acid Batteries

- 5.1.2 Lithium-ion Batteries

- 5.1.3 Other Battery Types

- 5.2 Material

- 5.2.1 Graphite

- 5.2.2 Silicon

- 5.2.3 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 UK Anodes LTD

- 6.3.2 Jennings Anodes

- 6.3.3 MG Duff International Ltd

- 6.3.4 Royston Lead

- 6.3.5 Nexeon Ltd

- 6.3.6 Tata Group

- 6.3.7 DKL Metals Ltd

- 6.3.8 Impalloy Ltd.

- 6.3.9 Nextrode

- 6.3.10 Phillips 66

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Research & Development in anode material

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.