Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636485

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636485

China Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 95 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

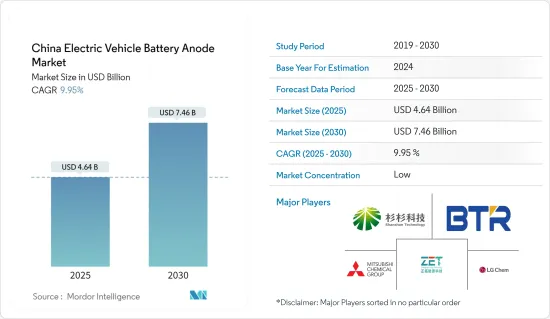

The China Electric Vehicle Battery Anode Market size is estimated at USD 4.64 billion in 2025, and is expected to reach USD 7.46 billion by 2030, at a CAGR of 9.95% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, supportive government policies and investments in battery manufacturing and the decreasing price of lithium-ion batteries are expected to drive the market in the forecast period.

- On the other hand, high production cost for anode materials is expected to restrain market growth in the future.

- Nevertheless, the ongoing research and advancement in anode material and efficient electrolytes may offer opportunities for market growth.

China Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Type is Expected to Have a Major Share

- Initially, lithium-ion batteries primarily powered consumer electronics, including mobile phones and personal computers. However, their application has broadened significantly, making them the dominant power source for hybrid and fully electric vehicles (EVs) in China. This transition is primarily driven by the environmental advantages of EVs, which emit no CO2, nitrogen oxides, or other greenhouse gases.

- Due to their high energy density, cost-effectiveness, and efficiency, lithium-ion batteries have become the preferred choice for electric vehicles (EVs). This growing adoption has spurred a rising demand for anode materials during the manufacturing process.

- Further, the decreasing cost of lithium-ion materials is also a significant reason for the increasing demand for lithium-ion battery manufacturing for electric vehicles. In 2023, the price of lithium-ion battery packs decreased by 14% compared to the previous year to USD139/kWh. As battery prices drop, EVs become more affordable, increasing adoption and a larger market share for electric vehicles. This surge in demand will drive higher consumption of battery components, including the anode, and encourage technological advancements to improve battery performance.

- In the future, as technological innovations enhance the efficiency of lithium-ion batteries in electric vehicles, the demand for anode materials is projected to rise simultaneously.

- For instance, in April 2024, Contemporary Amperex Technology Co., a Chinese electric vehicle manufacturer, launched a lithium iron phosphate (LFP) battery for electric vehicles. The new battery has an energy density of 205 Wh per kg, almost 8% higher than the current state of the art for such batteries. Such developments are expected to boost the demand for EV lithium-ion anode materials in the forecast period.

- Additionally, as per Automotive Industry Green and Low-Carbon Development Roadmap 1.0 developed under the supervision of China's Ministry of Industry and Information Technology, electric car sales in China for passenger new energy vehicle (NEV) is expected to reach a 50% share by 2025. Such roadmaps are expected to raise a futuristic oppotunity for EV anode manufacturing too in China.

- Thus, owing to the increasing use of lithium-ion batteries in electric vehicles and decreasing prices, the lithium-ion battery anode segment is expected to grow significantly in the forecast period.

Government Policies and Investments Towards Battery Manufacturing is Expected to Drive the Market

- A combination of supportive government policies and significant investment in battery production drives China's EV battery manufacturing, which, in turn, is expected to boost the demand for electric vehicle battery anodes. The government offers direct financial support, tax incentives, and subsidies, reducing manufacturers' costs and encouraging investment in advanced equipment. Manufacturers of electric vehicles in China benefit from government subsidies. For instance, all-electric plug-in cars boasting a range exceeding 400 km qualify for a subsidy of RMB 12,600 (around USD 2,000). Meanwhile, those ranging between 300 to 400 km receive a subsidy of RMB 9,100 (approximately USD 1,400).

- Further, the country's increasing demand for electric vehicles is fueling investment in electric vehicle battery manufacturing projects, thereby creating a potential need for electric vehicle battery anode materials. According to the International Energy Agency, in 2023, the demand for electric vehicle batteries in China accounted for 417 GWh, up from 314 GWh last year.

- Moreover, rising electric vehicle sales are motivating battery manufacturing companies to invest more in EV battery production, thereby creating demand for EV battery anode materials. According to the International Energy Agency, in 2023, the country's total EV car sales accounted for 8.1 million, higher than 5.9 million in 2022.

- In the future, the demand for EV battery anode materials is expected to increase as the country rushes towards manufacturing electric vehicles, and investments are expected to grow in EV battery manufacturing. For instance, in May 2024, China announced to invest 845 USD million to develop next-generation battery technology powering electricl vehicles. Such investments will boost the demand for electric vehicle battery manufacturing in the forecast period.

- Thus, supportive government policies and investments in battery manufacturing are expected to drive the market.

China Electric Vehicle Battery Anode Industry Overview

The China electric vehicle battery anode market is semi-fragmented. Some of the major players in the market (in no particular order) include Shanghai Shanshan Technology Co., Ltd., BTR New Material Group Co., Ltd., Jiangxi Zhengtuo New Energy Technology, Mitsubishi Chemical Group., and LG Chemical Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50003754

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Policies and Investments towards battery manufacturing

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 High Production Cost for Anode Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Other Battery Types

- 5.2 Material

- 5.2.1 Lithium

- 5.2.2 Graphite

- 5.2.3 Silicon

- 5.2.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Shanghai Shanshan Technology Co., Ltd.

- 6.3.2 BTR New Material Group Co., Ltd.

- 6.3.3 Jiangxi Zhengtuo New Energy Technology

- 6.3.4 Mitsubishi Chemical Group.

- 6.3.5 Shanghai Putailai New Energy Technology

- 6.3.6 Targray Industries Inc.

- 6.3.7 Ningbo Shanshan Co., Ltd.

- 6.3.8 LG Chemical Group

- 6.3.9 Tokai Carbon Co., Ltd.

- 6.3.10 Resonac Holdings Corporation.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Increasing Research and Development of Other Anode Materials

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.