Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693579

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693579

Europe Military Helicopters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 182 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

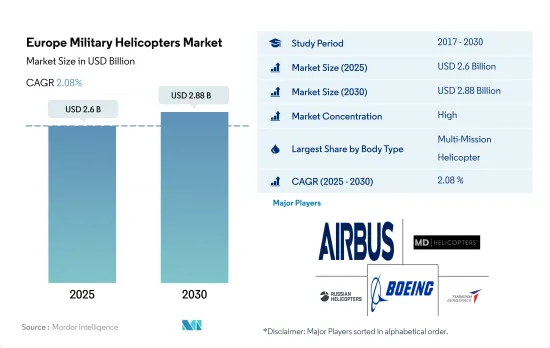

The Europe Military Helicopters Market size is estimated at 2.6 billion USD in 2025, and is expected to reach 2.88 billion USD by 2030, growing at a CAGR of 2.08% during the forecast period (2025-2030).

Multi-mission helicopters hold the highest market share

- The demand for rotorcrafts is being fueled by an increase in military conflicts, terrorism, border disputes, territory breaches, and violations. To gain a military advantage over the opposition, regional armed forces are upgrading the capabilities of helicopters with cutting-edge technologies.

- Ongoing tensions between Russia and Ukraine are encouraging various countries in the region to spend at least 2% of their GDP, which is a NATO standard, on their military. Thus, the countries are opting for the procurement of advanced helicopters to counter threats in an effective way.

- There are currently 3,363 helicopters in operation in Europe. With 1,632 operational helicopter forces, Russia possesses the highest number of helicopters in the region. France and Italy have the largest active fleets, with 478 and 435 helicopters, respectively, after Russia. Multi-mission helicopters are expected to record the highest CAGR during the forecast period. Multi-mission helicopters can be used for close air support for ground troops and anti-tank operations to destroy enemy armor. Multi-mission helicopters account for 38% of the total helicopter active fleet in the region, making it the largest segment, followed by other body types and transport helicopters, accounting for shares of 32% and 30%, respectively.

- More than 1000 helicopters are expected to be procured in Europe over the forecast period, mainly by Germany, France, the United Kingdom, Russia, Italy, Spain, the Netherlands, and the Rest of Europe, which may drive the demand for rotorcrafts in the region.

Factors such as fleet modernization and rising geopolitical tensions are driving the European market

- Europe has a robust and technologically advanced military helicopter market that is driven by various factors, including geopolitical concerns, modernization efforts, and defense budget allocations. The defense budgets of European countries play a crucial role in shaping the military helicopter market. Despite economic challenges, defense spending has remained a priority for many European nations due to rising security concerns. In 2022, Europe spent USD 480 billion on its military, an increase of 13% over 2021. By the end of March 2022, numerous European NATO member nations announced plans to increase military expenditure in reaction to the Russian invasion of Ukraine in February 2022, aiming to meet or exceed the NATO spending target of 2% of GDP or higher.

- During 2017-2022, in terms of fleet procurement, the region procured 20% of the global total fleet. Of these total fleets, the countries that procured most of the fleet were Italy with 33%, followed by Germany with 20%, France and the UK with 13% each, and Spain with 10%.

- Additionally, many European nations are actively engaged in modernizing their military helicopter fleets to meet the evolving security landscape. Upgrading aging platforms with state-of-the-art helicopters enables countries to enhance their operational effectiveness, increase mission versatility, and maintain interoperability with NATO and other allied forces. Germany, France, the United Kingdom, Russia, Italy, Spain, the Netherlands, and the Rest of Europe plan to purchase helicopters from 2023 to 2029. A total of 566 helicopters are expected to be delivered in Europe during the forecast period. During the forecast period, Romania and Hungary also plan to expand their fleet by procuring 60 and 18 helicopters, respectively.

Europe Military Helicopters Market Trends

NATO alliances are contributing to the region's defense spending

- In 2022, Europe spent USD 480 billion on its military, a 13% increase over 2021 and a 38% increase over 2013. In 2022, Europe accounted for 21% of the total defense expenditure in the world. In 2021, Central and Western Europe's combined military expenditure totaled USD 345 billion (USD 305 billion for Western Europe and USD 45 billion for Central Europe), including most NATO allies and all of the EU member states.

- Increased expenditures on military R&D and arms purchases were the main drivers of the surge in military spending in Central and Western Europe. In 2022, defense expenditures in Eastern Europe increased to USD 76.3 billion. In 2022, 19 European NATO member nations, up from five in 2014 and 13 in 2020, dedicated a minimum of 20% of their defense spending to arms purchases and military R&D.

- In 2022, these member states' average proportion of defense spending on weapons and R&D increased to 24% from 22% in 2020 and 14% in 2014. Only two of the 26 NATO members in Europe with a military budget, Albania and Estonia, did not increase the portion of their budgets devoted to arms purchases and R&D from 2014 to 2021. By the end of March 2022, numerous European NATO member nations announced plans to increase military expenditure in response to the Russian invasion of Ukraine in February 2022, aiming to meet or exceed the NATO spending target of 2% of the GDP or higher. Belgium, Denmark, Germany, Lithuania, the Netherlands, Norway, Poland, and Romania were members of this group. These budgets were expected to be centered on the purchase of new armaments.

Fixed-wing aircraft accounted for 54% of the total fleet in the European military aviation market

- As of 2022, there were 8,326 active aircraft in Europe, of which fixed-wing aircraft accounted for 58% and rotorcraft for 42%. The total active aircraft fleet increased by 4% compared to 2016 in the region. Russia, the United Kingdom, the Netherlands, Germany, Italy, Spain, and France accounted for 95% of the total active fleet in the region.

- The fixed-wing aircraft and multi-role aircraft segments accounted for 54%, while transport aircraft, training aircraft, and others accounted for 16%, 23%, and 7%, respectively. In 2021, the active fleet of fixed-wing aircraft decreased by 3% compared to 2016. In rotorcraft, multi-mission helicopters accounted for 38%, while transport helicopters and other helicopters accounted for 30% and 32%, respectively. In 2021, the active fleet of rotorcraft increased by 1% compared to 2016.

- As of 2022, the average age of the Russian aircraft fleet was 10.5 years. The Yakovlev Yak-42 jets had the highest average age of any type of aircraft, at nearly 28 years. During the forecast period, the United Kingdom, Germany, France, Italy, and Spain may continue to build and buy next-generation aircraft to meet the demands of modern warfare. The regional armed forces are also upgrading the capabilities of helicopters with cutting-edge technology to achieve military superiority over possible invaders. The UK Ministry of Defence plans to retire several aging aircraft; however, it needs to actively continue the procurement of replacement aircraft to avoid any gaps within the fleet. The country's continued support for Ukraine in its war with Russia may add pressure on its defense budget. This factor may threaten the country's usual place as Europe's largest defense spender.

Europe Military Helicopters Industry Overview

The Europe Military Helicopters Market is fairly consolidated, with the top five companies occupying 92.25%. The major players in this market are Airbus SE, MD Helicopters LLC., Russian Helicopters, The Boeing Company and Turkish Aerospace Industries (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92729

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Gross Domestic Product

- 4.2 Active Fleet Data

- 4.3 Defense Spending

- 4.4 Regulatory Framework

- 4.5 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Multi-Mission Helicopter

- 5.1.2 Transport Helicopter

- 5.1.3 Others

- 5.2 Country

- 5.2.1 France

- 5.2.2 Germany

- 5.2.3 Italy

- 5.2.4 Netherlands

- 5.2.5 Russia

- 5.2.6 Spain

- 5.2.7 Turkey

- 5.2.8 UK

- 5.2.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 BAE Systems

- 6.4.3 Leonardo S.p.A

- 6.4.4 Lockheed Martin Corporation

- 6.4.5 MD Helicopters LLC.

- 6.4.6 Russian Helicopters

- 6.4.7 The Boeing Company

- 6.4.8 Turkish Aerospace Industries

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.