Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693561

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693561

Middle East and Africa Military Helicopters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 170 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

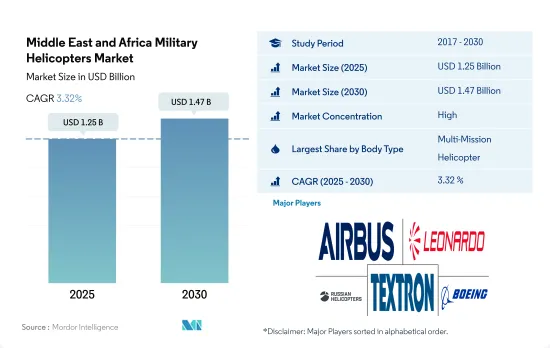

The Middle East and Africa Military Helicopters Market size is estimated at 1.25 billion USD in 2025, and is expected to reach 1.47 billion USD by 2030, growing at a CAGR of 3.32% during the forecast period (2025-2030).

Geopolitical challenges and rising defense budgets are the driving factors of military rotorcraft in the region

- The regional armed forces are modernizing the capabilities of helicopters with cutting-edge technologies to gain a military edge. During the forecast period, multi-mission helicopters are expected to hold the major share of the market. Multi-mission helicopters can provide close air support to ground troops and conduct anti-tank operations to destroy enemy armor. The armed forces in the region require these capabilities, aiding the procurement of multi-mission helicopters.

- There are currently 3,118 combat helicopters in operation in the Middle East & Africa. With a 474-helicopter operational force, Turkey possesses the most combat helicopters in the region. Egypt and Algeria have active fleets of 313 and 276 combat helicopters, respectively, after Turkey.

- Turkey, Algeria, and Egypt are anticipated to purchase most of the helicopters throughout the forecast period. Egypt plans to buy 24 EW-149 multi-mission helicopters by 2024. By 2024, Algeria plans to purchase 42 Mi-28 attack helicopters. Around 160 helicopters will likely be purchased by Turkey, including 109 S-70 utility helicopters. By 2026, all the helicopters are expected to be delivered.

- Earlier in 2018, the United Arab Emirates signed a USD 242 million contract with The Boeing Company for the procurement of 17 Apache AH-64E attack helicopters, which are expected to be delivered by 2023. Turkey is currently developing a new T629 attack helicopter, with a total displacement of six tons, lighter than its T129 ATAK predecessor. By the second half of 2020, Turkish Aerospace Industries started delivering ATAK FAZ 2 helicopters.

The demand for fleet upgradation and fleet replacement programs for the growing aging fleet is expected to aid the market growth

- The defense expenditure in the Middle East was around USD 184 billion in 2022, with a decline of over 3.2% compared to 2022. It was around USD 39.4 billion in Africa in 2022, with a decline of over 5% from 2021.

- The Gulf region continues to be fragmented due to geographic tensions between the countries in the region. Saudi Arabia, Egypt, Qatar, the UAE, and Algeria are the major arms importers globally. They also have active programs for procuring combat and utility helicopters in the rotorcraft segment. These countries are expected to procure newer rotorcraft for fleet upgradation during the forecast period.

- In 2022, the rotorcraft accounted for 41% of the overall aircraft deliveries in the region. Some major procurements during 2017-2021 were Boeing's AH-64E combat helicopters by the UAE and the procurement of 48 CH-47F Chinook heavy-lift helicopters by Saudi Arabia.

- During 2017-2021, the active rotorcraft fleet grew by around 4% in the Middle East and 6% in Africa. This growth was driven by the overt intervention of regional powers and ongoing conflicts between Iran, Saudi Arabia, and the UAE. The US, France, and Russia are the major supplier nations of rotorcraft in this region. Apart from the major countries, small countries such as Morocco and Nigeria are also increasing their defense budgets due to the ongoing tensions with Algeria. All such factors are expected to drive the spending on various types of military rotorcraft in the region during the forecast period. During 2023-209, around 514 rotorcraft are expected to be delivered in the region.

Middle East and Africa Military Helicopters Market Trends

Major military powers in the region have surged their defense expenditure

- Defense expenditures in the Middle Eastern region were around USD 184 billion in 2022, a decline of over 3.2% compared to 2021. In contrast, it was around USD 39.4 billion in Africa in 2022, with a decline of over 5% from 2021. Countries such as Saudi Arabia, Egypt, Qatar, United Arab Emirates, and Algeria were the major countries in the region with a high defense expenditure during 2017-22. They have active procurement programs for multi-role and utility aircraft in fixed-wing segments.

- Sub-Saharan Africa's combined military expenditure stood at USD 20.3 billion in 2022, down by 7.3% compared to 2021 and 18% compared to 2013. Nigeria and South Africa, the sub-regions two largest spenders, led the decline in military spending in 2022. In 2022, Israel's military spending fell for the first time since 2009. Its total of USD 23.4 billion was 4.2% lower than in 2021.

- The year-on-year (Y-o-Y) growth in Saudi Arabia's military spending was 16% in 2022 compared to 2021, the first Y-o-Y increase since 2018. Saudi Arabia's military expenditure was estimated at USD 75.0 billion last year. The reduction coincided with accusations that Saudi Arabia had started to remove its military personnel from Yemen. However, the Saudi government denied the allegations and insisted that the personnel were just being redeployed. Since 2015, Saudi Arabia has been leading a coalition in a military campaign against the war-torn nation of Yemen, and the fighting continued into 2022. Saudi Arabia had the second-largest military budget in the world, at 7.4% of GDP, after Ukraine in 2022.

Fleet replacement programs for older aircraft are projected to be the main driver for Middle Eastern military aviation

- As of 2022, the Middle East & Africa had an active fleet of 9,460 aircraft. The total active aircraft fleet increased by 1% in the region compared to 2017. South Africa, Algeria, the United Arab Emirates, Saudi Arabia, Turkey, Egypt, and Qatar accounted for 58% of the total active fleet in the region.

- In the Middle East, defense spending in 2022 totaled USD 157 billion, an increase of 8.6% from 2020 and 5.6% from 2012, respectively. While North Africa accounted for 49%, Sub-Saharan Africa accounted for 51% of the total spending.

- Countries such as Saudi Arabia, Qatar, and the United Arab Emirates are expanding their aircraft fleet size to fulfill the demands of modern warfare. They may continue to produce and acquire next-generation aircraft during the forecast period. The regional armed forces are also enhancing the capabilities of helicopters with cutting-edge technology to obtain military superiority over the external threat.

- Africa's active fleet size decreased by 1% in 2022 compared to 2017. South Africa, Algeria, and Egypt accounted for 45% of the total fleet in Africa. The fleet may increase in the coming years as major countries like Algeria and Egypt plan to procure around 100 aircraft. The Middle East & Africa's active fleet increased by 8% compared to 2017. Saudi Arabia, the United Arab Emirates, Qatar, and Turkey accounted for 59% of the total fleet in the Middle East. During the forecast period, the active aircraft fleet may increase in the region as countries like the United Arab Emirates, Qatar, and Turkey plan to procure around 400 aircraft.

Middle East and Africa Military Helicopters Industry Overview

The Middle East and Africa Military Helicopters Market is fairly consolidated, with the top five companies occupying 100%. The major players in this market are Airbus SE, Leonardo S.p.A, Russian Helicopters, Textron Inc. and The Boeing Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92655

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Gross Domestic Product

- 4.2 Active Fleet Data

- 4.3 Defense Spending

- 4.4 Regulatory Framework

- 4.5 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Multi-Mission Helicopter

- 5.1.2 Transport Helicopter

- 5.1.3 Others

- 5.2 Country

- 5.2.1 Algeria

- 5.2.2 Egypt

- 5.2.3 Qatar

- 5.2.4 Saudi Arabia

- 5.2.5 United Arab Emirates

- 5.2.6 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 Leonardo S.p.A

- 6.4.3 Lockheed Martin Corporation

- 6.4.4 Robinson Helicopter Company Inc.

- 6.4.5 Russian Helicopters

- 6.4.6 Textron Inc.

- 6.4.7 The Boeing Company

- 6.4.8 Turkish Aerospace Industries

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.