Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636566

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636566

Latin America Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 150 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

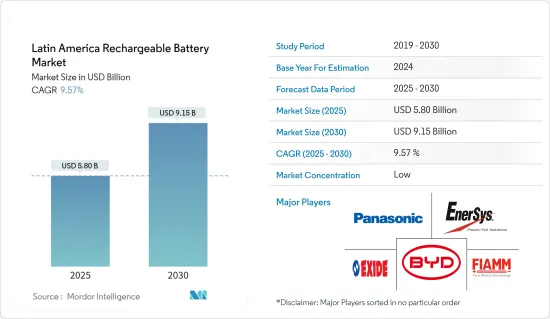

The Latin America Rechargeable Battery Market size is estimated at USD 5.80 billion in 2025, and is expected to reach USD 9.15 billion by 2030, at a CAGR of 9.57% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, declining lithium-ion battery prices, increasing adoption of electric vehicles, and the growing adoption of renewable energy are expected to drive the Latin America rechargeable battery market during the forecast period.

- Conversely, a mismatch in the demand and supply of raw materials is poised to impede the market's growth during the forecast period.

- However, rising demand from commercial infrastructures like data centers, coupled with the growing need for battery recycling and the second-life application of batteries, is set to unlock vast opportunities for the rechargeable battery market in Latin America.

- Brazil stands to see substantial growth in the rechargeable battery market, driven by surging electric vehicle sales and a broader adoption of renewable energy in the region.

Latin America Rechargeable Battery Market Trends

Lithium-ion Batteries to Witness Significant Growth

- During the forecast period, lithium-ion batteries (LIB) are poised to be among the fastest-growing segments in the Latin American rechargeable battery market. Their favorable capacity-to-weight ratio is making lithium-ion batteries increasingly popular compared to other types. Additional factors driving their adoption include superior performance (characterized by longevity and low maintenance), an extended shelf life, and a downward trend in prices.

- Offering distinct technical advantages, lithium-ion (Li-ion) batteries outshine traditional lead-acid batteries. For instance, while lead-acid batteries typically last for about 400-500 cycles, rechargeable Li-ion batteries boast an impressive average of over 5,000 cycles. Furthermore, Li-ion batteries demand less frequent maintenance and replacement. They also maintain consistent voltage throughout their discharge cycle, ensuring prolonged efficiency for connected electrical components.

- In recent years, major industry players have ramped up investments, focusing on economies of scale and R&D to boost battery performance. This surge in competition has led to a notable drop in lithium-ion battery prices. Thanks to technological advancements, manufacturing optimizations, and falling raw material costs, the volume-weighted average price of lithium-ion batteries plummeted from USD 780/kWh in 2013 to USD 139/kWh in 2023. Projections suggest a further decline to approximately USD 113/kWh by 2025 and USD 80/kWh by 2030, making lithium-ion batteries an increasingly attractive option.

- Historically, lithium-ion batteries found their primary application in consumer electronics like mobile phones and laptops. However, their role has expanded, with electric vehicles and battery energy storage systems (BESS) in the renewable energy sector increasingly relying on them.

- While the lithium-ion battery manufacturing industry in Latin America is still in its nascent stages, the region's abundant reserves of essential raw materials and the surging demand from diverse end-users signal a rapid market growth.

- Latin America, often dubbed the Lithium Triangle, boasts vast lithium reserves, a crucial component for lithium-ion batteries. This triangle encompasses Argentina, Bolivia, and Chile, collectively holding over half of the world's known lithium reserves. Chile leads in production, thanks to its extensive lithium-rich brine deposits in the Atacama Desert. Bolivia's Salar de Uyuni stands out as one of the globe's largest lithium reserves, despite extraction challenges. Argentina, with its salt flats in the Puna region, also plays a significant role. Together, these nations are integral to the global lithium-ion battery production supply chain.

- According to the US Geological Survey, lithium production figures for mid-2023 were approximately 44,000 metric tons in Chile, 9,600 metric tons in Argentina, and 4,900 metric tons in Brazil. Such substantial output positions Latin America as a pivotal player in the global lithium-ion battery landscape.

- Latin American countries are intensifying efforts to deepen their involvement in the electric vehicle supply chain. By capitalizing on their mineral wealth, enhancing processing capabilities, and eyeing vehicle manufacturing, nations like Argentina, Chile, Bolivia, and Brazil aim to transform more of their mined lithium into battery chemicals. They're also venturing into battery and electric vehicle manufacturing, as highlighted by Argentina's mining officials.

- In April 2023, BYD Co Ltd, China's leading electric vehicle manufacturer, announced plans for a USD 290 million lithium cathode factory in Chile's Antofagasta region, as reported by Chile's economic development agency, CORFO. Such strategic moves are expected to proliferate in the coming years.

- In mid-2023, the Argentinean government revealed plans for its inaugural lithium-ion battery plant. This facility will utilize lithium carbonate sourced and processed locally by US mining giant Livent Corporation. Constructed by YPF Tecnologia (Y-TEC), a subsidiary of the state-owned YPF, the plant signifies Argentina's commitment to adding value to its rich lithium reserves. With a USD 7 million investment, the facility aims for an annual production capacity of 13MWh, translating to 1,000 stationary energy storage batteries. Moreover, it emphasizes technology transfer opportunities for local firms keen on lithium-ion battery production.

- Given their lightweight nature, rapid charging capabilities, extended charging cycles, and the backdrop of declining costs, lithium-ion batteries are set to dominate the market, especially with the region's significant lithium reserves and industry advancements.

Brazil is Expected to Witness Significant Growth

- Brazil is poised to emerge as a dominant player in the Latin American rechargeable battery market in the near future. This surge is primarily fueled by the escalating demand for batteries across diverse sectors, notably electric mobility, renewable energy, and consumer goods. Furthermore, the industry's expansion is bolstered by supportive government initiatives and technological innovations within the nation.

- Recently, Brazil has seen a swift uptick in electric vehicle (EV) adoption, thanks to government-backed incentives. In 2023, Brazil's EV sales reached approximately 52,000 units (33,000 PHEV and 19,000 BEV), a substantial leap from 2022's 18,500 units (10,000 PHEV and 8,500 BEV). This surge in EV sales is anticipated to bolster the rechargeable battery market in the years ahead.

- Starting January 2024, Brazil imposed a 10% tax on imported 100% electric vehicles (EVs), set to escalate to 18% in July and peak at 35% by July 2026. In response, several Chinese automakers are ramping up local investments. Notably, BYD is establishing a manufacturing complex in Brazil, targeting production by late 2024 or early 2025, while Great Wall Motor's plant is set to commence operations in 2024. These moves are expected to enhance Brazil's domestic EV manufacturing and amplify the demand for rechargeable batteries.

- Echoing global trends, Brazil is actively working to curtail carbon emissions and reduce fossil fuel reliance. To facilitate this transition to electric mobility, the government has rolled out various subsidies and incentives. A prime example is the Green Mobility and Innovation Programme launched at the end of 2023, offering over BRA 19 billion in tax incentives from 2024 to 2028 for companies developing low-emission transport technologies. Such initiatives are poised to bolster the EV sector, subsequently benefiting the rechargeable battery market.

- Beyond the automotive realm, the industrial sector is also driving market growth. Industries are increasingly turning to rechargeable batteries for applications like backup power and renewable energy storage. The burgeoning renewable energy sector, especially solar and wind, is fueling the demand for advanced battery technologies.

- According to the International Renewable Energy Agency (IRENA), Brazil's renewable energy capacity reached about 194 GW in 2023, marking a 28.8% increase from 2020. In 2023, Brazil boasted over 37 GW in solar and 29 GW in wind energy capacities. With government plans to further boost these capacities, the demand for battery energy storage systems (BESS) is set to rise.

- In May 2024, Norwegian energy giant Statkraft AS unveiled a BRL 926 million (USD 180.7 million) investment to install 275 MW of solar capacity at two wind parks in Bahia, Brazil. The solar asset, named Sol de Brotas, will integrate with the 519 MW Ventos de Santa Eugenia complex and the 79.8 MW Morro do Cruzeiro wind power complex.

- Scheduled for construction in 2024, Sol de Brotas will utilize BESS technology, with operations commencing in phases: Morro do Cruzeiro in August 2025 and Ventos de Santa Eugenia in November 2025.

- In early 2023, United States-based Fractal EMS Inc and Brazil's You.On integrated a 30 MW/60 MWh battery energy storage system (BESS) in Brazil. Fractal EMS highlighted that the BESS will optimize power delivery during peak loads, enhancing transmission line resilience and reducing reliance on peaker plants. Such projects, especially with Fractal EMS's equipment-agnostic approach and You.On's choice of Kehua inverters and CATL liquid-cooled batteries, signal a growing trend in Brazil, boosting the demand for industrial rechargeable batteries.

- Given these dynamics, Brazil's rechargeable battery market is set for substantial growth in the foreseeable future.

Latin America Rechargeable Battery Industry Overview

The Latin Americarechargeable battery market is semi-fragmented. Some of the key players in the market (not in any particular order) include Exide Industries Ltd, BYD Company Ltd, FIAMM Energy Technology SpA, Panasonic Holdings Corporation, and EnerSys.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50004072

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Growing Renewable Energy Installation

- 4.5.2 Restraints

- 4.5.2.1 Demand-Supply Mismatch of Raw Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lead-Acid

- 5.1.2 Lithium-Ion

- 5.1.3 Other Technologies (NiMh, Nicd, etc.)

- 5.2 Application

- 5.2.1 Automotive Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Mexico

- 5.3.3 Chile

- 5.3.4 Colombia

- 5.3.5 Argentina

- 5.3.6 Rest of Latin America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Company Ltd

- 6.3.2 EnerSys

- 6.3.3 Panasonic Holdings Corporation

- 6.3.4 Exide Industries Ltd

- 6.3.5 FIAMM Energy Technology SpA

- 6.3.6 C&D Technologies Inc.

- 6.3.7 Duracell Inc.

- 6.3.8 Saft Groupe SA

- 6.3.9 Clarios

- 6.3.10 Acumuladores Moura S.A.

- 6.4 List of Other Prominent Companies (Company Name, Headquarters, Revenue, Relevant Products, Operating Sector, Contact Details, etc.) (In Brief Tabular Format)

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Demand from Commercial Infrastructures Such as Data Centers

- 7.2 Need for a Battery Recycling and Second-life Applications

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.