Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693716

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693716

North America Commercial Aircraft Cabin Seating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 118 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

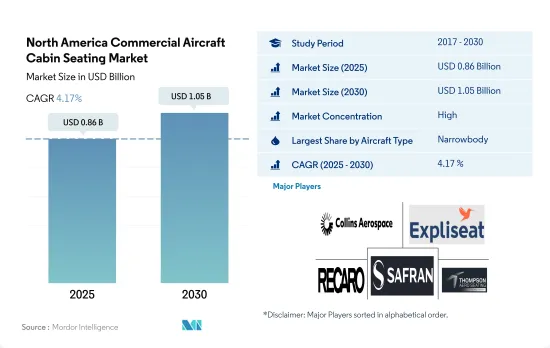

The North America Commercial Aircraft Cabin Seating Market size is estimated at 0.86 billion USD in 2025, and is expected to reach 1.05 billion USD by 2030, growing at a CAGR of 4.17% during the forecast period (2025-2030).

The focus of airlines on passengers' comfort and privacy is expected to drive the demand for narrowbody aircraft in North America

- The latest generation of aircraft seats are made from lightweight, non-metallic materials and designs to reduce fuel expenses and increase the aircraft's sustainability. The demand for seats with enhanced technological features and convenience is increasing, thereby accelerating market growth. Airline operators and OEMs worldwide are increasing their efforts to reduce aircraft weight and develop a sustainable way to manage the airline industry in consideration of the zero-emission 2050 goal.

- As domestic aviation demand has increased, the market for narrowbody aircraft is anticipated to rebound faster than that of widebody aircraft. The 737 MAX's return to service in late 2020 supported the expansion of the narrowbody market. Additionally, an enhanced seating structure with more space than economy-class seats is becoming highly essential due to the rising preferences of business-class travelers.

- In terms of deliveries during 2017-2022, a total of 2,049 aircraft were procured by various airlines in the region. Out of these 2,049 aircraft, narrowbody aircraft accounted for 92%, and widebody aircraft accounted for 8%. The rise in the delivery of new commercial passenger aircraft has positively driven the growth of the cabin seating market. For instance, in July 2021, United Airlines announced that it placed a 270-plane order for Boeing 737 Max and Airbus A320s, and Delta Airlines placed orders for 100 Boeing 737-10 aircraft, with an option for 30 more. Such orders are expected to generate demand for North America's aircraft cabin seating market, and during 2023-2030, a total of 2,885 aircraft are expected to be delivered.

Fleet development by airlines, an increase in demand for fuel-efficient aircraft, and passengers seeking personalized travel experiences are the factors driving the market

- The commercial aircraft segment is expected to experience significant growth during the forecast period, primarily driven by the demand for narrowbody aircraft due to the growing number of domestic passengers in North America. Fleet development of aircraft, an increase in demand for fuel-efficient aircraft, growth in the number of airline passengers, and the consideration of the zero-emission 2050 goal of airlines are factors fueling the demand for commercial aircraft. As of August 2023, the region had a backlog of 1,474 Boeing aircraft and 986 Airbus aircraft. Of these, the US alone had 2,405 aircraft in backlog; hence, the country is expected to witness more significant growth.

- The demand for aircraft seats is driven by passengers as they seek personalized travel experiences. Airlines are responding by investing in customizable seating options that cater to various passenger preferences, such as extra legroom and lie-flat beds. American Airlines had plans to introduce new long-haul routes in 2023; the airline is expected to start accepting deliveries of its next batch of 25 V787-9s and 50 A321XLRs. The new aircraft is expected to feature fully flat business-class seats with direct aisle access, along with proper premium economy seats. In June 2021, American Airlines finished the "Project Oasis" retrofit of its B737-800 fleet. It also completed a similar retrofit of its A321 fleet by the end of 2021. Similarly, Alaska Airlines (Alaska) has placed orders with Recaro Aircraft Seating to equip its new Boeing 737 MAX aircraft with the CL4710 and BL3530 seats. Canada's Nolinor Aviation is equipping its Boeing 737-400 fleet with the TiSeat E2 from Expliseat. With such developments, the market is expected to grow by 1.08% from 2023 to 2030.

North America Commercial Aircraft Cabin Seating Market Trends

Airlines are placing huge orders for new fuel-efficient aircraft, and the expansion of LCCs is contributing to the growth of the market

- The United States accounted for 80% of the total air passenger traffic in North America in 2022. Therefore, the United States is expected to generate the highest demand for new aircraft deliveries compared to other North American countries over the forecast period. Airlines are looking to expand their fleet size to cater to the growing demand for air travel, which may generate significant demand for new aircraft in North America.

- A total of 1,903 new passenger aircraft were delivered in North America between 2017 and 2022, and a further 2,885 new jets are expected to be delivered to the region during 2023-2030. Of the 1,903 jets delivered, 1,748 were narrowbody aircraft, and 155 were widebody aircraft. The expansion of low-cost carriers has resulted in huge demand for newer generation narrowbody aircraft, which offer advantages such as low operation costs and fuel efficiency in short-haul routes. It is expected that out of all the jets that will be delivered during the forecast period, around 2,678 of them will be narrowbody aircraft. This is due to several factors, including the preference for economical and smaller aircraft, the success of low-cost carriers, and the introduction of long-range narrowbody aircraft. Some of the major airlines in North America are American Airlines, Delta Air Lines, United Airlines, Southwest Airlines, Air Canada, and Alaska Airlines. These airlines together have a backlog of over 2,460 aircraft, including a mix of both narrowbody and widebody aircraft. During the COVID-19 pandemic, most major airlines retired some of their old aircraft models and procured new fuel-efficient aircraft to remain profitable. As the airlines try to maintain a younger fleet, large orders for new aircraft are expected during the forecast period.

Rising economy, increase in tourism industry and ease of restrictions are the driving factors for a consistent air passenger traffic growth in North America

- North America's vast landmass and diverse destinations make it a popular choice for millions of passengers who choose to fly both domestically and internationally. Factors such as a growing economy, increased affordability of air travel, and a rising middle class have contributed to a significant uptick in air passenger traffic. Air passenger traffic in the United States reached 1.04 billion in 2022, up by 7% compared to 2021 and 12% compared to 2019. In 2022, from January through December, US airlines carried 853 million passengers, up from 658 million in 2021 and 388 million in 2020. The total number of passengers carried by airlines in Canada reached 107 million in 2022, surpassing the levels in 2021 by 6%. In 2022, Mexico had 100 million air passenger traffic, representing a 7% growth compared to its 2021 traffic levels. North America has benefitted from fewer and shorter-lasting travel restrictions than many other countries and regions. This has boosted domestic travel in the large home market, as well as international travel. Net profits in the region are expected to rise from USD 9.9 billion in 2022 to USD 11.4 billion in 2023.

- To cater to the demand driven by air passenger traffic, various airlines in the region are planning to procure new aircraft. For instance, around one-third of global aircraft deliveries in 2023 were anticipated to be received by various carriers in North America. Although the region's aircraft deliveries were already above 2019 levels in 2022, they were expected to grow by an additional 72 units in 2023. Overall, with consistent air travel, the region's air passenger traffic is expected to increase by 1.7 billion in 2030 compared to 1.2 billion recorded in 2022.

North America Commercial Aircraft Cabin Seating Industry Overview

The North America Commercial Aircraft Cabin Seating Market is fairly consolidated, with the top five companies occupying 68.43%. The major players in this market are Collins Aerospace, Expliseat, Recaro Group, Safran and Thompson Aero Seating (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 93612

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 New Aircraft Deliveries

- 4.3 GDP Per Capita (current Price)

- 4.4 Revenue Of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure On Airport Construction Projects (ongoing)

- 4.8 Expenditure Of Airlines On Fuel

- 4.9 Regulatory Framework

- 4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Narrowbody

- 5.1.2 Widebody

- 5.2 Country

- 5.2.1 Canada

- 5.2.2 United States

- 5.2.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Adient Aerospace

- 6.4.2 Collins Aerospace

- 6.4.3 Expliseat

- 6.4.4 Jamco Corporation

- 6.4.5 Recaro Group

- 6.4.6 Safran

- 6.4.7 STELIA Aerospace (Airbus Atlantic Merginac)

- 6.4.8 Thompson Aero Seating

- 6.4.9 ZIM Aircraft Seating GmbH

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.