PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683483

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683483

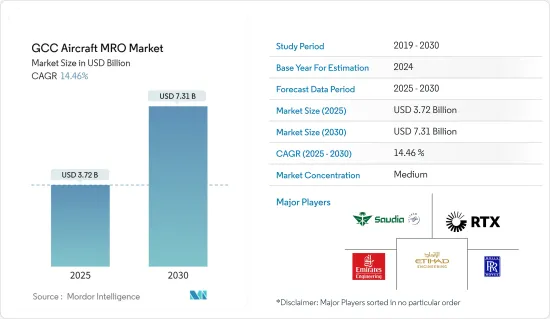

GCC Aircraft MRO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The GCC Aircraft MRO Market size is estimated at USD 3.72 billion in 2025, and is expected to reach USD 7.31 billion by 2030, at a CAGR of 14.46% during the forecast period (2025-2030).

Key regional economic powerhouses, including the United Arab Emirates, Saudi Arabia, and Qatar, are investing substantially in acquiring new aircraft. Meanwhile, several other GCC nations focus on procuring refurbished aircraft and enhancing their existing military fleet. This collective push is a primary driver for the growth of the aircraft MRO market.

While the GCC region has witnessed a surge in aircraft fleets and MRO entities over the past two decades, attracting and retaining skilled labor is a notable challenge. While this challenge is prevalent globally, it has become increasingly pronounced in the region. The demand for maintenance technicians is projected to outstrip supply shortly, so the situation calls for strategic solutions.

The United Arab Emirates and Saudi Arabia stand out as pivotal aviation hubs in the GCC. Recognizing this, their governments are actively fostering partnerships and joint ventures between local and foreign MRO providers, aiming to bolster the region's aircraft MRO market in the coming years.

GCC Aircraft MRO Market Trends

Engine Segment Anticipated to Generate Highest Growth

- The Middle East and Africa's aircraft engine MRO market is poised for robust growth, buoyed by a surging commercial aviation sector. This growth is underpinned by escalating air passenger traffic, airlines' heightened procurement of new aircraft, and improving economic landscapes in several regional countries.

- In response to the escalating air traffic, several GCC nations have granted substantial aircraft contracts to industry giants like Airbus and Boeing. Notably, Qatar Airways, as of March 2023, had a staggering USD 72 billion worth of orders for around 250 Airbus and Boeing aircraft, with most slated for delivery within the forecast period. Capitalizing on their strategic location, Gulf governments are funneling significant investments into bolstering and expanding their airport infrastructure.

- Moreover, the Middle East's landscape, with its limited domestic travel and the presence of global aviation hubs like Dubai, has seen a surge in the utilization of widebody aircraft. Consequently, the demand for widebody aircraft engine MRO services is rising. For instance, in December 2023, FlyDubai sealed a deal with Boeing for 30 B787-9 aircraft, intending to deploy them on new, high-demand routes. Notably, a significant portion of the region's engine MRO is managed by industry stalwarts like Rolls Royce PLC, General Electric Company, and Pratt & Whitney, further fueling the demand for commercial aircraft engine MRO services in the region.

United Arab Emirates to Hold the Largest Market Share

- The United Arab Emirates boasts major airlines like Etihad Airways and Emirates, which are actively modernizing passenger and cargo aircraft fleets. This, in turn, fuels the demand for aircraft MRO services, driven by the influx of new aircraft into the region's airlines.

- Moreover, these carriers are bolstering their presence in the LCC (low-cost carrier) sector through strategic partnerships. As a result, there is a rising demand for narrowbody aircraft and their MRO services. For example, Air Arabia Abu Dhabi, a collaboration between Etihad Aviation Group and Air Arabia, commenced operations in July 2020, marking the UAE capital's first low-cost carrier. In a significant move, the airline inked a deal with Airbus in November 2019 for 120 A320neo aircraft, with deliveries set to begin in 2025. Subsequently, in November 2023, Air Arabia Abu Dhabi secured a contract with CFM International for 240 CFM Leap-1A engines to power its fleet, including the A321XLR. Such substantial aircraft and engine orders are poised to propel the MRO market's growth in the GCC region.

- While many UAE airlines boast robust MRO capabilities, they still rely on engine OEMs and third-party providers for maintenance. This reliance has notably bolstered the market for engine MRO services in recent years. For instance, in November 2023, Sanad unveiled its LEAP Engine MRO Center in Abu Dhabi. This new facility, dedicated to LEAP-1A and 1B engines, has an impressive capacity to service up to 200 engines annually. These advancements are set to further fuel the country's aircraft MRO market during the forecast period.

GCC Aircraft MRO Industry Overview

The GCC aircraft MRO market is semi-consolidated and dominated by local players who perform base and line maintenance, ranging from simple A to complex D checks. Some major players in the market are Saudia Aerospace Engineering Industries, Emirates Engineering (Emirates Group), Rolls Royce PLC, RTX Corporation, and Etihad Airways Engineering LLC.

As governments increasingly support the establishment of maintenance hubs, local players in the GCC region are forming domestic and international partnerships. Entities like Lufthansa Technik AG (a part of the Lufthansa Group), AMAC Aerospace, and Joramco have significantly expanded their MRO service networks through strategic collaborations. This surge in partnerships stands out as a primary catalyst for the growth of the aircraft MRO market in the GCC. Consequently, the region's expansion initiatives are predominantly centered around partnerships involving airlines, third-party providers, and engine OEMs. These collaborative strategies are expected to enhance the market shares of companies in the years ahead.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By MRO Type

- 5.1.1 Airframe

- 5.1.2 Engine

- 5.1.3 Component and Interior

- 5.1.4 Line

- 5.2 By Geography

- 5.2.1 United Arab Emirates

- 5.2.2 Saudi Arabia

- 5.2.3 Qatar

- 5.2.4 Oman

- 5.2.5 Kuwait

- 5.2.6 Bahrain

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Safran SA

- 6.2.2 General Electric Company

- 6.2.3 Rolls-Royce PLC

- 6.2.4 RTX Corporation

- 6.2.5 Lufthansa Technik AG

- 6.2.6 Jordan Aircraft Maintenance Limited (Dubai Aerospace Enterprise (DAE))

- 6.2.7 Etihad Airways Engineering LLC

- 6.2.8 Saudia Aerospace Engineering Industries

- 6.2.9 Qatar Airways Group

- 6.2.10 ExecuJet MRO Services (Pty) Ltd (Dassault Aviation)

- 6.2.11 Emirates Engineering (Emirates Group)

- 6.2.12 Oman Air

7 MARKET OPPORTUNITIES AND FUTURE TRENDS