Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636569

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636569

Middle-East And North Africa Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 150 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

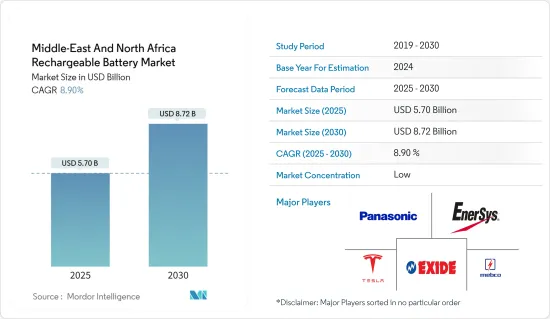

The Middle-East And North Africa Rechargeable Battery Market size is estimated at USD 5.70 billion in 2025, and is expected to reach USD 8.72 billion by 2030, at a CAGR of 8.9% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing adoption of electric vehicles, rising adoption of renewable energy, and declining lithium-ion battery prices are expected to drive the Middle East and North Africa rechargeable battery market during the forecast period.

- Conversely, a mismatch between the demand and supply of raw materials is anticipated to impede the market's growth during the forecast period.

- However, advancements in new battery technologies, innovative battery chemistries, and an increasing emphasis on battery recycling are poised to offer substantial opportunities for the rechargeable battery market in the Middle East and North Africa.

- The United Arab Emirates is set to experience notable growth in the rechargeable battery market, driven by surging electric vehicle sales and a growing adoption of renewable energy in the region.

Middle-East And North Africa Rechargeable Battery Market Trends

Lithium-ion Battery to be the Fastest Growing

- Among various battery technologies, lithium-ion batteries (LIBs) are poised to emerge as the fastest-growing segment in the rechargeable battery market of the Middle East and North Africa during the forecast period. LIBs are outpacing other battery types in popularity due to their favorable capacity-to-weight ratio. Their adoption is further fueled by advantages like superior performance (including extended life and low maintenance), an impressive shelf life, and a notable decrease in prices.

- Li-ion batteries boast several technical advantages over alternatives like lead-acid batteries. On average, rechargeable Li-ion batteries offer over 5,000 cycles, a stark contrast to the 400-500 cycles typical of lead-acid batteries. Moreover, Li-ion batteries demand less frequent maintenance and replacement. They also maintain consistent voltage throughout their discharge cycle, ensuring prolonged efficiency for electrical components.

- In recent years, major industry players have ramped up investments in R&D and economies of scale, intensifying competition and driving down lithium-ion battery prices. Thanks to technological innovations, manufacturing enhancements, and falling raw material costs, the volume-weighted average price of lithium-ion batteries plummeted from USD 780/kWh in 2013 to USD 139/kWh in 2023. Projections suggest a further dip to around USD 113/kWh by 2025 and an ambitious USD 80/kWh by 2030. Such trends in declining battery costs position lithium-ion batteries as an increasingly attractive option.

- Historically, lithium-ion batteries found their primary application in consumer electronics like mobile phones and laptops. Yet, their role has expanded significantly. Today, they're the preferred power source for hybrids, the entire range of battery electric vehicles (BEVs), and battery energy storage systems (BESS) in the renewable energy sector.

- While the Middle East and North Africa's lithium-ion battery manufacturing industry is still in its nascent stages, trailing behind global frontrunners like China, the United States, and Europe, there's a concerted effort to bolster this sector. Countries, especially the UAE and Saudi Arabia, are channeling investments into battery manufacturing and related technologies. This move aims to diversify their economies, support renewable energy goals, and cater to the surging demand for electric vehicles.

- For instance, in February 2024, Titan Lithium, in partnership with Khalifa Economic Zones Abu Dhabi (KEZAD) Group, unveiled plans for a state-of-the-art lithium processing facility. This AED 5 billion venture, sprawling over 290,000 square meters in KEZAD Al Mamourah, aims to produce battery-grade lithium carbonate and hydroxide, essential for the lithium-ion battery and EV sectors.

- Similarly, Saudi Arabia is making strides in the global rechargeable battery arena. In June 2023, Obeikan Investment Group teamed up with Australian startup European Lithium to establish a lithium hydroxide refinery. The following month, Saudi state mining giant Ma'aden and US-based Ivanhoe Electric struck a deal to explore 48,500 sq km of the Arabian Shield for lithium and other rare metals.

- In September 2023, Energy Capital Group, a Saudi investment firm, collaborated with US tech startup Pure Lithium to pioneer batteries using lithium sourced from oilfield brines. With an initial investment of USD 50 million, this venture aims to address the burgeoning demand for lithium-ion battery metals. Additionally, ERG's membership in the Global Battery Alliance underscores its commitment to a sustainable global supply chain for lithium-ion batteries. Such initiatives signal a promising trajectory for the region's lithium-ion battery industry.

- In summary, attributes like lightweight design, rapid charging, extended charging cycles, decreasing costs, and advancements in the lithium-ion battery sector position it as the fastest-growing battery technology in the Middle East and North Africa's rechargeable battery market during the forecast period.

United Arab Emirates to Witness Significant Growth

- During the forecast period, the rechargeable battery market in the United Arab Emirates (UAE) is poised for substantial growth, positioning it as a regional leader. This momentum is fueled by rapid industrialization, government backing for renewable energy, a burgeoning electric vehicle (EV) sector, technological strides, and the UAE's strategic economic stature in the region. Collectively, these elements foster a fertile ground for the adoption and innovation of rechargeable batteries in the UAE.

- As the UAE industrializes swiftly, the demand for dependable energy storage solutions surges, driving the uptake of rechargeable batteries across diverse sectors. Moreover, the UAE's dedication to sustainability and renewable energy is set to play a pivotal role, especially as the nation seeks to curtail its carbon emissions and amplify the proportion of renewables in its energy portfolio. This shift is bolstered by governmental initiatives championing clean energy technologies, notably solar power. Such efforts amplify the demand for efficient battery energy storage systems (BESS), thereby propelling the rechargeable battery market. Illustratively, the UAE has set ambitious energy targets, aiming to elevate its renewable energy capacity from approximately 6.05 GW in 2023 to a robust 14.2 GW by 2030, more than tripling its current capacity. This ambitious goal is poised to generate a substantial demand for BESS.

- In recent years, the UAE has witnessed a swift embrace of electric vehicles (EVs). Data from the International Energy Agency (IEA) highlights this trend: EV sales in the UAE, encompassing both Battery Electric Vehicles (BEV) and Plug-in Hybrid Electric Vehicles (PHEV), surged to roughly 28,900 units in 2023, marking a 50% increase from 2022's tally of about 18,900 units. Such a rising tide in EV adoption is anticipated to bolster the rechargeable battery market.

- Moreover, the UAE envisions electric and hybrid vehicles constituting 50% of all vehicles on its roads by 2050. With substantial investments in EV infrastructure and a push for EV adoption-aimed at mitigating climate change and reducing fossil fuel dependence-the demand for high-capacity, durable rechargeable batteries is escalating.

- In tandem with the surging battery demand, the UAE is making strides in battery recycling. A notable development occurred in December 2023, when LOHUM Cleantech, an Indian firm, unveiled plans to establish the UAE's inaugural EV Battery Recycling plant. This venture, in collaboration with the UAE's Ministry of Energy & Infrastructure and BEEAH-a leader in sustainability and digitalization in the Middle East-aligns with the UAE's COP28 agenda, its Net Zero by 2050 Strategic Initiative, and its Circular Economy Policy. The initiative also champions emissions-free mobility with forward-thinking solutions.

- The ambitious project will feature an expansive 80,000 sq ft facility dedicated to refurbishing and recycling lithium batteries. Annually, this facility is set to recycle 3,000 tons of lithium-ion batteries and convert 15MWh of battery capacity into Energy Storage Systems (ESS). Such output is projected to satisfy over 80% of the anticipated EV battery management needs.

- Advancements in battery technology, particularly the emergence of solid-state batteries, are boosting the efficiency, safety, and overall appeal of rechargeable batteries for both consumers and businesses. A testament to this trend, in April 2024, US-based Statevolt announced its intent to produce solid-state battery cells in the UAE by 2026. The company is laying the groundwork for a USD 3.2 billion gigafactory in Ras Al Khaimah, targeting an annual output of 40 gigawatt-hours (GWh). This initiative eyes the burgeoning export markets for battery storage and electric mobility across the Middle East, extending to Africa and India.

- Given these dynamics, the United Arab Emirates (UAE) is set to emerge as a dominant player in the rechargeable battery landscape of the Middle-East and North Africa during the forecast period.

Middle-East And North Africa Rechargeable Battery Industry Overview

The Middle-East and North Africa rechargeable battery market is semi-fragmented. Some of the key players in the market (not in any particular order) include Tesla Inc., Exide Industries Ltd., Middle East Battery Company (MEBCO), EnerSys and Panasonic Holdings Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50004075

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Growing Renewable Energy Installation

- 4.5.2 Restraints

- 4.5.2.1 Demand-Supply Mismatch of Raw Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lead-Acid

- 5.1.2 Lithium-Ion

- 5.1.3 Other Technologies (NiMh, Nicd, etc.)

- 5.2 Application

- 5.2.1 Automotive Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 United Arab Emirates

- 5.3.2 Saudi Arabia

- 5.3.3 Egypt

- 5.3.4 Algeria

- 5.3.5 Rest of Middle-East and North Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Panasonic Holdings Corporation

- 6.3.2 Tesla Inc.

- 6.3.3 Saft Groupe SA

- 6.3.4 Middle East Battery Company (MEBCO)

- 6.3.5 EnerSys

- 6.3.6 Exide Industries Ltd

- 6.3.7 FIAMM Energy Technology SpA

- 6.3.8 Statevolt

- 6.3.9 Statron Ltd

- 6.3.10 Amara Raja Energy & Mobility Limited.

- 6.3.11 C&D Technologies Inc.

- 6.3.12 United Batteries Co.

- 6.3.13 Chloride Egypt S.A.E.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Progress in Developing New Battery Technologies and Advanced Battery Chemistries

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.