Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636449

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636449

South America Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 110 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

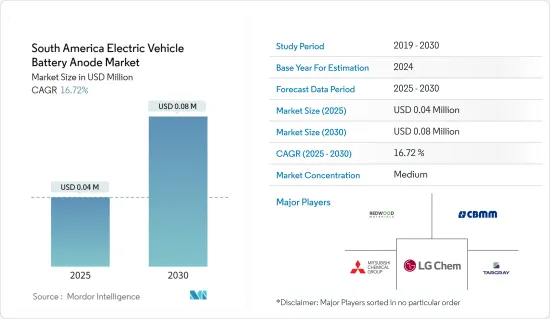

The South America Electric Vehicle Battery Anode Market size is estimated at USD 0.04 million in 2025, and is expected to reach USD 0.08 million by 2030, at a CAGR of 16.72% during the forecast period (2025-2030).

Key Highlights

- In the forecast period, the market is poised for growth, driven by the rising adoption of electric vehicles, supportive government initiatives, and declining prices of lithium-ion batteries.

- However, the region's heavy reliance on importing battery components poses a challenge to future market expansion.

- Yet, ongoing research and advancements in anode materials and efficient electrolytes present promising opportunities for market growth.

- Brazil is set to lead the market, fueled by the increasing demand for anode materials in the automotive sector.

South America Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery is Expected to Have a Major Share

- South America's lithium-ion EV battery market is poised for growth, thanks to the region's abundant lithium resources. The Lithium Triangle, spanning parts of Argentina, Bolivia, and Chile, harbors over half of the world's lithium reserves, cementing South America's pivotal role in the global EV supply chain.

- With these vast reserves and a 14% drop in lithium-ion battery pack prices in 2023 (down to USD139/kWh), there's a burgeoning opportunity for domestic manufacturing of electric vehicle batteries and their components, such as anodes.

- In light of these developments, many battery companies are channeling investments into exploring the region's lithium reserves. This surge in exploration and production is set to amplify the demand for lithium-ion batteries in electric vehicles, subsequently heightening the need for battery anodes in their production.

- For example, in July 2024, French mining group Eramet and China's Tsingshan launched a lithium production plant in Salta, Argentina, addressing the electric car industry's rising demands. This strategic investment, amounting to USD 870 million, underscores the site's significance.

- Looking ahead, as the region ramps up investments in lithium-ion battery manufacturing, buoyed by its rich reserves, the market for lithium-ion anodes in EVs is on an upward trajectory. Bolstering this outlook, Bolivia's President, in March 2024, unveiled ambitions to commence battery exports, including EV batteries, by 2026.

- Given the rising adoption of lithium-ion batteries in electric vehicles and their plummeting prices, the lithium-ion battery anode segment is set for substantial growth in the coming years.

Brazil is Expected to have a Significant Share

- Brazil stands as South America's largest automotive market, boasting a robust manufacturing base that hosts numerous global automakers. As the industry pivots towards electrification, this trend has seamlessly transitioned to the production of essential components, notably batteries and battery anodes.

- Moreover, Brazil's rising stature in the EV battery manufacturing arena is shaping the trajectory of its EV battery anode market. With Brazil drawing substantial foreign investments and forging global partnerships to set up battery production facilities, there's a heightened demand for premium anode materials, vital for lithium-ion batteries.

- For example, in September 2023, BYD, a Chinese firm, launched its first battery factory in Brazil. Beyond electric vehicles (EVs), BYD is set to produce electric buses in Brazil, leveraging batteries manufactured on-site. Such strategic moves are poised to amplify the demand for the country's EV battery anode market.

- Furthermore, as electric vehicle sales surge in Brazil, battery manufacturers are increasingly investing in local production, further fueling the demand for EV battery anodes. The International Energy Agency reported that in 2023, Brazil's EV car sales reached 52,000 units, a significant jump from 18,500 units in 2022.

- Looking ahead, bolstered by government backing in the EV battery sector, the battery anode market is poised for growth. Recent policy shifts by Brazil's government have ignited a wave of new investments from vehicle manufacturers. These investments, targeting facility modernization and enhanced R&D, emphasize sustainability and the production of electric and hybrid vehicles. The Brazilian Association of Vehicle Manufacturers highlighted a landmark commitment of USD 22 billion in 2024 investments, extending through 2032.

- Given the surging adoption of EVs and the burgeoning battery manufacturing landscape, Brazil is set to lead the market in the coming years.

South America Electric Vehicle Battery Anode Industry Overview

The South America electric vehicle battery anode market is semi-concentrated. Some of the major players in the market (in no particular order) include Redwood Materials Inc., Mitsubishi Chemical Group Corporation, CBMM, LG Chem Ltd, and Targray Industries Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50003716

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Policies and Investments towards battery manufacturing

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 Dependence on Battery Imported Components

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Other Battery Types

- 5.2 Material

- 5.2.1 Lithium

- 5.2.2 Graphite

- 5.2.3 Silicon

- 5.2.4 Others

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Colombia

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Redwood Materials Inc.

- 6.3.2 Anovion LLC

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 CBMM

- 6.3.5 NEI Corporation

- 6.3.6 Targray Industries Inc.

- 6.3.7 Nexeon Lid.

- 6.3.8 LG Chem Ltd

- 6.3.9 Tokai Carbon Co., Ltd.

- 6.3.10 Resonac Holdings Corporation.

- 6.4 Market Ranking Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Increasing Research and Development of Other Anode Materials

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.