Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693782

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693782

Africa Biopesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 149 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

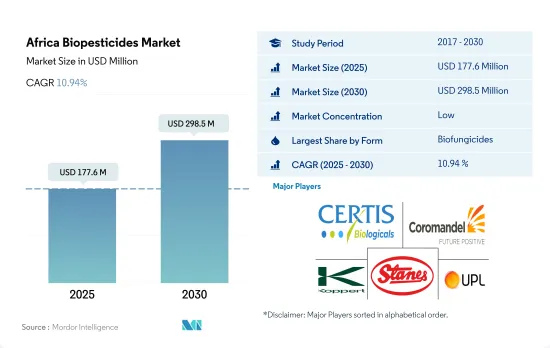

The Africa Biopesticides Market size is estimated at 177.6 million USD in 2025, and is expected to reach 298.5 million USD by 2030, growing at a CAGR of 10.94% during the forecast period (2025-2030).

- Biopesticides are naturally occurring substances or agents derived from animals, plants, insects, and microorganisms, including bacteria and fungi, used to manage agricultural pests and infections. The African biopesticides market grew by 23.4% from 2017 to 2022.

- Biopesticide consumption in row crops is higher than other crops in the region, accounting for 73.8% in 2022. Horticultural crops accounted for 19.7%, while cash crops accounted for 6.5% of the overall consumption in the same year.

- The Integrated Pest Management (IPM) concept is important in the African biopesticides market. IPM 1.0 was established decades ago to reduce the overuse of agricultural pesticides. IPM 2.0 gradually incorporated agroecological principles such as biological control and habitat management. However, throughout this period, smallholder farmers did not improve their decision-making skills and continued to rely on hazardous pesticides as their first line of defense. The African region also implemented Integrated Pest Management 3.0 (IPM 3.0), which includes three new features, i.e., real-time farmer decision-making access, pest-management options based on science and nature, and the integration of genomic approaches, biopesticides, and habitat-management practices. These IPM practices may drive the biopesticides market in Africa.

- In collaboration with Real IPM Ltd, the International Centre of Insect Physiology and Ecology commercialized two biopesticides, Campaign (icipe69) and Achieve (icipe78). Campaign (icipe69) is being used against mealybugs, thrips, and fruit flies, in crops such as cucumber, mango, papaya, rose, and tomato. Adoption of IPM practices and increased R&D activities of biopesticides may boost the market value by 84.7% between 2023 and 2029.

- The African biopesticides market has exhibited a growth rate of 15.8% between 2017 and 2021, and this growth is expected to continue with a projected expansion of about 84.7% by 2029.

- This growth is primarily attributed to the launch of Integrated Pest Management 3.0 (IPM 3.0) in Africa. This pest management strategy is based on three pillars: real-time farmer decision-making access, science-based pest-management alternatives, and the combination of genetic methods, biopesticides, and habitat-management strategies. These IPM methods are expected to play a critical role in driving the growth of the African biopesticides market.

- Biofungicides are the dominant segment of the biopesticides market in the Rest of Africa segment, and it was valued at USD 45.6 million in 2022. Trichoderma is widely used as a biofungicide as it destroys other fungi enzymatically and produces anti-microbial substances that kill pathogenic fungi.

- Egypt, South Africa, and the Rest of Africa are the primary segments in the African region regarding organic agriculture acreage. In 2022, the Rest of Africa accounted for 95.0% of total organic agricultural land in Africa, with 1.2 million hectares. Egypt contributed 3.5% with 45.1 thousand hectares, while South Africa accounted for 1.0% with 12.6 thousand hectares. The high organic agricultural acreage in these countries provides significant market opportunities.

- The increasing consumer interest in organic products, growing awareness among farmers, and the economic advantages of using biopesticides are anticipated to drive the demand for biopesticides in Africa, and the market is expected to record a CAGR of 9.2% between 2023 and 2029.

Africa Biopesticides Market Trends

8,34,000 organic producers are in the region's organic sector with Tunisia is having more organic land

- In 2022, the area of organic agricultural land in the African region amounted to over 1.2 million hectares, representing 9.0% of the global organic agricultural area.

- In 2020, Africa reported 149,000 hectares more in organic cultivation land than in 2019, recording a 7.7% increase Y-o-Y in line with the presence of nearly 834,000 producers. Tunisia had the largest amount of organic land (more than 290,000 hectares in 2020), whereas Ethiopia had the highest number of organic producers (almost 220,000). The island states of Sao Tome and Principe have the most significant amount of land committed to organic farming in the region, with 20.7% of their agricultural area dedicated to organic crops.

- In the African region, cash crops account for a significant share of organic agricultural land, amounting to 63.2% of the total organic acreage with 817.4 thousand hectares. Row crops hold the second-largest share of organic acreage in Africa, which amounts to about 25.6% of the total organic acreage, totaling 331.2 thousand hectares. Horticultural crops account for 11.2% of the total organic acreage in Africa, with 144.9 thousand hectares in 2022.

- The African countries with significant organic agricultural acreage include the Rest of Africa regional segment, Egypt, and South Africa. In 2022, the Rest of Africa accounted for 95.0% of the total organic agricultural acreage in Africa, with 1.2 million hectares, Egypt accounted for a 3.5% share with 45.1 thousand hectares, and South Africa accounted for a 1.0% share with 12.6 thousand hectares.

- Organic agricultural acreage rose by 6.9% between 2017 and 2022 in Africa. It is anticipated to increase by about 52.2% and reach USD 2.0 million by 2029.

Per capita spending on organic product predominant in Egypt, South Africa, and Nigeria countries

- Africa's per capita income has consistently increased throughout the years, encouraging people to spend more money on nutritious food. Organic foods and beverages are gaining more shelf space in the African region. Since the domestic consumption of certified organic produce is relatively small, most organic goods are produced for export.

- In Africa, consumption of organic products has increased significantly, especially in Egypt, South Africa, and Nigeria. In 2021, the per capita consumption of organic products was USD 55.5 in Egypt, followed by South Africa with USD 7.1. The countries with the highest number of organic producers were Ethiopia (almost 222,000), Tanzania (nearly 149,000), and Uganda (over 139,000).

- In the African region, commonly consumed organic products include fresh vegetables and fruits. In Africa, significant efforts have been made to mainstream organic agriculture into policy, national extension systems, marketing, and value chain development. All these factors have gained the attention of consumers.

- With the increasing per capita consumption of beverages, primarily fruit juices, growing health awareness, and consumers shifting toward organic drinks and food that do not contain chemical ingredients, the demand for the African organic food market is expected to grow between 2023 and 2029.

- However, low-income levels and a lack of organic standards and other infrastructure for local market certification are the major restraining factors for the growth of the organic market in the region.

Africa Biopesticides Industry Overview

The Africa Biopesticides Market is fragmented, with the top five companies occupying 14.93%. The major players in this market are Certis USA LLC, Coromandel International Ltd, Koppert Biological Systems Inc., T. Stanes and Company Limited and UPL (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 500042

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Egypt

- 4.3.2 Iran

- 4.3.3 Nigeria

- 4.3.4 South Africa

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Biofungicides

- 5.1.2 Bioherbicides

- 5.1.3 Bioinsecticides

- 5.1.4 Other Biopesticides

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 Egypt

- 5.3.2 Nigeria

- 5.3.3 South Africa

- 5.3.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Andermatt Group AG

- 6.4.2 Atlantica Agricola

- 6.4.3 Biolchim SPA

- 6.4.4 Certis USA LLC

- 6.4.5 Coromandel International Ltd

- 6.4.6 IPL Biologicals Limited

- 6.4.7 Koppert Biological Systems Inc.

- 6.4.8 T. Stanes and Company Limited

- 6.4.9 UPL

- 6.4.10 Valent Biosciences LLC

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.