Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693455

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693455

North America Oilseed (seed For Sowing) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 202 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

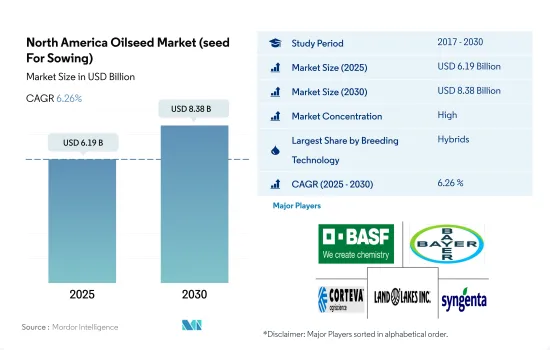

The North America Oilseed Market (seed For Sowing) size is estimated at 6.19 billion USD in 2025, and is expected to reach 8.38 billion USD by 2030, growing at a CAGR of 6.26% during the forecast period (2025-2030).

Increased innovation of seeds and increased area under cultivation are driving the market growth

- Oilseeds accounted for 22.9% of the North American seed market in 2022, which is projected to grow during the forecast period. The acreage under cultivation of oilseeds was 49.8 million ha in 2022, which increased by 5.6% from 2020 due to the increased availability of high-yielding hybrids and the adoption of GM hybrids.

- In 2022, hybrids dominated the oilseeds market with a market value of USD 4.84 billion in the region. Major companies in the market are introducing hybrid varieties. For instance, in 2022, Syngenta Seeds launched a new conventional soybean brand, "Silverline," in the Canadian market. This brand offers high-protein soybeans and NK-treated soybean varieties.

- The United States and Canada are the major countries in the world that have approved and commercialized genetically modified oilseeds such as canola and soybean. The major traits are herbicide tolerance and insect resistance, and other traits, such as high oil content, high oleic acid, and lauric acid content, fetch high prices in the processing industry. The total acreage under hybrid oilseed cultivation in 2022 was 29.7 million hectares, which increased by 20.3% compared to 2017.

- The United States is the largest country in terms of area under open-pollinated varieties and hybrid derivatives in North America. This is because the total acreage of oilseeds is higher in the United States.

- OPVs are expected to increase in the United States and Mexico due to organic farming and the prohibition of GMOs during the forecast period. In Canada, transgenic hybrids are most adopted by growers due to their high oil content and market prices. Therefore, the oilseed market is estimated to grow in the region in both hybrids and OPVs during the forecast period.

The United States is the largest oilseed market in North America

- In 2022, North America accounted for 40.3% of the global oilseeds market. The market grew by 65% in 2022, compared to 2017, mainly due to the increased cultivation area of oilseed crops. North America is the major exporter of oilseeds, and there is a high demand for consumption in different forms. Moreover, the area under oilseeds accounted for 49.8 million hectares, which has increased by 12.8% compared to 2019.

- In 2022, the United States accounted for 74.4% of the North American oilseed seed demand due to the high demand for consumption, being a leading exporter, and high-profit margins. Soybean and canola are the major oilseeds grown in the country, together contributing 95.3% of the country's oilseed market.

- Canada accounted for 24.7% of the North American oilseed market in 2022, with canola being a major oilseed market, accounting for USD 784.2 million. Canada is the world's largest producer of canola oilseeds, as it has high demand from the biofuel industry. In addition, the country has adopted transgenic canola seeds, which has contributed to major growth in the country's oilseed market.

- Mexico and other major North American countries, such as Cuba, Dominican Republic, Costa Rica, Jamaica, Panama, and Haiti, held a 0.8% market share of the region's oilseed market. Oilseeds are mainly used for domestic consumption in these countries.

- The trade agreement between the United States, Canada, and Mexico is helping these countries have free trade and limited approvals required for exporting seeds from one to another between the three countries.

- Therefore, the high demand for oil crops, trade agreements, and adoption of transgenic oilseed cultivars are the major factors anticipated to drive the growth of the market during the forecast period with a CAGR of 6.1%.

North America Oilseed Market (seed For Sowing) Trends

Soybean occupied the major share of oilseed acreage, with growth potential toward canola and sunflower in Canada and Mexico, respectively

- North America is a significant global producer of oilseeds, primarily due to its favorable climate conditions. In 2022, oilseed crops covered 28.8% of the total cultivated area, spanning 49.8 million hectares. However, compared to 2017, there was a decrease in oilseed cultivation in 2018 and 2019 by 3.3% and 15%, respectively, due to the decline in soybean cultivation. This reduction was driven by China's trade restrictions, which reduced global demand for US varieties of soybeans, leading to lower soybean prices. Additionally, heavy spring rains in 2019 further contributed to the decline in soybean cultivation.

- The United States was the largest country in the region, which accounted for 75.3% in 2022, with 37.5 million hectares. Soybean was the major crop in the region, with 94.1% of the oilseed acreage in 2022. The higher share of soybeans was because of the approval of transgenic soybeans and higher returns for farmers owing to their demand for edible oil and protein concentrate for livestock feeding.

- Canada had an area of 11.8 million hectares under the cultivation of oilseeds segment in 2022, of which 77.4% of the acreage was occupied by canola. Canada is the largest producer of canola in the world. The demand for canola as vegetable oil and feed is anticipated to drive the area under canola cultivation during the forecast period. However, in Mexico, other oilseeds such as safflower, castor, and linseed have a major share. The area under safflower cultivation has increased because of the demand for its oil and the shift from cotton to oilseeds, as GM cotton is banned.

- Therefore, the increase in the number of edible oil and feed applications is driving the area under oilseed cultivation in the region.

North America Oilseed (seed For Sowing) Industry Overview

The North America Oilseed Market (seed For Sowing) is fairly consolidated, with the top five companies occupying 76.34%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Land O'Lakes Inc. and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92517

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.2 Most Popular Traits

- 4.2.1 Soybean

- 4.3 Breeding Techniques

- 4.3.1 Row Crops

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.1.2.3 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Crop

- 5.2.1 Canola, Rapeseed & Mustard

- 5.2.2 Soybean

- 5.2.3 Sunflower

- 5.2.4 Other Oilseeds

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Groupe Limagrain

- 6.4.6 Land O'Lakes Inc.

- 6.4.7 Nufarm

- 6.4.8 S&W Seed Co.

- 6.4.9 Stine Seed Company

- 6.4.10 Syngenta Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.