Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693443

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693443

Oilseed (seed For Sowing) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 488 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

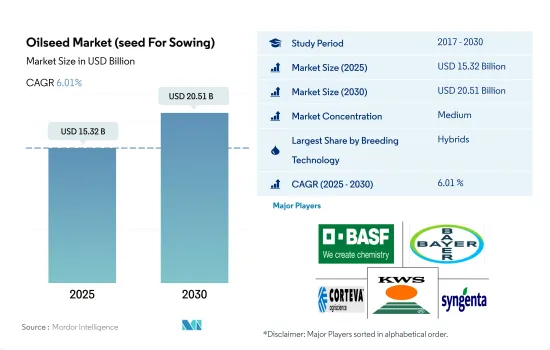

The Oilseed Market (seed For Sowing) size is estimated at 15.32 billion USD in 2025, and is expected to reach 20.51 billion USD by 2030, growing at a CAGR of 6.01% during the forecast period (2025-2030).

Hybrids dominated the market due to the higher yield, pest resistance, and improved oil quality traits

- Globally, hybrids accounted for a higher share than open-pollinated varieties because hybrid seeds are high-yielding, adaptable to different regions and weather conditions, pest resistant, and high-quality oil crops are produced by using hybrid seeds.

- Among the hybrids, transgenic hybrid seeds dominated the global oilseed market, with a share of 56.2% in 2022, which increased by 72.5% during 2017- 2022. This is due to the growing acceptance of transgenic seeds worldwide as well as the increase in areas under cultivation as farmers are increasingly using them to meet the required production.

- Globally, in 2022, the non-transgenic share was 43.8% of the hybrid oilseed market because of the transgenic crops banned in Europe and growing awareness among the people about the benefits of consuming non-GMO food.

- In 2022, the herbicide-tolerant hybrid seed market accounted for 76.5% of the global transgenic oilseed market, with soybean being the largest market, valued at USD 4.75 billion, followed by canola with USD 810.8 million in 2022. Among the transgenic crop traits for oilseeds, the herbicide-tolerant trait is the most adopted by farmers, as weeds are the major problem in crop production and cause a reduction of 20%-25% in crop yield.

- Open-pollinated seed varieties are used less compared to hybrid seed varieties because open-pollinated seed varieties are not resistant to diseases and can be attacked easily by weeds. Thus, to minimize crop loss due to weeds and insects, growers use hybrid seed traits that have characteristics such as disease tolerance and insect resistance. Thus, benefits such as higher yield and resistance to pets drive the hybrid seed segment during the forecast period.

North America dominated the global oilseed market, with soybean, canola, and sunflower having higher shares

- Oilseed crops contributed 19.6% of the global seed market in 2022, which was an increase of 29.5% during the historical period.

- In 2022, North America was the largest producer of oilseeds and accounted for USD 5.2 billion. The United States was the largest country in the region, which accounted for 30% of the global oilseed market in 2022 because of the demand from export markets, the availability of high-yield seed varieties, and an increase in global demand for protein-rich feeds.

- China was the second largest country, which accounted for 14.4% of the global oilseed market in 2022. The Chinese oilseeds market is dominated by soybean, canola, rapeseed, and mustard crops, which accounted for 74.7% and 16.1% of the market in 2022, respectively.

- South America had a market of USD 3.04 billion in the global oilseed market in 2022 due to an increase in the cultivation area and leading producers of oilseed crops, such as Brazil and Argentina, which together accounted for 16.7% of the global oilseed market.

- In Europe, oil seeds contributed USD 1.5 billion to the region's seed market in 2022. Sunflower and soybean are the major oilseed crops in the region, which were dominated by Russia, Ukraine, and Turkey in 2022.

- Africa accounted for USD 497.3 million in the oilseed market in 2022. South Africa occupied a major share, which accounted for 42.2% of the African oilseed market in 2022 due to the increase in the prices and demand from consumers and the expansion of edible oil processing plants.

- An increase in the prices, demand from consumers, and the expansion of edible oil processing plants are driving the oilseed market in the region. Thus, the oilseed market is estimated to grow in the forecast period.

Global Oilseed Market (seed For Sowing) Trends

Soybean dominated the area under oilseeds due to the increased demand from the feed sector, increase in export margins, and reasonable prices

- Oilseeds accounted for 18.4% of global row crop acreage (1.5 billion hectares) in 2022. Soybeans accounted for most oilseed acreage, followed by rapeseed and sunflower. The area under cultivation for oilseeds increased by 9% between 2017 and 2022 and reached 289.6 million hectares in 2022, which is mainly due to increased demand for oilseeds with attractive prices. Globally, South America and North America had the largest share of soybean cultivation acreage, which accounted for 76.4% in 2022. However, the acreage of the soybean fluctuated due to poor market prices in these regions.

- In Asia-Pacific, the area under soybean cultivation was 16.2 million hectares in 2017, which increased to 19.2 million ha in 2022. The increase in the area was due to the increased demand from the livestock feed sector, an increase in export margins, and convenient prices in the domestic and international markets. The acreage is estimated to increase during the forecast period.

- Sunflowers are one of the major oilseed crops cultivated globally. Europe accounted for a large portion of the acreage in global sunflowers. Between 2017 and 2022, the area under cultivation of sunflowers increased by 21.5%. Farmers in Hungary, Bulgaria, the Czech Republic, and Slovakia led this trend because sunflower seeds were selling for high prices.

- Asia-Pacific is the major region in the other oilseed segment. The area under other oilseeds cultivation was 32.7 million hectares in 2022. The increased demand for groundnuts, castor, linseed consumption, and affordable prices on both domestic and foreign markets are estimated to drive the acreage in the region. Thus, increased demand from processing industries and higher prices for oilseeds are estimated to drive the seeds market during the forecast period.

The increasing demand for sunflower oil and the higher demand for soybean from various industries drive the need for disease-resistant, wider adaptability, and high oleic and linoleic content varieties

- Soybean seed is majorly cultivated in countries such as the United States, Brazil, and China due to favorable weather conditions. Traits such as disease resistance, drought tolerance, high yielding, and high oleic content have been gaining popularity due to changes in the climate and soil conditions with high demand for soybean from oil processing companies and preventing southern-stem canker, Root-Knot Nematode (RKN), and Phytophthora sojae. For instance, Land O' Lakes has seed varieties under the brand Enlist and Roundup Ready to meet the increasing demand for improved seed varieties. Other major companies such as Corteva Agriscience, KWS SAAT SE & Co. KGaA, Land O'Lakes, Burrus Seeds, and Syngenta AG offer these seed traits.

- Sunflower is one of the major oilseed crops widely cultivated. In the United States, 10%-20% of sunflower production is used in shelled kernels, whole seeds, and nut and fruit mixes containing sunflower seed. Kernels are also used in processed foods, such as granola bars and bread. The demand for seed varieties with improved traits is expected to increase during the forecast period. Moreover, high oil content with oleic and linoleic has significant demand. The demand for sunflower oil is increasing after a ban on palm oil. Thus, the high oil content increases the demand for crops such as sunflowers and increases the higher income returns. Products such as 65A25, P62LL109, LG 50760 CL, and Xi Arko by companies such as Corteva Agriscience, Groupe Limagrain, and Syngenta AG contain this trait.

- The availability of new hybrid seed varieties by companies with advanced traits, such as higher resistance to viruses and high demand by processing industries, is expected to help in the growth of the market during the forecast period.

Oilseed (seed For Sowing) Industry Overview

The Oilseed Market (seed For Sowing) is moderately consolidated, with the top five companies occupying 54.67%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, KWS SAAT SE & Co. KGaA and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92505

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.2 Most Popular Traits

- 4.2.1 Soybean & Sunflower

- 4.3 Breeding Techniques

- 4.3.1 Row Crops

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.1.2.3 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Crop

- 5.2.1 Canola, Rapeseed & Mustard

- 5.2.2 Soybean

- 5.2.3 Sunflower

- 5.2.4 Other Oilseeds

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Breeding Technology

- 5.3.1.2 By Crop

- 5.3.1.3 By Country

- 5.3.1.3.1 Egypt

- 5.3.1.3.2 Ethiopia

- 5.3.1.3.3 Ghana

- 5.3.1.3.4 Kenya

- 5.3.1.3.5 Nigeria

- 5.3.1.3.6 South Africa

- 5.3.1.3.7 Tanzania

- 5.3.1.3.8 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Breeding Technology

- 5.3.2.2 By Crop

- 5.3.2.3 By Country

- 5.3.2.3.1 Australia

- 5.3.2.3.2 Bangladesh

- 5.3.2.3.3 China

- 5.3.2.3.4 India

- 5.3.2.3.5 Indonesia

- 5.3.2.3.6 Japan

- 5.3.2.3.7 Myanmar

- 5.3.2.3.8 Pakistan

- 5.3.2.3.9 Philippines

- 5.3.2.3.10 Thailand

- 5.3.2.3.11 Vietnam

- 5.3.2.3.12 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Breeding Technology

- 5.3.3.2 By Crop

- 5.3.3.3 By Country

- 5.3.3.3.1 France

- 5.3.3.3.2 Germany

- 5.3.3.3.3 Italy

- 5.3.3.3.4 Netherlands

- 5.3.3.3.5 Poland

- 5.3.3.3.6 Romania

- 5.3.3.3.7 Russia

- 5.3.3.3.8 Spain

- 5.3.3.3.9 Turkey

- 5.3.3.3.10 Ukraine

- 5.3.3.3.11 United Kingdom

- 5.3.3.3.12 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 By Breeding Technology

- 5.3.4.2 By Crop

- 5.3.4.3 By Country

- 5.3.4.3.1 Iran

- 5.3.4.3.2 Saudi Arabia

- 5.3.4.3.3 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 By Breeding Technology

- 5.3.5.2 By Crop

- 5.3.5.3 By Country

- 5.3.5.3.1 Canada

- 5.3.5.3.2 Mexico

- 5.3.5.3.3 United States

- 5.3.5.3.4 Rest of North America

- 5.3.6 South America

- 5.3.6.1 By Breeding Technology

- 5.3.6.2 By Crop

- 5.3.6.3 By Country

- 5.3.6.3.1 Argentina

- 5.3.6.3.2 Brazil

- 5.3.6.3.3 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Euralis Semences

- 6.4.6 Groupe Limagrain

- 6.4.7 KWS SAAT SE & Co. KGaA

- 6.4.8 Nufarm

- 6.4.9 RAGT Group

- 6.4.10 Syngenta Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.