Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693431

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693431

Processed Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 422 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

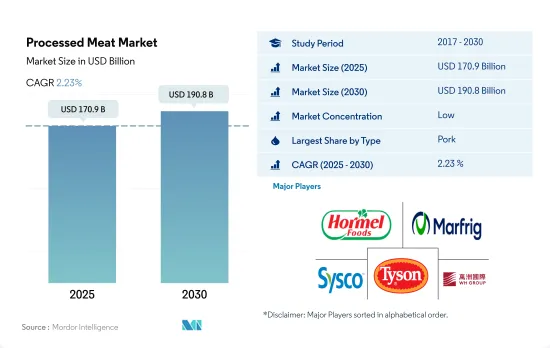

The Processed Meat Market size is estimated at 170.9 billion USD in 2025, and is expected to reach 190.8 billion USD by 2030, growing at a CAGR of 2.23% during the forecast period (2025-2030).

Innovations in the meat industry drive the market

- Processed meat has been growing at a steady rate. It registered a CAGR of 15.38% from 2017 to 2022. The most consumed processed meat type is processed pork. Even though some communities or regions do not consume pork, it is the most consumed meat in Europe and Asia and the second most consumed worldwide, after poultry. Lunch meats, hot dogs, bacon, sausage, smoked ham, and other processed pork make up the category of processed pork. Considering various ethnicities, processed pork is particularly popular among the African-American and Hispanic communities.

- The mutton meat category is expected to be the fastest-growing processed meat segment, recording a CAGR of 2.74% during the forecast period. The mutton processed meat sector focuses on the ongoing demand of consumers for healthier processed meats. The approaches are either focused on decreasing the number of unhealthy ingredients, such as less sodium chloride, nitrite, and nitrate, or raising the number of ingredients that have positive health effects, such as replacing nitrate with other curing agents, like celery powder.

- In terms of off-trade channels, processed meat products were primarily sold through retail outlets like supermarkets. In 2022, pork sales represented 63.96% of the total value of meat sold, while beef meat contributed 21.31% through the off-trade channel. It is because of innovations in meat products occurring globally. Commercial meat snacking has experienced a massive explosion in the last few years. Some examples of meat-snacking products that have gained popularity include My Protein's beef biltong, Vital Proteins' beef liver, Jim's Jerky, The Stock Merchant's Grass Fed Beef Stock, and Protein Kick's Peperami Beef Bars.

Increased domestic production is propelling the market growth

- Sales for processed meat around the world are growing at a moderate growth rate, which observed a Y-o-Y growth rate of 3.42% in 2022. The demand for prepared and processed goods, especially processed meats, is rising throughout Asia as customers have embraced the convenience of these goods as they become more time-constrained. From 2017 to 2022, revenues climbed by 23.4%. Countries are focusing on increasing domestic production to reduce the retail prices for meat products. China's pork production increased by 4.6% Year-on-Year in 2022, reaching 55.41 million tons, and nearly 700 million pigs were slaughtered.

- Europe held the second highest share in the market in 2022 owing to the growing consumer awareness of the dangers of using nitrate as a curing agent in processed meat, which is driving up demand for nitrite-free processed meat products like bacon in European nations, which boosted sales by 6.12% between 2020 and 2022. The processed meat market is competitive and comprises many regional and international competitors, which are dominated by players like Hormel Foods Corporation, Conagra Brands Inc., and WH Group Limited.

- Africa is projected to be the fastest-growing region with a CAGR of 4.88% by value during the forecasted period. Owing to the rising demand among consumers, the domestic poultry meat supply in South Africa increased from 1,707 thousand tons in 2018 to 1,947 thousand tons in 2022, which is growing at an average annual rate of 2.80% due to investments in production facilities and poultry farms. Domestic production in Africa increased by 13.8% from 2017 to 2022 due to investments in production facilities and poultry farms. Moreover, poultry is the second most consumed meat in Africa, with a per capita consumption of 34.79 kg/capita.

Global Processed Meat Market Trends

Production across regions is likely to boost a growth in demand

- Beef production grew by 6.90% between 2017 and 2022. Global beef production for 2023 is anticipated to increase by nearly 1% to 59.6 million tons, according to USDA's April 2022 forecast. The drought in Argentina has led to more herd break-ups and increased production by 6% compared to the previous year. Similarly, larger fattening stalls and higher slaughter of cows are expected to boost US production by 1% from April 2022. New Zealand production will increase by 3% as male dairy calves are now marketed for beef.

- Due to the high input costs, EU production is cut by 1% due to lower slaughter numbers and lower weights. Upward revisions in forecasts for New Zealand, Australia, Argentina, and Brazil offset declines in forecasts for Mexico, the United Kingdom, and the European Union. Strong demand from China is expected to attract supplies from Brazil and Argentina. Australia is likely to benefit from increasing demand from Japan and South Korea. Additionally, strong US demand for processed beef will boost supplies from Australia and New Zealand.

- Beef production is dominated by North America, which produced 32.13% in 2022. Beef production in North America was highly impacted by the increased production costs and increased feed expenses due to dry conditions. The drought also negatively affected locations in western North America. On January 1, 2022, in Canada, beef cow inventories were down by 1% for the fifth consecutive year, reaching 3.5 million heads. The total US cattle inventories were down by 2% compared to last year, reaching 91.9 million heads. South America also caters to global beef production, producing almost 20.12% of global beef production in 2022. The increased beef demand worldwide increased production and productivity gains.

Production uncertainties across regions are impacting the prices

- The average global price of beef increased by 9.15% between 2017 and 2022, with the United States accounting for the highest price at USD 6.93/kg. Beef has faced strong demand and high prices worldwide, with a visible change in international market dynamics. Local disruptions, such as droughts and increasing consumer demand in individual countries or regions, now exert a greater impact on global trade.

- Key drivers influencing prices in top beef-producing countries include a demand-driven surge in beef prices in the United States. The US beef sector has clearly been in a demand-driven market, witnessing a 40.75% price increase in 2022 compared to 2017. In Brazil, a delay in seasonal rains leads to the production of fewer cattle, forcing processors to raise cattle prices and maintain supply, particularly given demand in the Chinese market. The market faced a reduction in livestock supply across the European Union, resulting in poor profitability of the sector. In June 2023, the retail prices of different forms of beef in the United States were USD 5.028/lb for ground beef, USD 7.020/lb for uncooked beef roasts, and USD 10.359/lb for beef steaks.

- In China, slow growth in domestic beef production, which failed to keep up with local consumption growth prompted by pork-to-beef substitution during the African swine fever outbreak, led to rising beef imports in 2021 and 2022, which, in turn, led to a rise in prices in the country. Australia's supply also impacted the world market, as consecutive years of drought and large herd liquidations resulted in the country's lowest cattle population in 30 years. Australian young stock prices were up by almost 20% in February 2021 compared to the previous year.

Processed Meat Industry Overview

The Processed Meat Market is fragmented, with the top five companies occupying 21.78%. The major players in this market are Hormel Foods Corporation, Marfrig Global Foods S.A., Sysco Corporation, Tyson Foods Inc. and WH Group Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92490

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Beef

- 3.1.2 Mutton

- 3.1.3 Pork

- 3.1.4 Poultry

- 3.2 Production Trends

- 3.2.1 Beef

- 3.2.2 Mutton

- 3.2.3 Pork

- 3.2.4 Poultry

- 3.3 Regulatory Framework

- 3.3.1 Canada

- 3.3.2 Mexico

- 3.3.3 United States

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Type

- 4.1.1 Beef

- 4.1.2 Mutton

- 4.1.3 Pork

- 4.1.4 Poultry

- 4.1.5 Other Meat

- 4.2 Distribution Channel

- 4.2.1 Off-Trade

- 4.2.1.1 Convenience Stores

- 4.2.1.2 Online Channel

- 4.2.1.3 Supermarkets and Hypermarkets

- 4.2.1.4 Others

- 4.2.2 On-Trade

- 4.2.1 Off-Trade

- 4.3 Region

- 4.3.1 Africa

- 4.3.1.1 By Type

- 4.3.1.2 By Distribution Channel

- 4.3.1.3 By Country

- 4.3.1.3.1 Egypt

- 4.3.1.3.2 Nigeria

- 4.3.1.3.3 South Africa

- 4.3.1.3.4 Rest of Africa

- 4.3.2 Asia-Pacific

- 4.3.2.1 By Type

- 4.3.2.2 By Distribution Channel

- 4.3.2.3 By Country

- 4.3.2.3.1 Australia

- 4.3.2.3.2 China

- 4.3.2.3.3 India

- 4.3.2.3.4 Indonesia

- 4.3.2.3.5 Japan

- 4.3.2.3.6 Malaysia

- 4.3.2.3.7 South Korea

- 4.3.2.3.8 Rest of Asia-Pacific

- 4.3.3 Europe

- 4.3.3.1 By Type

- 4.3.3.2 By Distribution Channel

- 4.3.3.3 By Country

- 4.3.3.3.1 France

- 4.3.3.3.2 Germany

- 4.3.3.3.3 Italy

- 4.3.3.3.4 Netherlands

- 4.3.3.3.5 Russia

- 4.3.3.3.6 Spain

- 4.3.3.3.7 United Kingdom

- 4.3.3.3.8 Rest of Europe

- 4.3.4 Middle East

- 4.3.4.1 By Type

- 4.3.4.2 By Distribution Channel

- 4.3.4.3 By Country

- 4.3.4.3.1 Bahrain

- 4.3.4.3.2 Kuwait

- 4.3.4.3.3 Oman

- 4.3.4.3.4 Qatar

- 4.3.4.3.5 Saudi Arabia

- 4.3.4.3.6 United Arab Emirates

- 4.3.4.3.7 Rest of Middle East

- 4.3.5 North America

- 4.3.5.1 By Type

- 4.3.5.2 By Distribution Channel

- 4.3.5.3 By Country

- 4.3.5.3.1 Canada

- 4.3.5.3.2 Mexico

- 4.3.5.3.3 United States

- 4.3.5.3.4 Rest of North America

- 4.3.6 South America

- 4.3.6.1 By Type

- 4.3.6.2 By Distribution Channel

- 4.3.6.3 By Country

- 4.3.6.3.1 Argentina

- 4.3.6.3.2 Brazil

- 4.3.6.3.3 Rest of South America

- 4.3.1 Africa

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 BRF S.A.

- 5.4.2 Cargill Inc.

- 5.4.3 COFCO Corporation

- 5.4.4 Conagra Brands Inc.

- 5.4.5 Hormel Foods Corporation

- 5.4.6 Itoham Yonekyu Holdings, Inc.

- 5.4.7 JBS SA

- 5.4.8 Marfrig Global Foods S.A.

- 5.4.9 OSI Group

- 5.4.10 Sysco Corporation

- 5.4.11 The Kraft Heinz Company

- 5.4.12 Tyson Foods Inc.

- 5.4.13 Wen's Food Group Co. Ltd

- 5.4.14 WH Group Limited

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.