Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692139

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692139

Europe Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 300 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

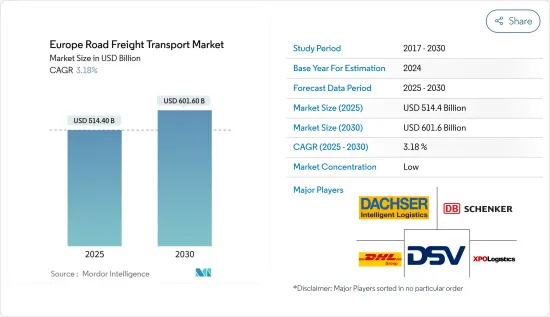

The Europe Road Freight Transport Market size is estimated at 496.83 billion USD in 2024, and is expected to reach 601.59 billion USD by 2030, growing at a CAGR of 3.24% during the forecast period (2024-2030).

Retail e-commerce surge driving advancements in the wholesale and retail trade end user segment

- In 2022, the manufacturing end-user segment grew due to the rise in human-robot collaboration, which boosted production. Germany is the fifth largest robot market globally, with 22,000 industrial robots utilized in various industries, accounting for 6% of the global robot installations as of 2021. Moreover, in 2021, the Schwarz Group, a German food retailer, emerged as the foremost retail company in Europe, with a total revenue of USD 153.75 billion within the region. In Germany, the retail sales of consumer durables were projected to increase by 1.50% YoY in 2022. This was supported by an estimated 5.40% increase in private consumption in 2022.

- In Europe's oil and gas, mining, and quarrying sectors, German regasification plans are one of the factors driving growth in the oil and gas end-user segments. Russia supplies the country's natural gas needs. As a result, Germany is expected to add the highest LNG regasification capacity in Europe between 2022 and 2026, accounting for 36% of the region's total capacity additions by 2026. In 2022, Italy's net energy import costs are expected to more than double, reaching USD 113.24 billion.

- The wholesale and retail trade end-user segment is poised for substantial growth in the upcoming years, primarily driven by the anticipated expansion of the European e-commerce industry, projected to register a compounded annual growth rate (CAGR) of 8.85 from 2023 to 2027. In the context of the German e-commerce landscape, it is projected that the market will encompass 68.4 million users by 2025, achieving a penetration rate of 81.9%, marking an increase from 80.1% in 2022.

Increasing road freight volume transported across Europe and government initiatives to develop the infrastructure are driving the growth in the market

- In 2022, the EU and extra-EU tons transported by international road freight transportation in France were major. For instance, the total EU/extra-EU transported by road between France and Switzerland held a share of 7.3% of the total tonnage transported by road, and the total EU/extra-EU transported by road between France and the United Kingdom held a share of 6.5% in 2022. Road haulage transported 68.1% of Italian goods during the first half of 2022, resulting in a 1.5% increase in transport (measured in tonne-km) compared to the previous year. The number of companies in the Italian road haulage sector reached approximately 100,797 units at the end of 2022, a rise of 1.34% from 99,465 at the end of 2021.

- The road freight transport market employs about 430,000 employees in Germany in about 35,000 road freight companies, which has been stable over the past five years. The fleet with a carrying capacity of 3.5 tons in 2021 was 964,696 in Germany and had a growth of 1.3% compared to 2020 and 3.4% over five years. The declining activity in all major economies and inflation, which led to a rise in fuel and wage costs, resulted in the decline of freight transportation through trucks between the 27th and 30th week of 2022 in the Netherlands. Since week 25, the weekly decrease in the movement of trucks was 9-21% lower than the same week in 2021.

- In the Nordics, the overseas shipments of trucks increased by 6.7% in 2022. The main destinations for truck exports from Denmark are the Netherlands, Poland, and Germany, with a combined 54% share of total exports. In the UK, the top five countries for exports and imports have remained relatively constant over time. However, exports to Germany decreased from 1.4 million tons in 2000 to 0.19 million tons in 2021.

Europe Road Freight Transport Market Trends

European Union allocated USD 5.76 billion to 135 transportation projects to boost economic recovery

- The transportation and warehouse sector plays a crucial role in supporting operations across various industries, with Germany leading as the dominant player, surpassing France and the United Kingdom. Globally, Germany ranks third in both imports and exports of goods. The German federal government expressed its intention to increase investments in transportation infrastructure, allocating over EUR 12 billion (USD 12.80 billion) for federal highways and around EUR 1.7 billion (USD 1.81 billion) for waterways in 2022, thereby demonstrating its commitment to improving transportation networks.

- The German government intends to invest more in rail than road network. In 2022, Deutsche Bahn, the federal government, and the local and regional governments invested roughly EUR 13.6 billion (USD 14.51 billion) in rail infrastructure. Lower Saxony, Hamburg, Bremen, Mecklenburg-Western Pomerania, and Schleswig-Holstein are partnering with DB to invest in modernizing their rail network by 2030.

- In 2022, the European Union approved EUR 5.4 billion through grants for approximately 135 transport infrastructural projects. These projects aim to aid post-pandemic economic recovery in the EU Member States, enhance transport links, promote sustainable transportation, boost safety, and create job opportunities. All supported projects are part of the Trans-European Transport Network, which connects EU Member States and aligns with the European Union's goal of completing the TEN-T core network by 2030 and the comprehensive network by 2050, all while aligning with climate objectives outlined in the European Green Deal.

Since February 2023, diesel imports from the Middle East, Asia, and North America have increased due to the ban on imports from Russia

- Gasoline prices surpassed EUR 2 (USD 2.13) per liter in most of the 19 eurozone countries in Q1 2022. The main reason behind the increased prices was supply issues due to the conflict between Russia and Ukraine, as Russia supplied more than a quarter of the EU's petroleum needs. In 2021, the average price for a liter of gasoline in the eurozone was EUR 1.30 (USD 1.38); at the start of 2022, the price was about EUR 1.55 (USD 1.65) per liter.

- Russia has been Europe's largest supplier of diesel. In 2023, diesel prices declined in Europe. Since February 2023, when the European Union implemented the ban on petroleum product imports from Russia, diesel exports from Russia to Europe have averaged 24,000 barrels per day (b/d), down by 96% from the 630,000 b/d Russia sent to Europe in 2022. From February through May, diesel exports to Europe increased by 51% (160,000 b/d) from the Middle East, by 97% (147,000 b/d) from Asia, and by 65% (47,000 b/d) from North America.

- Denmark is the most expensive country for petrol, and Finland is the most expensive for diesel. Austria has the cheapest petrol, and Spain is the cheapest for diesel. Fuel prices in the United Kingdom reached record highs in 2022, with the average price of petrol hitting 191.53 p-per-litre and diesel reaching 199.05 p-per-litre in July. The average cost of petrol at UK forecourts has risen to break 150p a liter (USD 1.80) since the start of 2023, and diesel has risen to 152.41p a liter (USD 1.83). Spanish fuel prices were lower than in the United Kingdom by about 20 cents per liter for petrol and 40 cents per liter for diesel in January 2023.

Europe Road Freight Transport Industry Overview

The Europe Road Freight Transport Market is fragmented, with the top five companies occupying 5.99%. The major players in this market are Dachser, DB Schenker, DHL Group, DSV A/S (De Sammensluttede Vognmaend af Air and Sea) and XPO, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90833

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 GDP Distribution By Economic Activity

- 4.2 GDP Growth By Economic Activity

- 4.3 Economic Performance And Profile

- 4.3.1 Trends in E-Commerce Industry

- 4.3.2 Trends in Manufacturing Industry

- 4.4 Transport And Storage Sector GDP

- 4.5 Logistics Performance

- 4.5.1 Albania

- 4.5.2 Bulgaria

- 4.5.3 Croatia

- 4.5.4 Czech Republic

- 4.5.5 Denmark

- 4.5.6 Estonia

- 4.5.7 Finland

- 4.5.8 France

- 4.5.9 Germany

- 4.5.10 Hungary

- 4.5.11 Iceland

- 4.5.12 Italy

- 4.5.13 Latvia

- 4.5.14 Lithuania

- 4.5.15 Netherlands

- 4.5.16 Norway

- 4.5.17 Poland

- 4.5.18 Romania

- 4.5.19 Russia

- 4.5.20 Slovak Republic

- 4.5.21 Slovenia

- 4.5.22 Spain

- 4.5.23 Sweden

- 4.5.24 Switzerland

- 4.5.25 United Kingdom

- 4.6 Length Of Roads

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Pricing Trends

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Major Truck Suppliers

- 4.13 Road Freight Tonnage Trends

- 4.14 Road Freight Pricing Trends

- 4.15 Modal Share

- 4.16 Inflation

- 4.17 Regulatory Framework

- 4.18 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

- 5.8 Country

- 5.8.1 France

- 5.8.2 Germany

- 5.8.3 Italy

- 5.8.4 Netherlands

- 5.8.5 Nordics

- 5.8.6 Russia

- 5.8.7 Spain

- 5.8.8 United Kingdom

- 5.8.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 A.P. Moller - Maersk

- 6.4.2 C.H. Robinson

- 6.4.3 Dachser

- 6.4.4 DB Schenker

- 6.4.5 DHL Group

- 6.4.6 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.7 Kuehne + Nagel

- 6.4.8 Mainfreight

- 6.4.9 Scan Global Logistics

- 6.4.10 XPO, Inc.

7 KEY STRATEGIC QUESTIONS FOR ROAD FREIGHT CEOS

8 APPENDIX

- 8.1 Global Logistics Market Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.