Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692030

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692030

Soy Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 397 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

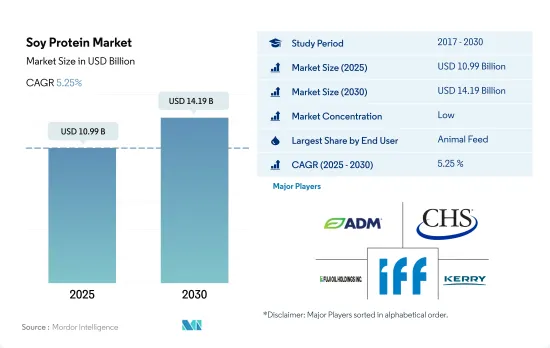

The Soy Protein Market size is estimated at 10.99 billion USD in 2025, and is expected to reach 14.19 billion USD by 2030, growing at a CAGR of 5.25% during the forecast period (2025-2030).

The suitability of soy protein due to its easier digestibility factor led to its dominance, mainly in the animal feed segment

- The usage of soy protein ingredients in animal feed marginally surpasses its usage in food and beverages. Soy protein, mainly in the form of concentrates, is widely used in the diets of animals, birds, and fish. Its main characteristics, such as easy digestibility, improved shelf life, and protein enrichment, are driving its application in the food and beverage segment. In 2022, the animal feed segment was largely driven by concentrates that addressed about 53.27% of soy protein needs.

- Food and beverage is another crucial application segment for soy protein, mainly in the meat/meat alternative subsegment. This is attributed to its multifunctionalities that mimic muscle texture when stacked in straight fibers, thus improving its use for texture and protein enrichment in meat alternatives. In 2023, the meat alternatives subsegment accounted for about 43.70% of the total soy protein sales in the food and beverage segment.

- In terms of growth, supplements remained the fastest-growing segment, with a projected CAGR of 6.31% by value during the forecast period, attributed to the growing number of fitness enthusiasts in developed economies like the United States, the United Kingdom, and Germany. The segment's growth can also be attributed to the increasing acceptance of soy protein in baby food and infant formula with the support of research studies. The EFSA (European Food Safety Authority), in its review of the essential composition of infant and follow-on formulae, states that isolated soy protein is a safe and suitable protein source for use in infant and follow-on formulae. In July 2022, Danone launched the new dairy and plant blend baby formula, in which 60% plant protein is sourced from high-quality/non-GMO soy protein.

Increasing demand for cost-effective protein products in North America and Asia-Pacific

- North America dominated the soy protein market, with most of its applications in the food and beverages segment. Meat and dairy alternatives led the demand, holding a volume share of 44% in 2022. This growth can be attributed to the increasing demand for plant-based products, especially in the United States and Canada, which had a combined vegan population of about 10 million in 2021. Being among the largest producers of soybeans, the United States widely contributes to the regional soy protein demand. In 2021, soybean production totaled a record-high 4.44 billion bushels, up by 5% from 2020.

- North America is followed by the Asia-Pacific region. China remained the largest consumer of soy protein in the region, attributed to high production capacity that reduces the ingredient's price and boosts volume consumption. About 70% of the world's supply of soy protein isolates, a primary ingredient in many plant-based foods, is processed in the Shandong province in China. This factor also enables immense innovation in the plant-based space, attracting more consumers to try the differentiated product offerings. The region is projected to record a CAGR of 5.67% by value during the forecast period.

- South America is projected to be the fastest-growing market as the demand for natural and sustainable ingredients is rapidly increasing due to rising health consciousness. The region is set to record a CAGR of 6.0% by value over the forecast period. Over the last few years, concerns about damage to the environment and unethical treatment of animals in intensive farming systems have increased among consumers, leading to increased demand for sustainable protein. This factor has led to the rising demand for plant proteins in most South American countries.

Global Soy Protein Market Trends

Due to several health benefits of plant protein-based diets, customers are moving toward vegan offerings

- Globally, consumers are shifting their dietary preferences. Notably, there is a growing preference for dairy and meat alternatives, especially among consumers in Europe and North America. In 2022, Europe led the way with plant-based milk accounting for 38% of total plant-based food sales, followed closely by plant-based meat. This evolving trend is boosting the number of flexitarian and vegan consumers and opening doors for manufacturers to innovate within the plant protein sector.

- The popularity of plant-based protein alternatives is due to their nutritional value and stems from growing concerns over environmental impact, ethics, and health. Proteins, known for their slower digestion compared to carbohydrates, play a crucial role in weight management by promoting a longer-lasting feeling of fullness with fewer calories. A new study reveals that over one billion people globally were living with obesity between 2022 and 2023.

- Moreover, the rising engagement of the younger population in sports and fitness activities, coupled with a growing trend of fortifying food and beverages with functional ingredients for added health benefits, is fueling the demand for plant-based proteins. In 2023, a record-high 242 million Americans aged 6 and older (nearly 80% of the population) participated in at least one sport or fitness activity, a 2.2% increase from 2022. This active lifestyle shift is driving the demand for plant-based protein food products. Furthermore, government initiatives, such as Canada's Health Ministry, which revamped its food guide, emphasizing three key categories: vegetables and fruits, whole grains, and plant-based proteins, are driving awareness and demand for alternative proteins among consumers.

Global soy production is surging, propelled by ideal growing conditions in specific countries

- Regardless of fluctuating production trends, soybeans, the fundamental raw material for soy proteins, are mostly produced in Brazil and closely followed by the United States and then Argentina. In 2018, 349 million tons of soy were produced worldwide. Brazil produced 118 million tons (34%), whereas the United States produced 123 million tons (35%) of the total. They made up 69% of the world's total production. A substantial reduction in soybean output was seen in 2012 due to the historic drought conditions in most of the Midwest over the summer. However, the output increased by 5% in 2020.

- Globally, India is another major producer of soybeans. India's soybean output for the harvesting season 2021-22 was 11.200 million tons, which rose from 10.450 million tons in the previous year. Due to flood-induced crop damage in major growing states, both corporate and government institutions involved in the soybean, soya oil, and oil meal business expected India's soybean output to stay lower in 2019-2020. Among the states, Madhya Pradesh is the top producer with 55.84 lakh ha, followed by Maharashtra (46.01 lakh ha), Rajasthan (10.62 lakh ha), Karnataka (3.82 lakh ha), Gujarat (2.24 lakh ha), and Telangana (1.51 lakh ha).

- In 2021, more than 75% of the soy produced worldwide was fed to animals for the production of meat and dairy products. Vegetable oils, industries, and biofuels make up the majority of the remainder. Only 7% of soy is used specifically to make products for human consumption, including tofu, soy milk, edamame beans, and tempeh.

Soy Protein Industry Overview

The Soy Protein Market is fragmented, with the top five companies occupying 28.75%. The major players in this market are Archer Daniels Midland Company, CHS Inc., Fuji Oil Group, International Flavors & Fragrances Inc. and Kerry Group PLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90229

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Plant

- 3.3 Production Trends

- 3.3.1 Plant

- 3.4 Regulatory Framework

- 3.4.1 Australia

- 3.4.2 Canada

- 3.4.3 China

- 3.4.4 France

- 3.4.5 Germany

- 3.4.6 India

- 3.4.7 Italy

- 3.4.8 Japan

- 3.4.9 United Kingdom

- 3.4.10 United States

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Isolates

- 4.1.3 Textured/Hydrolyzed

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Dairy and Dairy Alternative Products

- 4.2.2.1.6 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Supplements

- 4.2.3.1 By Sub End User

- 4.2.3.1.1 Baby Food and Infant Formula

- 4.2.3.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.3.1.3 Sport/Performance Nutrition

- 4.3 Region

- 4.3.1 Africa

- 4.3.1.1 By Form

- 4.3.1.2 By End User

- 4.3.1.3 By Country

- 4.3.1.3.1 Nigeria

- 4.3.1.3.2 South Africa

- 4.3.1.3.3 Rest of Africa

- 4.3.2 Asia-Pacific

- 4.3.2.1 By Form

- 4.3.2.2 By End User

- 4.3.2.3 By Country

- 4.3.2.3.1 Australia

- 4.3.2.3.2 China

- 4.3.2.3.3 India

- 4.3.2.3.4 Indonesia

- 4.3.2.3.5 Japan

- 4.3.2.3.6 Malaysia

- 4.3.2.3.7 New Zealand

- 4.3.2.3.8 South Korea

- 4.3.2.3.9 Thailand

- 4.3.2.3.10 Vietnam

- 4.3.2.3.11 Rest of Asia-Pacific

- 4.3.3 Europe

- 4.3.3.1 By Form

- 4.3.3.2 By End User

- 4.3.3.3 By Country

- 4.3.3.3.1 Belgium

- 4.3.3.3.2 France

- 4.3.3.3.3 Germany

- 4.3.3.3.4 Italy

- 4.3.3.3.5 Netherlands

- 4.3.3.3.6 Russia

- 4.3.3.3.7 Spain

- 4.3.3.3.8 Turkey

- 4.3.3.3.9 United Kingdom

- 4.3.3.3.10 Rest of Europe

- 4.3.4 Middle East

- 4.3.4.1 By Form

- 4.3.4.2 By End User

- 4.3.4.3 By Country

- 4.3.4.3.1 Iran

- 4.3.4.3.2 Saudi Arabia

- 4.3.4.3.3 United Arab Emirates

- 4.3.4.3.4 Rest of Middle East

- 4.3.5 North America

- 4.3.5.1 By Form

- 4.3.5.2 By End User

- 4.3.5.3 By Country

- 4.3.5.3.1 Canada

- 4.3.5.3.2 Mexico

- 4.3.5.3.3 United States

- 4.3.5.3.4 Rest of North America

- 4.3.6 South America

- 4.3.6.1 By Form

- 4.3.6.2 By End User

- 4.3.6.3 By Country

- 4.3.6.3.1 Argentina

- 4.3.6.3.2 Brazil

- 4.3.6.3.3 Rest of South America

- 4.3.1 Africa

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 A. Costantino & C. SpA

- 5.4.2 Archer Daniels Midland Company

- 5.4.3 Bunge Limited

- 5.4.4 CHS Inc.

- 5.4.5 Fuji Oil Group

- 5.4.6 International Flavors & Fragrances Inc.

- 5.4.7 Kerry Group PLC

- 5.4.8 Wilmar International Ltd

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.