Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683498

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683498

Asia-Pacific Soy Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 240 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

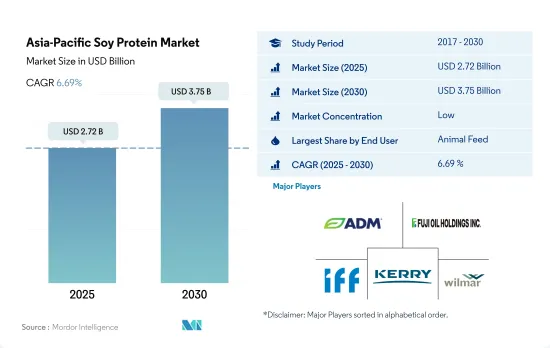

The Asia-Pacific Soy Protein Market size is estimated at 2.72 billion USD in 2025, and is expected to reach 3.75 billion USD by 2030, growing at a CAGR of 6.69% during the forecast period (2025-2030).

F&B and animal feed hold major applications of soy protein due to their high nutritional properties

- Asia-Pacific boasts a well-established soy protein market, with consumers in the region embracing it as a traditional staple. Soy protein, known for its versatility as both a protein source and flavor enhancer, finds extensive use across various end-user segments. Notably, the animal feed segment leads in soy protein utilization, closely followed by the food and beverage industry.

- Within animal feed, soy protein shines as a dairy and fishmeal substitute, prized for its high digestibility, cost-effectiveness, low anti-nutritional factors, and extended shelf life. Consequently, the animal feed segment is poised to exhibit the swiftest growth, with a projected CAGR of 6.23%. Soy protein's digestibility makes it a favored ingredient in pet foods, especially for dogs with allergies to traditional proteins like chicken or beef. Soy, rich in protein, fiber, vitamins, and minerals, serves as a nutritious meat alternative, with half a cup of cooked textured soy protein packing 11 grams of protein.

- In the food and beverage (F&B) industry, soy protein finds its niche in meat and dairy substitutes. Meat and dairy alternatives collectively hold a significant share in the F&B industry, with meat and its substitutes claiming 46.24% and dairy and its alternatives close behind at 36.72%. Soybeans, being a protein powerhouse with a meat-like texture and easy digestibility, are the primary drivers for their adoption. Additionally, soy-fortified milk, offering a nutrient profile akin to cow's milk with comparable protein, calcium, and vitamins A, D, and B, is witnessing a surge in demand.

China holds significant share in soy protein consumption due to high production capacity

- China, with its robust production capacity, stands as the leading consumer of soy protein in the region. This capacity not only drives down soy protein prices but also amplifies consumption. Notably, Shandong Province, China, processes a staggering 70% of the global supply of soy protein isolate, a key component in many plant-based foods. This concentration fosters a hotbed for product innovations, luring in more consumers with diverse offerings. Soy protein, besides being a viable alternative to animal-derived meals, boasts attributes like high digestibility and minimal anti-nutritional factors.

- With a surge in consumer appetite for vegan foods and a landscape ripe with product innovations, China is poised to lead the pack with a projected CAGR volume growth of 8.11%. Meanwhile, India's soy protein landscape is vibrant, with over 200 plant-based ingredients finding their way into startups. In 2022, the food and beverage industry, along with animal feed, commanded significant shares of 56.68% and 43.09%, respectively. Bolstered by entities like FSSAI championing soy protein consumption, India's appetite for soy protein is set to rise.

- Indonesia, a key player in the soy market, is gearing up for a steady growth trajectory, with a projected CAGR value of 2.22%. The nation is intensifying its efforts to bolster soybean production, aiming for self-sufficiency. Initiatives like Gema Palagung, Bangkit Kedelai, and Farmer's School for Integrated Crop Management underscore Indonesia's commitment to meeting the surging demand for protein-rich products. This push aligns well with the rising consumer interest in soy protein, fueled by a heightened focus on wellness and nutrition in daily diets.

Asia-Pacific Soy Protein Market Trends

The consumption growth of plant protein fuels opportunities for key players in the plant protein ingredients segment

- Plant proteins are gaining interest in the Asia-Pacific market as awareness and proof of their benefits are rising in the region. Among all plant proteins, soy proteins occupy the market share with the increased acceptability of the ingredients in different foods and their increased production. The volume of soybean meal consumption in China in 2020-21 was 72.68 MMT, which was around 9% more than in 2018. High investments in research, rapid technological advancements, and advanced innovation techniques are some of the major factors resulting in the use of developed protein ingredients, including soy proteins.

- Major drivers of allergen-free plant proteins such as soy, pea, hemp, and potato are the rising adoption of a vegetarian lifestyle, increasing demand for lactose-free and gluten-free products, and growing concerns about health-related problems. Around 81% of Indian consumers restrained meat from their diet in 2021. Major benefits of plant protein ingredients over animal proteins include high nutritional value, being a good source of several vitamins and minerals, technological advancements in various food industries, and increasing demand for natural and organic substitutes, which are expected to change consumer preferences.

- The increasing consumption of plant proteins and consumer acceptance in the region are driving manufacturers to innovate products fortified with these ingredients. Major grains consumed in Japan are soybeans, rice, and wheat, along with some other types like corn and peas. The rise in plant-based protein is expected to continue to provide opportunities for food manufacturers in the coming years.

India is one of the top five soybean producers in the world

- The graph given shows the production of soybeans in Asia-Pacific. A rise in maize production in China is leading to a decline in soybean production. Domestic soybean production is expected to decline by 1 MMT to 17.5 MMT due to farmers moving toward corn owing to soybean's high price. China's imports of soybeans increased by 2 million tons to 102 million tonnes for 2021-2022 due to a slight increase in feed demand. In addition, China's recovery from the swine fever outbreak resulted in increased use of soybean meal for food during the period. Increasing soybean crushing is expected to constrain vegetable oil imports over the forecast period.

- India is one of the top five soybean producers in the world. In 2020, soybean production in India decreased by 8.09% over a decade, primarily due to the lower yield obtained from states like Madhya Pradesh, which is considered the primary soybean-growing state with excessive rainfall registered in recent years. The regular rainfall during harvesting and disease attacks severely affected the crop and led to low yields.

- Soybean is the most planted legume in Japan in terms of acreage (141,800 ha). Most soybeans are cultivated for dry seeds. To prevent the overproduction of rice, the Japanese government recommends the cultivation of soybeans instead of rice. Hence, soybeans are commonly seen in Japanese paddy fields. The production volume of soybeans increased to over 7,600 tons in 2020 compared to 2018. A few decades ago, Japanese farmers used to plant soybeans on a small scale, and seeding and harvesting were performed manually. However, with technological improvements, the mechanization of soybean cultivation became more widespread at production sites, encouraging the cultivation scale of soybeans to increase.

Asia-Pacific Soy Protein Industry Overview

The Asia-Pacific Soy Protein Market is fragmented, with the top five companies occupying 20.54%. The major players in this market are Archer Daniels Midland Company, Fuji Oil Group, International Flavors & Fragrances, Inc., Kerry Group PLC and Wilmar International Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90181

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Plant

- 3.3 Production Trends

- 3.3.1 Plant

- 3.4 Regulatory Framework

- 3.4.1 Australia

- 3.4.2 China

- 3.4.3 India

- 3.4.4 Japan

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Isolates

- 4.1.3 Textured/Hydrolyzed

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Dairy and Dairy Alternative Products

- 4.2.2.1.6 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Malaysia

- 4.3.7 New Zealand

- 4.3.8 South Korea

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.3.11 Rest of Asia-Pacific

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Archer Daniels Midland Company

- 5.4.2 Bunge Limited

- 5.4.3 CHS Inc.

- 5.4.4 Foodchem International Corporation

- 5.4.5 Fuji Oil Group

- 5.4.6 International Flavors & Fragrances, Inc.

- 5.4.7 Kerry Group PLC

- 5.4.8 Shandong Yuwang Industrial Co. Ltd

- 5.4.9 Wilmar International Ltd

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.