Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692026

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692026

Africa Animal Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 217 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

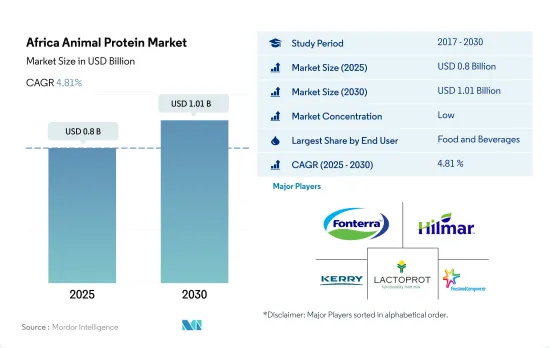

The Africa Animal Protein Market size is estimated at 0.8 billion USD in 2025, and is expected to reach 1.01 billion USD by 2030, growing at a CAGR of 4.81% during the forecast period (2025-2030).

Rising influx of affordable and high-quality products drive the food and beverages and personal care and cosmetics segment in the market

- By application, the food and beverages segment was the region's leading end-user segment for animal protein in 2022. The bakery and snacks sub-segment accounted for the major volume shares in the food and beverage segment, i.e., 27.14% and 23.58%, respectively, in 2022. Healthy snacking, rising demand for frozen snacks, and increased influx of affordable and high-quality private label products contribute to the growth of the snacks sub-segment. The health and wellness trend continued to support the growth of yogurt and other frozen snack products in South Africa since gelatin and whey protein is supposed to be highly nutritious and good at improving digestive health. Thus, the snacks sub-segment is projected to record a CAGR of 3.55% by value during the forecast period.

- However, the personal care segment is set to register the fastest CAGR of 5.95% by value during the forecast period. The increasing number of beauty clinics, rising per capita expenditure on personal appearance, robust regulatory framework, and the growing beauty and cosmetics market propel the region's demand for collagen ingredients.

- Supplements held the second position in the market. The sports and performance nutrition sub-segment, the fastest-growing sub-segment, aids the growth of supplements. It is projected to record a CAGR of 4.05%, by value, during the forecast period. African consumers are actively into sports, such as running and football, among other activities. There is a considerable portion of consumers in the region with gym memberships. For instance, in 2020, there were around 2,450 health clubs in South Africa. The increasing number of health and fitness centers has been positively influencing the growth of the sub-segment.

Rising demand for protein-enriched foods in countries like Nigeria and Rest of Africa segment draw the segmental demand

- The Rest of Africa (including Ethiopia, Kenya, Ghana, Guinea, and Ivory Coast) led the animal protein market in 2022. By protein type, whey protein dominated the market with a 32.30% volume share in 2022. The highest market demand was for whey protein-based functional snacks. Consumers in these countries are becoming increasingly concerned about healthy eating and prefer whey protein-based diets. They are opting for products like snack bars, protein-enriched cookies, and others to fulfill their nutritional requirements, thereby boosting the sub-segment's growth.

- However, Nigeria is projected to be the fastest-growing country for animal proteins, recording a CAGR of 6.94% during the forecast period. Gelatin was the most consumed protein in the country in 2022, with a value share of 27%. Gelatin is an easily digestible protein that caters to weight management and maintains a healthy immune system. These benefits have promoted its demand in the Nigerian animal protein market. Animal-based gelatin, particularly grass-fed beef gelatin, dominates the market as it contains no dangerous contaminants such as GMOs, pesticides, hormones, antibiotics, or chemical additives.

- South Africa held a minor share in the African animal protein market. It is projected to record a CAGR of 3.20% during the forecast period. Whey protein emerged as one of the country's major protein types among other animal proteins. It has major applications in the supplements segment, especially in the sports nutrition sub-segment, as it is ideal for muscle rehabilitation and pre-workout exercises.

Africa Animal Protein Market Trends

Per capita consumption of animal protein to witness significant growth due to growing health awareness and healthy eating habits of consumers

- This consumption is propelled by a rising health consciousness and a recent shift toward nutritious eating among consumers. The awareness among parents regarding the nutritional benefits of infant formulas, especially those derived from milk protein, is fueling their consumption. However, the market faces challenges from the increasing adoption of veganism and a notable prevalence of lactose intolerance. Since 2017, the market's growth has been sluggish, attributed in part to shifts in South African legislation, particularly around dietary supplements, which have led to additional certification costs for manufacturers.

- While Sub-Saharan Africa has seen a decline in per capita milk consumption over the past two decades, the consumption of animal protein rose from 88 g in 2017 to 105.7 g in 2022. Given Africa's projected population growth from 1.3 billion to 2.5 billion by 2050, the demand for animal protein is set to rise.

- South African manufacturers have embraced innovative production techniques to gain market cost leadership. Increasing demand from working women for high-quality protein infant formulas and the nutritional needs of athletes are driving growth rates. With a mature and organized retail sector, shelf space for protein products is expected to increase, maintaining a large share in the African region. As a result, consumers are increasingly buying protein bars and supplements to meet their nutritional needs and maintain their health. Changing consumer lifestyles and rising healthcare expenditures also play a vital role in the growth of the plant protein market in Africa.

Meat and milk production are primary sources of raw materials for manufacturers of animal protein ingredients

- Milk serves as the primary raw material for producing animal proteins like milk proteins, whey proteins, casein, and caseinates. Sudan, Egypt, Kenya, South Africa, and Algeria emerge as the top five milk-producing nations in Africa. West Africa saw a 50% surge in local milk production from 2000 to 2016, reaching approximately 4 billion liters by 2019. The region's growing fitness culture, exemplified by South Africa's 2019 figure of 2.26 million health club members, boosted whey protein production.

- Locally produced milk accounts for 65-70% of consumption, with imported milk powder filling the gap. In 2018, the European Union exported 92,620 tons of milk powder and 276,982 tons of fat-filled milk powder to West Africa. Kenya stands out as East Africa's primary milk producer, with the dairy industry leading the country's agricultural landscape, contributing 4% to its GDP and playing a pivotal role in income generation and employment.

- Based on the records of per capita animal product consumption, the feed required for South Africa was 13.3 million tons in 2021, which is projected to increase further during the forecast period due to the rising demand for insect proteins for animal feed in the region. In Africa, animal proteins like collagen and gelatin are typically sourced from animal and marine waste. Interestingly, pigs stand out by requiring less feed. This not only helps in managing the excess heat generated during digestion and metabolism but also influences their protein content.

Africa Animal Protein Industry Overview

The Africa Animal Protein Market is fragmented, with the top five companies occupying 11.63%. The major players in this market are Fonterra Co-operative Group Limited, Hilmar Cheese Company Inc., Kerry Group plc, Lactoprot Deutschland GmbH and Royal FrieslandCampina N.V (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90221

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 South Africa

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Protein Type

- 4.1.1 Casein and Caseinates

- 4.1.2 Collagen

- 4.1.3 Egg Protein

- 4.1.4 Gelatin

- 4.1.5 Insect Protein

- 4.1.6 Milk Protein

- 4.1.7 Whey Protein

- 4.1.8 Other Animal Protein

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Nigeria

- 4.3.2 South Africa

- 4.3.3 Rest of Africa

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Amesi Group

- 5.4.2 Fonterra Co-operative Group Limited

- 5.4.3 Hilmar Cheese Company Inc.

- 5.4.4 Kerry Group plc

- 5.4.5 Lactoprot Deutschland GmbH

- 5.4.6 Prolactal

- 5.4.7 Royal FrieslandCampina N.V

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.