Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690989

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690989

United Kingdom Animal Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 213 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

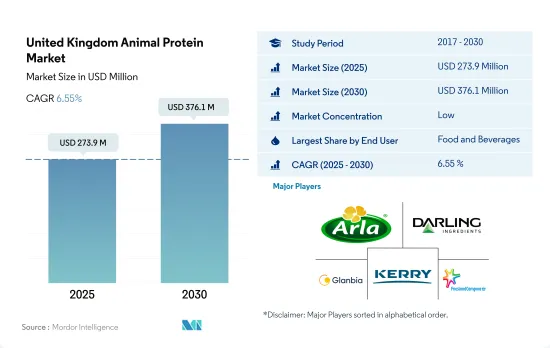

The United Kingdom Animal Protein Market size is estimated at 273.9 million USD in 2025, and is expected to reach 376.1 million USD by 2030, growing at a CAGR of 6.55% during the forecast period (2025-2030).

With manufacturers strategy to innovate products like lactose-free animal proteins, like gelatin, collagen, and insect proteins, has led the food and beverage sector to lead the market

- By application, the food and beverage industry is the leading end-user segment in the UK animal protein market, followed by supplements. The bakery products sub-segment accounts for the major volume in the food and beverage segment, followed by the snacks sub-segment. The food and beverage segment is likely to outpace the growth of other applications in terms of value and record a CAGR of 6.79% during the forecast period (2023-2029). Around 4,000 bakers in the country are continuously innovating and developing products like lactose-free animal proteins, like gelatin, collagen, and insect proteins because the lactose-intolerant population is increasing in the United Kingdom.

- The supplements segment accounts for the second-largest share of the UK animal protein market, led by the sports/performance nutrition industry, which is anticipated to register a CAGR value of 6.67% during the forecast period. Among all animal proteins, insect protein has a price advantage in the market because it costs 40% lesser than other well-known animal proteins, such as milk proteins. The number of sports and fitness enthusiasts increased to around 180,000 in 2021, thereby increasing the demand for supplements.

- The market observed a hike of 0.91% in terms of value on a Y-o-Y basis from 2018 to 2020. Due to the COVID-19 pandemic-related restrictions and work-from-home norms, the market for snacks grew by around USD 2 million from 2019 to 2020. This situation positively impacted the growth of the animal protein market in the United Kingdom. For instance, around 5.6 million people were working from home in 2020 and 2021, which majorly increased the consumption of snacks, beverages, and bakery products.

United Kingdom Animal Protein Market Trends

The consumption growth of animal protein fuels opportunities for key players in the ingredients segment

- Consumers in the United Kingdom are looking for healthier food options due to increasing urbanization, the growing geriatric population, lifestyle changes, and the increasing number of women in the registered workforce. The demand for protein-fortified foods is also growing among consumers in the country to meet their daily dietary requirements. Animal protein has transformed from a low-profile commodity to a value-enhancing ingredient. The per capita consumption of overall animal protein increased from 60.4 g in 2018 to 65.2 g in 2022.

- The highly matured food and beverage industry witnessed a rising demand for high-quality protein ingredients from health-conscious people. There is also a growing popularity of personal care and sports nutrition products in the United Kingdom. These industries are boosting the animal protein market. Animal protein is one of the primary ingredients in products that promote weight management and boost immunity. As of July 2022, around 40% of consumers in the United Kingdom looked for protein while choosing foods and beverages for their exercise schedules. The demand rose by almost 50% among people aged 18-29 years.

- With a significant focus on overall health and clean-label products, the demand for natural ingredients from the sports nutrition segment is growing. The market for whey protein is mostly driven by the rising intention of leading healthy lifestyles. The number of health and fitness clubs increased largely due to this trend, significantly enhancing the market's growth possibilities. The UK whey protein market was also driven by the industry's experience in consumers' demand for high-quality protein ingredients. The number of gyms and fitness centers in the United Kingdom increased from 2,642 in 2017 to 3,060 in 2021.

Rapid development in dairy processing industry to drive milk production

- The animal protein market include the production of distinct raw materials, like meat from cattle, chickens, and pigs with bone, raw milk from cattle, skim milk from cows, and dry whey powder. Consumers are inclined toward consuming home-slaughtered meat, including beef/veal and pig. In 2020, the demand for beef/veal and pig meat increased by 1.92% and 2.81%, respectively, amounting to 932.10 thousand tons and 984.30 thousand tons, respectively. The constant rise in meat production is catering to the country's animal protein sector.

- Milk production is constantly rising in the United Kingdom despite the continuous decline in the number of dairy cows. During 2016-2019, the average daily protein intake of individuals aged 19 to 64 years was 76 g per person, which was more than the 64 g/day average adult daily requirement. This number was calculated using a reference intake value of 0.83 g/kg of body weight per day. The average daily consumption of animal protein per person is projected to be 39.6 g, with 25.9 g coming from meat and meat products and 9.9 g from milk and milk products. Accordingly, the total domestic milk production has risen. Less than 7% of the domestic production is exported, providing easy access to manufacturers.

- The forecast year, 2023, was challenging for the UK pig industry. The contraction in the breeding herd in 2022 led to a significant reduction in the number of finishing pigs in 2023. This, in turn, was expected to result in production volumes falling Y-o-Y as clean pig slaughter fell to its lowest number in a decade. The estimated cost of pig production fell in 2023 and moved net margins into a positive position for the first time in over two years.

United Kingdom Animal Protein Industry Overview

The United Kingdom Animal Protein Market is fragmented, with the top five companies occupying 30.12%. The major players in this market are Arla Foods AmbA, Darling Ingredients Inc., Glanbia PLC, Kerry Group PLC and Koninklijke FrieslandCampina NV (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90155

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 United Kingdom

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Protein Type

- 4.1.1 Casein and Caseinates

- 4.1.2 Collagen

- 4.1.3 Egg Protein

- 4.1.4 Gelatin

- 4.1.5 Insect Protein

- 4.1.6 Milk Protein

- 4.1.7 Whey Protein

- 4.1.8 Other Animal Protein

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Agrial Enterprise

- 5.4.2 Arla Foods AmbA

- 5.4.3 Carbery Food Ingredients Limited

- 5.4.4 Darling Ingredients Inc.

- 5.4.5 Glanbia PLC

- 5.4.6 Insect Technology Group Holdings UK Limited

- 5.4.7 Jellice Pioneer Private Limited

- 5.4.8 Kerry Group PLC

- 5.4.9 Koninklijke FrieslandCampina NV

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.