PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683805

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683805

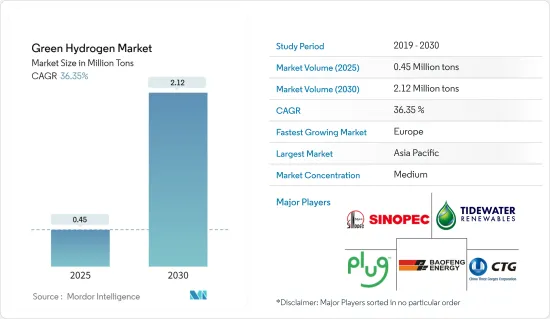

Green Hydrogen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Green Hydrogen Market size is estimated at 0.45 million tons in 2025, and is expected to reach 2.12 million tons by 2030, at a CAGR of 36.35% during the forecast period (2025-2030).

The COVID-19 pandemic moderately impacted the overall growth of the green hydrogen industry, owing to a halt in production and disruption in the supply chain. However, after the pandemic, the demand for green hydrogen increased in the transportation segment, which, in turn, has propelled the industry's growth.

Over the medium term, the demand for green hydrogen in the chemical industry and growing environmental concerns regarding carbon emissions are expected to drive the demand for green hydrogen.

On the flip side, the high investment cost of green hydrogen, limited access to technology and infrastructure, and high energy losses will likely hinder the industry's overall growth.

Favorable policies and regulations promoting the usage of green hydrogen are projected to offer new growth opportunities to the market.

Asia-Pacific is expected to dominate the market, and Europe will likely witness the highest annual growth rate during the forecast period.

Green Hydrogen Market Trends

The Power and Other End-user Industries Segment is Expected to Dominate the Market

- Hydrogen is a very versatile energy carrier that has the potential to play a significant role in decarbonizing the energy system.

- Renewable energy produced via wind or solar farms is stored as compressed gas. The hydrogen energy storage system consists of an electrolyzer to convert electricity to green hydrogen, a storage facility to store hydrogen as a compressed gas, and a fuel cell to convert green hydrogen to electricity.

- Leading economies worldwide are ramping up their hydrogen storage capacities, primarily targeting the power generation sector for decarbonization.

- This push is evident through various initiatives, such as grants and incentives. For example, in 2023, the US government allocated nearly USD 48 million across 16 projects, focusing on advancing clean hydrogen technologies, notably fuel cells and storage.

- Major economies around the globe are foraging into the field of developing innovative solutions to improve the adoption of integrated green hydrogen-based power generation solutions to meet climate goals. In a significant move, in September 2023, India's Ministry of New & Renewable Energy unveiled plans for a pilot project to generate 100 MW of round-the-clock power using green hydrogen storage.

- Moreover, in April 2024, Satluj Jal Vidyut Nigam (SJVN) announced the commissioning of India's first multi-purpose green hydrogen pilot project, a 20 Nm3/hr electrolyzer and 25 kW fuel cell capacity-based green hydrogen pilot project, Nathpa Jhakri Hydro Power Station (NJHPS) in Himachal's Jhakri.

- Similarly, China made strides in July 2023, inaugurating a 12 MW/2 MWh green hydrogen-based energy storage facility in Gannanzhou Cooperation City, Gansu Province.

- Numerous market players are developing innovative solutions to integrate green hydrogen into power generation facilities. For instance, Siemens Energy and Siemens Gamesa target a total investment of around EUR 120 million in the coming five years to develop an offshore wind turbine as a single synchronized system to directly produce green hydrogen, with a full-scale offshore demonstration expected by 2025/2026.

- The rising adoption of green hydrogen, coupled with aggressive decarbonization efforts in the building and power sectors, paints a promising picture for the market under study, projecting robust growth in the coming years.

- Additionally, low-carbon fuels, like green hydrogen (H2), will be a key component of the global energy system, which aims to achieve net zero greenhouse gas (GHG) emissions by 2050.

- According to the report of the International Renewable Energy Agency (IRNA), the number of new power-to-hydrogen projects worldwide has changed yearly. For instance, in 2022, there were five projects, and in 2023, there were only two.

- Therefore, the aforementioned factors are projected to boost the consumption of green hydrogen in the power and other end-user energy industries.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific is expected to dominate the market. China has the largest GDP in the region, and China and India are among the fastest-emerging economies in the world.

- In March 2022, China revealed its first long-term hydrogen plan from 2021 to 2035. This strategic roadmap emphasizes a phased approach, prioritizing the growth of the domestic hydrogen industry through technological advancements and enhanced manufacturing capabilities. Notably, the plan targets producing 100,000 to 200,000 tons of hydrogen annually from renewable sources by 2025, with a broader goal of mainstreaming renewable hydrogen in the economy to bolster China's green energy transition by 2035. Additionally, the plan advocates for a diverse technology pathway, promoting a varied mix of renewable sources over the next 15 years.

- Chinese steelmakers spearhead the shift toward green hydrogen, aiming to replace fossil fuels in processes like Blast Furnace operations. Notably, Baowu, a major player, initiated the construction of a green hydrogen-fueled electric arc furnace in Zhanjiang, Guangdong.

- Industries like steel, cement, and fertilizers, known for their high carbon footprint, face mounting pressure for decarbonization. However, with India's concerted efforts and the ambitious targets set by the National Green Hydrogen Mission, which aims to slash INR 1 lakh crore worth of fossil fuel imports and nearly 50 million metric tons (MMT) of CO2 emissions annually by 2030, green hydrogen emerges as a beacon of hope in their transition.

- Similarly, NTPC Limited took a significant step starting in January 2023, blending up to 8% green hydrogen into the PNG Network at its Kawas Township in Surat, Gujarat, India.

- Tokyo is making strides in developing its green hydrogen facilities on publicly owned land rather than falling behind. The metropolitan government announced intentions to begin constructing three units by the fiscal year 2024, aiming to have one operational by the end of that year. However, further details from the government are eagerly anticipated.

- In January 2024, SK Ecoplant partnered with Bloom Energy for a groundbreaking green hydrogen initiative. Teaming up with Korea Southern Power and local authorities, they aim to introduce hydrogen power on a significant scale. SK Ecoplant will leverage Bloom's cutting-edge solid oxide electrolyzer (SOEC) technology to produce green hydrogen as a transport fuel on Jeju Island, South Korea. The upcoming presentation, scheduled to commence in late 2025, will involve the implementation of 1.8 megawatts of electrolyzer technology.

- Hence, the above-mentioned factors are expected to boost the consumption of green hydrogen in Asia-Pacific.

Green Hydrogen Industry Overview

The global green hydrogen market is partially consolidated. Some of the major players in the market include China Petroleum & Chemical Corporation, Ningxia Baofeng Energy Group Co. LTD, Plug Power Inc., China Three Gorges Corporation (CTG), and Tidewater Renewables Ltd (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Realizing the Potential in the Chemical Industry

- 4.1.2 Growing Environmental Concerns Regarding Carbon Emissions

- 4.2 Market Restraints

- 4.2.1 High Investment Cost of Green Hydrogen

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Technological Snapshot

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 End-user Industry

- 5.1.1 Refining

- 5.1.2 Chemicals

- 5.1.3 Iron and Steel

- 5.1.4 Transportation

- 5.1.5 Power and Other End-user Industries

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Rest of Europe

- 5.2.4 Rest of the World

- 5.2.4.1 South America

- 5.2.4.2 Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Products and Chemicals Inc.

- 6.4.2 Air Liquide

- 6.4.3 BP PLC

- 6.4.4 China Petroleum & Chemical Corporation

- 6.4.5 China Three Gorges Corporation

- 6.4.6 Engie

- 6.4.7 Fortescue Future Industries

- 6.4.8 Green Hydrogen International Corp.

- 6.4.9 Iberdrola SA

- 6.4.10 Intercontinental Energy

- 6.4.11 LHYFE

- 6.4.12 Linde PLC

- 6.4.13 Ningxia Baofeng Energy Group Co. Ltd

- 6.4.14 Plug Power Inc.

- 6.4.15 Reliance Industries Limited

- 6.4.16 Tidewater Renewables Ltd

- 6.4.17 Uniper SE

- 6.4.18 Yara

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Favorable Policies and Regulations Promoting the Usage of Green Hydrogen