PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644495

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644495

Global Office Space - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

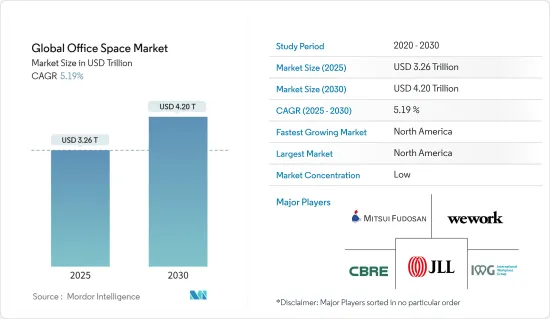

The Global Office Space Market size is estimated at USD 3.26 trillion in 2025, and is expected to reach USD 4.20 trillion by 2030, at a CAGR of 5.19% during the forecast period (2025-2030).

In particular, larger companies still use a classic leasing model for office space on long-term agreements. Nevertheless, the development of flexible workspace solutions, such as coworking spaces and service offices, and the demand for meeting rooms are fueled by the increasing flexibility in working arrangements. The Employment Relations Flexible Working Bill was adopted by Parliament in July 2023 and received royal assent in the United Kingdom.

Coworking spaces, offering shared workspaces with flexible lease terms, have gained popularity among freelancers, start-ups, and even established enterprises. These spaces often provide a collaborative environment, networking opportunities, and amenities, attracting businesses seeking flexibility.

Technology is playing an increasingly significant role in office spaces. Smart office solutions, including IoT devices, occupancy sensors, and integrated communication tools, enhance efficiency, security, and workplace experience. In January 2023, Global IT Corporation and Konica Minolta Inc. announced the establishment of a joint venture, Konica Minolta Solution Labs Inc., to fortify software development capabilities and boost the growth of the office space market. Konica Minolta also targets other peripheral areas of the market, such as smart office solutions and the potential for untapped software solutions.

Global Office Space Market Trends

The Popularity Of Flexible Office Spaces is Increasing

The demand for office spaces increased significantly due to the maturity of the flexible workspace market, particularly in some cities, and the need for pandemic preparedness. The emergence of several start-ups and greater appreciation for existing market players offering flexible workspaces as real estate strategies underpinned this trend. As technology companies seek to set up global capability centers with a flexible model that allows them to control costs successfully in an economically challenging environment, demand for flexible office space will increase. Increased flexibility and shorter lease periods are expected to be requested by occupiers due to the effects of the pandemic and recession. They will be more careful when allocating capital and operational costs. This trend is expected to continue, and enterprise corporate offices may look for fitted-out spaces, shorter leases, or privately operated spaces with an average lock-in period of 36 months or less. According to industry reports, by 2024, the number of flexible workspace desks is expected to increase from 2.54 million to 3.1 million.

However, with increased occupancy levels and demand, vital micro-market operators are looking to improve their prices. The occupancy rate of flex contracts in private offices returned to a pre-pandemic level of more than 80% and more than 65% for shared space. Flex operators charged higher prices for private office desks, as recorded by an average 9% increase in October 2022 in Europe.

Indian Cities Recorded Highest Prime Office Rental Growth in Asia-Pacific

In India, the Mumbai Metropolitan Region recorded the highest office rental, followed by the National Capital Region (NCR) and Bengaluru, in the first half of 2023. The highest rental growth of approximately 16% Y-o-Y was recorded in Mumbai owing to limited availability of space, followed by Delhi-NCR and Pune, which noted a marginal rise of 3% and 2% Y-o-Y, respectively.

Bengaluru and Hyderabad saw a rise in vacancy levels due to a consistent infusion of space outpacing the leasing momentum. The Indian commercial real estate sector was not completely insulated from headwinds of slowing global economic growth, with select organizations reducing headcount and a few cities undergoing a technical recession. There was a visible slowdown in demand in the first quarter, with a 14% decline compared to the previous year, which continued in the second quarter, with demand contracting by 9% Y-o-Y.

With quite a few tech companies encouraging employees to return to the office, leasing activity saw a marked improvement in the city. The IT sector accounted for 46% of the leasing activity in Chennai in H1 2023, demonstrating its continued importance to the city's office market. Following the IT-BPM sector, flexible workspaces were leased aggressively, with a contribution of 21% and nearly 0.9 million sq. ft of leased area. The energy and chemicals sector occupiers were also active, with a substantial 19% share in leasing activity in H1 2023, up from a negligible share in H1 2022.

Global Office Space Industry Overview

The global office space market is highly competitive and consists of several players. Some prominent players in the market include CBRE Group, Mitsui Fudosan, Jones Lang LaSalle Incorporated, IWG PLC, and WeWork. These companies leverage strategic collaborative initiatives to increase their market share and profitability. Vendors depend on successive merger and acquisition strategies, research and development, geographic expansion, and new product introduction strategies to execute further business expansion and growth.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Government Regulations and Initiatives

- 4.3 Technological Trends in the Industry

- 4.4 Insights into Office Rents

- 4.5 Insights into Office Space Planning

- 4.6 Impact of Covid-19 on the Market

- 4.7 Value Chain / Supply Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Flexible Work Arrangements and Coworking Spaces

- 5.2 Market Restraints

- 5.2.1 Remote Work Trends

- 5.3 Market Opportunities

- 5.3.1 Technology Integration and Smart Offices

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Building Type

- 6.1.1 Retrofits

- 6.1.2 New Buildings

- 6.2 By End User

- 6.2.1 IT and Telecommunications

- 6.2.2 Media and Entertainment

- 6.2.3 Retail and Consumer Goods

- 6.2.4 Other End-users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Rest of the Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 India

- 6.3.3.2 China

- 6.3.3.3 Japan

- 6.3.3.4 Rest of the Asia-Pacific

- 6.3.4 Middle East and Africa

- 6.3.4.1 South Africa

- 6.3.4.2 United Arab Emirates

- 6.3.4.3 Saudi Arabia

- 6.3.4.4 Egypt

- 6.3.4.5 Rest of the Middle East and Africa

- 6.3.5 Latin America

- 6.3.5.1 Mexico

- 6.3.5.2 Brazil

- 6.3.5.3 Argentina

- 6.3.5.4 Rest of the Latin America

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 CBRE Group Inc.

- 7.2.2 Mitsui Fudosan Co. Ltd

- 7.2.3 Jones Lang LaSalle Incorporated

- 7.2.4 IWG PLC

- 7.2.5 WeWork

- 7.2.6 Knotel Inc.

- 7.2.7 Servcorp

- 7.2.8 The Office Group

- 7.2.9 WOJO

- 7.2.10 Mindspace*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX