Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636478

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1636478

ASEAN Countries Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 120 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

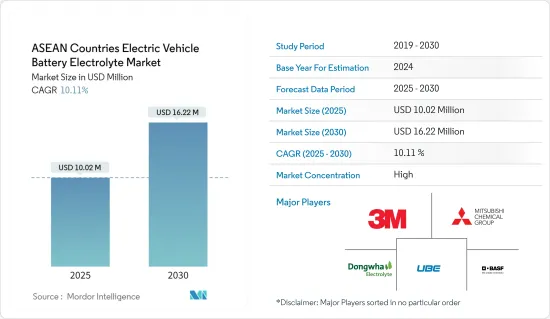

The ASEAN Countries Electric Vehicle Battery Electrolyte Market size is estimated at USD 10.02 million in 2025, and is expected to reach USD 16.22 million by 2030, at a CAGR of 10.11% during the forecast period (2025-2030).

Key Highlights

- In the medium term, the market is poised for growth, fueled by the surging adoption of electric vehicles (EVs) and supportive government initiatives.

- Conversely, disruptions in the supply chain may pose challenges to this growth.

- However, advancements in electrolyte formulations present lucrative opportunities for the market in the near future.

- Within the region, Singapore stands out, anticipating notable growth, thanks to its concerted efforts to bolster the country's EV ecosystem.

ASEAN Countries Electric Vehicle Battery Electrolyte Market Trends

Lithium-Ion Batteries Segment to Dominate the Market

- The lithium-ion battery segment stands as a pivotal component of the electric vehicle (EV) battery electrolyte market in the ASEAN region, propelled by the swift uptake of electric vehicles and innovations in battery technology.

- With regional governments championing greener transportation and a growing consumer preference for EVs, the appetite for efficient, high-performance batteries is on the rise. Electrolytes play a vital role in boosting battery performance, ensuring safety, and extending longevity.

- A key driver behind the lithium-ion battery segment's expansion is the notable drop in battery costs. For example, in 2023, the average price of lithium-ion batteries dipped to approximately USD 139 per kilowatt-hour (kWh), marking a remarkable decline of over 82% since 2013. Forecasts suggest prices might slide below USD 113/kWh by 2025 and could touch USD 80/kWh by 2030.

- This downward trajectory in battery prices not only enhances the affordability of electric vehicles for consumers but also spurs manufacturers to delve into advanced battery technologies and premium electrolytes, amplifying market demand.

- Moreover, sustainability is emerging as a pivotal force in the lithium-ion battery segment. With a surge in environmental consciousness, manufacturers are pivoting towards eco-friendly electrolyte solutions crafted from sustainable materials. This green shift not only resonates with consumer preferences but also dovetails with regulatory mandates aimed at curbing the environmental footprint of battery production.

- In July 2024, LG Energy Solution and Hyundai Motor Corp inaugurated a 10 GWh capacity EV battery manufacturing facility in Indonesia. Furthering its ambition to be a global EV hub, Indonesia, in October 2024, unveiled a joint venture with China's Contemporary Amperex Technology Co Ltd (CATL), committing a substantial USD 1.2 billion towards lithium-ion battery production in the Southeast Asian landscape.

- In conclusion, driven by increasing investments and declining prices, the adoption of lithium-ion technology is set to accelerate in the region, paving the way for substantial market growth in the years ahead.

Singapore Expected to Play a Key Role

- Singapore has been at the forefront of EV charging infrastructure in ASEAN, with more than 1,800 public charging points available. The Government of Singapore plans to install 60,000 more charging points by the end of 2030.

- From 2021 to 2025, the Singapore government has earmarked USD 22 million to boost EV adoption. This initiative aims to bolster the number of chargers on private properties, enhancing the overall charging infrastructure. Concurrently, Singapore has positioned itself as a pivotal R&D hub for the EV sector, attracting investments from multinationals and startups alike, thereby nurturing a robust local EV ecosystem.

- With a commitment to curbing pollution, the Singapore government is championing electric mobility. This push is anticipated to drive up EV sales. Notably, Singapore aims to transition from internal combustion engines to cleaner-energy vehicles by 2040. Leading this charge is the newly established National Electric Vehicle Centre (NEVC), steering efforts towards Singapore's 2040 green energy vehicle goal. This shift is poised to elevate the demand for battery materials, particularly electrolytes, in the near future.

- As reported by the Land Transport Authority, EV sales in Singapore are on the rise. Between January-July 2024, the country registered 6,019 battery electric vehicles. This marks a significant jump from 1,892 registrations during the same period in 2023, representing an 32.4% increase.

- The swift growth of the EV market not only benefits the environment-due to zero emissions improving air quality and curbing greenhouse gases-but also plays a vital role in the global fight against climate change.

- Given the alignment of consumer preferences and regulatory support, the demand for electric vehicle battery electrolytes in Singapore is set to rise in the foreseeable future.

ASEAN Countries Electric Vehicle Battery Electrolyte Industry Overview

The ASEAN Countries' electric vehicle battery electrolyte market is semi-consolidated. Some of the major players include (not in particular order) Mitsubishi Chemical Group, 3M, Dongwha Eletrolyte, BASF SE, and UBE Corp. among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50003746

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Electric Vehicle (EV) Adoption

- 4.5.1.2 Supportive Government Initiatives

- 4.5.2 Restraints

- 4.5.2.1 Supply Chain Disruptions

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Force Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-Ion Batteries

- 5.1.2 Lead-Acid Batteries

- 5.1.3 Others

- 5.2 Electrolyte Type

- 5.2.1 Liquid Electrolyte

- 5.2.2 Gel Electrolyte

- 5.2.3 Solid Electrolyte

- 5.3 Geography

- 5.3.1 Malaysia

- 5.3.2 Thailand

- 5.3.3 Indonesia

- 5.3.4 Singapore

- 5.3.5 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Mitsubishi Chemical Group

- 6.3.2 3M

- 6.3.3 Dongwha Eletrolyte

- 6.3.4 UBE Corp.

- 6.3.5 BASF SE

- 6.3.6 Hitachi, Ltd.

- 6.3.7 Cabot Corporation

- 6.3.8 Umicore N.V

- 6.4 Market Ranking/Share Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovations in Electrolyte Formulations

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.