Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1624594

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1624594

Latin America Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 100 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

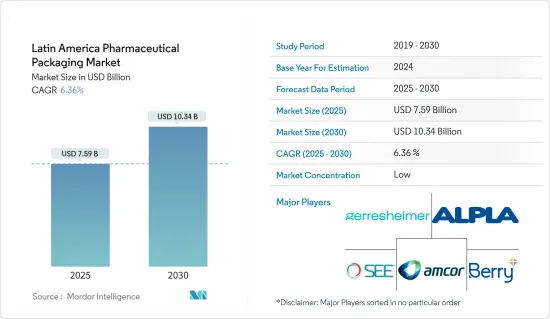

The Latin America Pharmaceutical Packaging Market size is estimated at USD 7.59 billion in 2025, and is expected to reach USD 10.34 billion by 2030, at a CAGR of 6.36% during the forecast period (2025-2030).

Key Highlights

- Pharmaceutical packaging is crucial in drug product presentation, protection, identification, and containment throughout their lifecycle. It facilitates storage, transport, and display while ensuring compliance with regulatory standards until the product is consumed. Adequate packaging shields the drug from various environmental factors, including climatic, biological, physical, and chemical conditions. To be optimal, pharmaceutical packaging must be cost-effective and provide adequate stability throughout the product's shelf life. The selection of packaging materials and types is based on the specific nature of the drug, ensuring that the chosen packaging offers appropriate protection and clear identification and maintains the integrity of the enclosed pharmaceutical product.

- The pharmaceutical packaging industry in Latin America is experiencing increased demand driven by the region's expanding economies and urbanising population. The growing elderly demographic requiring continuous medical care further fuels this trend. As the pharmaceutical manufacturing sector gains momentum, packaging vendors in the region can capitalise on the market's significant potential. Foreign investments, rising local production, and new product development contribute to the growth of the regional packaging industry. Consequently, Latin America is expected to remain a key market for pharmaceutical packaging shortly.

- The pharmaceutical industry in Latin America stands as one of the region's largest and most capital-intensive sectors. Research and development (R&D) plays a crucial role in developing innovative drugs, contributing to increased life expectancy in Latin America over the past two decades, albeit at a high cost. This focus on R&D has led to significant advancements in medical treatments and therapies, addressing various health challenges specific to the region.

- Traditionally, large multinational companies from Western Europe and the United States have dominated the pharmaceutical market in Latin America. These established firms have leveraged their extensive resources, global research networks, and advanced manufacturing capabilities to maintain a strong regional presence. However, in recent years, the landscape has begun to shift with the entry of new players into the industry.

- These new entrants include multinational companies from China, India, and South Korea, bringing different drug development and manufacturing approaches. Additionally, local firms from several developing countries within Latin America have emerged, often focusing on generic drugs or niche therapeutic areas. This diversification of market participants has led to increased competition, potentially driving innovation and improving access to medicines for Latin American populations.The evolving pharmaceutical landscape in Latin America presents opportunities and challenges for established and emerging companies. As the market continues to develop, factors such as regulatory environments, intellectual property rights, and healthcare policies will significantly shape the industry's future in the region.

- ALIFAR, the Latin American Association of Pharmaceutical Industries, is a non-profit international organisation operating independently from governmental and intergovernmental bodies. It represents nationally owned pharmaceutical companies across Latin America. ALIFAR's membership encompasses over 400 companies from 12 Latin American countries, accounting for over 90% of the region's pharmaceutical market. The organization plays a crucial role in advocating for the interests of its member companies and promoting the development of the pharmaceutical industry in Latin America. ALIFAR works to foster collaboration among its members, share best practices, and address common challenges faced by the industry in the region.

- The growing demand for pharmaceutical drugs and medicines in Latin America has been driven by population growth, increasing life expectancy, and a rising prevalence of chronic diseases. This demand and technological advancements in the pharmaceutical industry have directly led to an increased need for packaging solutions such as bottles, ampules, and other containers. The pharmaceutical packaging market in Latin America has consequently experienced significant growth. Manufacturers of packaging materials and solutions have had to adapt to meet the industry's evolving requirements, including considerations for drug stability, safety, and compliance with regulatory standards.

- Environmental concerns related to pharmaceutical packaging raw materials may limit the market but also provide opportunities for innovation in packaging within the pharmaceutical industry in the region. The increasing focus on sustainability has heightened scrutiny of traditional packaging materials, prompting manufacturers to explore eco-friendly alternatives. This shift presents cost and regulatory compliance challenges but also opens avenues for developing novel, environmentally responsible packaging solutions.

- Companies are investing in research and development to create biodegradable materials, reduce plastic usage, and improve the recyclability of pharmaceutical packaging. These efforts address environmental concerns and align with changing consumer preferences and regulatory requirements. As a result, the industry is witnessing a surge in innovative packaging designs that maintain product integrity while minimising environmental impact, potentially creating new market segments and competitive advantages for forward-thinking companies.

Latin America Pharmaceutical Packaging Market Trends

Plastic Bottles to Hold Significant Market Share

- Plastic is widely used in pharmaceutical packaging due to its versatility, durability, flexibility, and sustainability. Pharmaceutical packaging employs plastic bottles made from various materials, including polyvinyl chloride, polyethene, polypropylene, and polystyrene. The industry utilises transparent, durable, lightweight plastic for storage and distribution. These plastic materials offer several advantages, such as resistance to breakage, ease of moulding into various shapes and sizes, and compatibility with a wide range of pharmaceutical products.

- Additionally, plastic packaging helps protect medications from moisture, light, and contaminants, ensuring product integrity and extending shelf life. The use of plastic in pharmaceutical packaging also contributes to cost-effectiveness in manufacturing and transportation, as it is generally lighter and more economical than alternative materials like glass or metal.

- Plastic bottles are extensively utilised for packaging various liquid and solid medicines, including syrups, capsules, tablets, and ophthalmic preparations. The pharmaceutical industry favours plastic packaging due to its strength, lightweight nature, and flexibility, allowing for diverse forms and sizes. The market for pharmaceutical plastic bottles has expanded, driven by technological advancements and the increased adoption of plastic containers for oral solid and liquid medications.

- Plastics in pharmaceutical applications must be non-toxic, non-carcinogenic, biocompatible, and harmless to the biological environment. These stringent requirements ensure the safety and efficacy of pharmaceutical products. The drug development process includes rigorous testing of PET packaging for leaching and extractability in conjunction with the drug. This testing is crucial to prevent contamination or interaction between the packaging and the pharmaceutical contents. PET bottles provide an effective oil barrier, helping to resist chemical spills during transport. This barrier property is significant for maintaining the integrity of liquid medications and preventing contamination from external sources. Additionally, PET packaging offers durability and resistance to breakage, essential qualities for pharmaceutical containers that may be subject to various handling and transportation conditions.

- The demand for pharmaceutical plastic bottles has increased, impacting the market valuation of plastic bottles in Latin America. In 2023, the combined value of pharmaceutical exports from Latin America and the Caribbean reached approximately USD 9.3 billion, marking the region's highest level of pharmaceutical exports during the analyzed period. In 2022, Mexico led Latin American countries in pharmaceutical export value.Further, it is anticipated that the growth of solid containers may be aided due to the increased adoption of medicines containing nutrients. The increasing awareness of nutritional enrichment among working professionals for maintaining balanced nutrition in the human body is anticipated to promote the consumption of dietary supplements and drive demand for plastic bottles in the region.

- Individuals with eye conditions commonly use dropper bottles. These specialised containers allow for the precise administration of eye medications and solutions. Companies like Gerresheimer provide pharmaceutical plastic packaging for various applications, including solid, liquid, and ophthalmic products. Their product range includes PET bottles for liquid dosage forms and ophthalmic solutions. These bottles are engineered to meet specific requirements for preserving and dispensing eye medications, ensuring proper dosage and maintaining product integrity. The use of dropper bottles in ophthalmic applications has become increasingly important as the prevalence of eye-related disorders continues to rise in the region.

Mwxico is Expected to Witness Significant Growth

- Mexico is a significant contributor to the pharmaceutical market share in Latin America. As a mature market in the region's pharmaceutical industry, Mexico has experienced numerous product innovations, particularly in pharmaceutical packaging. This innovation is driven by the presence of significant vendors throughout the country. The Mexican pharmaceutical market has grown steadily, supported by a robust healthcare system and increasing demand for generic and branded medications.

- The country's strategic location and trade agreements, such as NAFTA (now USMCA), have further enhanced its position as a critical player in the regional pharmaceutical landscape. In recent years, Mexico has seen a rise in pharmaceutical research and development activities, with domestic and international companies investing in local facilities. This has increased the production of high-quality, cost-effective medications, further solidifying Mexico's position in the Latin American pharmaceutical market.

- The packaging sector within Mexico's pharmaceutical industry has been particularly dynamic. Innovations in this area have focused on improving drug safety, extending shelf life, and enhancing patient compliance. These advancements include intelligent packaging solutions, eco-friendly materials, and designs catering to different patient groups' needs. Despite challenges such as regulatory complexities and competition from other emerging markets, Mexico's pharmaceutical industry continues to evolve and adapt. The country's commitment to innovation and established manufacturing capabilities position it well for continued growth and influence in the Latin American pharmaceutical market.

- The Mexican healthcare industry is primarily price-driven, with domestically produced goods having a pricing advantage in government sales. Businesses must comply with all sanitary registration standards to ensure quality. Foreign companies should consider cost-cutting measures and highlight the benefits of new technology in their marketing and promotional materials. In 2023, Mexico's pharmaceutical product sales reached approximately USD 10.83 billion, an increase from USD 10.12 billion in 2022. The region's expanding pharmaceutical production, increased availability of over-the-counter medicines, and significant investments by local businesses contribute to the substantial growth of the Brazilian pharmaceutical sector. These trends are expected to lead to an increase in pharmaceutical packaging demand nationwide, along with growing exports.

- The increasing cost of healthcare and the growing preference among end-users such as hospitals and pharmaceutical manufacturers are expected to drive product usage in Mexico during the forecast period. Vials, like other glass containers, are easily recyclable and considered environmentally friendly. The medical and healthcare sectors in the country are experiencing a lucrative demand for these products due to end-users' shift from conventional containers to vials.

Latin America Pharmaceutical Packaging Industry Overview

The pharmaceutical packaging market in Latin America is fragmented, as established companies focus on innovation and acquisition. Companies like Amcor Group GmbH, Berry Global Inc., Schott AG. invest a lot of their resources and money in Research and development to innovate new products, meet with the environment, and ensure government compliance.

- May 2024 - Gerresheimer, a Germany-based company specialising in pharmaceutical and healthcare packaging, is set to expand its facility in Queretaro, Mexico. This expansion aims to boost production capacities for ready-to-fill (RTF) syringes, addressing the North American market's demand for premium syringes. These prefillable glass syringes are designed for injectable biopharmaceuticals, including glucagon-like peptide-1 drugs for obesity management. The expansion started with a ground-breaking ceremony in November 2023, and Gerresheimer is channelling an investment of around EUR 100 million (USD 106 million) into the project.

- November 2023 - Amcor has introduced a mono-PE laminate to create all-film medical packaging recyclable in the polyethylene stream. This innovation reportedly reduces the package's carbon footprint while ensuring patient safety. The film is expected to enable recycle-ready lidding for 3D thermoformed packages, which house items like drapes, protective materials, catheters, and injection and tubing systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 46776

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Domestic Pharmaceuticals Production

- 5.1.2 Growing FDI In regional pharmaceutical and packaging sector

- 5.2 Market Restraints

- 5.2.1 Environmental Concerns related to Pharmaceutical Packaging Raw Materials

- 5.2.2 Fluctuations In Raw Material Prices

6 MARKET SEGMENTATION

- 6.1 By Packaging Material

- 6.1.1 Plastic

- 6.1.2 Glass

- 6.1.3 Metal

- 6.1.4 Paper

- 6.2 By Product Type

- 6.2.1 Blister Packs

- 6.2.2 Plastic Bottles

- 6.2.3 Prefillable Syringes

- 6.2.4 Vials and Ampuls

- 6.2.5 Closures

- 6.2.6 Containers

- 6.2.7 Other Product Types

- 6.3 By Country

- 6.3.1 Brazil

- 6.3.2 Mexico

- 6.3.3 Columbia

- 6.3.4 Argentina

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Sealed Air Corporation

- 7.1.3 Berry Global Inc.

- 7.1.4 Schott AG

- 7.1.5 Gerresheimer AG

- 7.1.6 Aptar Group Inc.

- 7.1.7 ALPLA Werke Alwin Lehner GmbH & Co KG

- 7.1.8 Pretium Packaging

- 7.1.9 Silgan Holdings Inc.

- 7.1.10 Greiner Packaging International GmbH

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.