Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550224

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1550224

France Plastic Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

PUBLISHED:

PAGES: 112 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

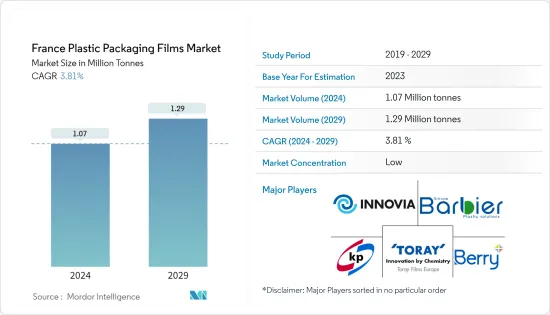

The France Plastic Packaging Films Market size is estimated at 1.07 Million tonnes in 2024, and is expected to reach 1.29 Million tonnes by 2029, growing at a CAGR of 3.81% during the forecast period (2024-2029).

Key Highlights

- The French packaging industry is experiencing robust growth, propelled by a buoyant economy empowering consumers to gravitate toward premium products, often presented in innovative and distinctive packaging. Additionally, the surge in demand for compact, on-the-go packaging, especially prevalent in pouch formats, is fueled by the country's busy professionals juggling hectic lifestyles. This heightened demand for pouch packaging is not limited to a single sector; industries like food, FMCG, groceries, and cosmetics are poised to ramp up their adoption of this packaging style significantly. Consequently, solution providers are ramping up their innovation efforts to bolster their market presence by offering more enticing products.

- The urban lifestyle in France is fueling a surge in demand for convenient packaging. Consumers seek lightweight, user-friendly options, prompting vendors to pivot their designs to stay ahead in the expanding organized retail landscape. Embracing lighter materials, like flexible pouches, meets these evolving demands and offers substantial energy-saving advantages. Additionally, the shift toward sustainable packaging solutions aligns with the increasing consumer awareness and preference for environmentally friendly products. This trend is expected to drive further innovation and competition among packaging vendors.

- Consumer preferences for practicality, portability, sustainability, and enhanced user experiences fuel the rising demand for plastic film in the flexible packaging market. As these trends evolve, the plastic film packaging industry is poised to innovate, catering to the increasingly diverse needs of today's consumers and businesses. This innovation is expected to include advancements in materials, production processes, and design to ensure that plastic film packaging remains a competitive and environment-friendly option in the market.

- Further, consumers are gravitating toward products with extended shelf lives, driven by convenience and a growing concern for reducing food waste. With its superior barrier properties, plastic film packaging shields items from moisture, oxygen, light, and other elements that can compromise their quality and freshness. As a result, it is pivotal in prolonging the shelf life of perishable items, spanning from food and beverages to pharmaceuticals and personal care. France continues to grapple with the prevalent use of single-use plastics, notably in the retail of fresh produce. To curb this, a new law prohibits plastic film and netting.

- This legislation aims to reduce plastic waste and significantly promote sustainable packaging alternatives. Consequently, this legislation is poised to constrict the market for plastic packaging films in the country, impacting manufacturers and suppliers who rely on this market segment. The law is part of a broader initiative to transition toward a circular economy, encouraging the use of biodegradable and reusable materials. This shift is expected to drive innovation in the packaging industry as companies seek to develop eco-friendly solutions that comply with the new regulations.

- In this scenario, manufacturers operating in the country ramp up R&D investments and expand their facilities to innovate and introduce new products. Notably, in March 2024, Berry Global Group Inc.'s Flexibles division, a key player in a pan-European effort, enhanced recycling capabilities in three of its European facilities. This move is part of a larger strategy to boost production of its Sustane line of recycled polymers. The company aims to meet the rising demand for premium films made from recycled materials, leveraging its vast global network for recycled plastics.

France Plastic Packaging Films Market Trends

Polyethylene Segment to Hold Significant Market Share

- Polyethylene, known for its flexibility, high moisture barrier, and durability, also boasts exceptional performance in low temperatures. It distinguishes itself by sealing effectively, even without added coatings. Whether utilized independently or in conjunction with other materials, polyethylene creates a formidable barrier. Furthermore, its eco-friendly attributes garner attention from packaging film manufacturers, underscoring the industry's growing focus on sustainability. The material's versatility extends to various applications, including food packaging, agricultural films, and industrial wrappings, making it a preferred choice across multiple sectors. Its ability to be recycled and its contribution to reducing plastic waste further enhance its appeal in the market.

- Polyethylene (PE) dominates the plastic landscape in the region due to its versatile physical properties. Its popularity stems from its cost-effective production, a distinguishing feature from its plastic counterparts. Notably, PE boasts the lowest softening point among primary packaging plastics, reducing energy consumption. Alongside PE, LDPE and LLDPE are prominent in the flexible packaging sector. Widely used in crafting plastic bags, films, and geomembranes, polyethylene's appeal lies in its lightweight, partially crystalline structure and standout features like chemical resistance, low moisture absorption, and sound insulation.

- Reduced polyethylene prices in Europe are creating a lucrative growth avenue for polyethylene barrier film manufacturers in France. With these price drops, manufacturers can bolster their margins, leading to a potential revenue surge. The savings from cheaper raw materials can be channeled back into R&D, elevating product quality and innovation. Armed with this pricing edge, manufacturers stand poised to retain and expand their market share by enticing customers with more competitive pricing.

- Product visibility plays a pivotal role in shaping consumer choices. Transparent packaging, particularly in the form of polythene films, is witnessing heightened demand across diverse industries. This surge is fueled by consumers' preference for visually assessing products before buying, a factor that not only fosters trust but also boosts sales. Consequently, producers of polyethylene barrier films are now placing a premium on transparency to bolster their market presence.

- In the food and beverage sector, the importance of transparent packaging, which showcases product quality and freshness, is unmistakable. France has witnessed a notable uptick in packaging activities, a surge further fueled by the country's escalating e-commerce endeavors. E-commerce sales revenue in France climbed from USD 121.4 billion in 2020 to USD 173 billion in 2023. This uptick was primarily driven by the growing preference for transparent packaging solutions across sectors like food and beverage, pharmaceuticals, and consumer goods, especially for e-commerce deliveries. Transparent packaging enhances the visual appeal of products and builds consumer trust by allowing them to see the product before making a purchase. Additionally, the rise in online shopping has necessitated using durable and visually appealing packaging to ensure product safety and customer satisfaction during transit.

Food Segment Expected to Hold Significant Share in the Market

- The country's growing appetite for food is a crucial catalyst propelling the demand for specialized plastic films catering to various food items. This surge is primarily driven by the quest for packaging that provides food safety, prolongs shelf life, and elevates product aesthetics. With consumers increasingly prioritizing health and convenience, the plastic film market in food packaging is witnessing a notable upswing, presenting avenues for innovation and expansion. Additionally, advancements in material science and manufacturing technologies enable the development of more sustainable and efficient plastic films, further driving market growth. The increasing adoption of e-commerce for grocery shopping also contributes to the rising demand for robust and reliable packaging solutions.

- Moreover, the rising sales of consumer goods in French supermarkets and hypermarkets are poised to bolster market demand. Key drivers, such as the surging need for plastic films in food and the growing necessity for protecting frozen food and vegetables, are set to propel the demand for plastic films in the coming years. Additionally, the increasing appetite for eco-friendly and lightweight plastic films offers a promising avenue for market growth.

- From April 2023 to March 2024, sales of non-dairy fresh food in French supermarkets and hypermarkets reached approximately USD 16,557 million. Dairy beverages closely followed this at USD 25,574 million, sugary foods at USD 23,802 million, and frozen foods at USD 6,868.9 million. The total sales for the period accounted for USD 146,251.9 million. This increasing demand for various food and non-food products in supermarkets and hypermarkets is paving the way for the plastic film market to align with consumer preferences for convenience, quality, sustainability, and brand appeal.

- The French plastic film market is poised for steady growth during the forecast period, driven by the expanding food and beverage industries, rising consumer spending, and the surge in the e-commerce sector. The increasing demand for packaged food and beverages and the convenience offered by online shopping significantly contribute to this market's expansion. Additionally, advancements in plastic film technology and sustainable packaging solutions are expected to propel market growth further.

France Plastic Packaging Films Industry Overview

The French plastic packaging films market is fragmented, with several global and regional players, such as Innovia Films (CCL Industries Inc.), Berry Global Inc., Klockner Pentaplast, and Cosmo Films, vying for attention in a contested market space characterized by low product differentiation, growing product penetration, and high competition.

- June 2024: Trioworld Group inked a deal to purchase all shares of Sopal SAS, effectively acquiring the French firms Palamy SAS (Palamy) and Beaudet et Rene Jean Emballage SAS (BRJ). These companies are key players in the French market, specializing in high-performance packaging solutions for bread, frozen food, and various consumer packaging needs.

- January 2024: Berry Global unveiled an enhanced iteration of its Omni Xtra polyethylene cling film, positioning it as a certified recyclable substitute for conventional PVC options. Initially tailored for fruits, vegetables, meats, poultry, and deli items, the new Omni Xtra+ film boasts heightened impact resistance, enhanced elasticity, and a more consistent stretching profile.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 50002804

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Defintion

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Driver

- 5.1.1 Growing Demand for Lightweight Packaging Solution

- 5.1.2 Increasing Demand for Plastic Films Across Various Industries Indicates Growth Potential

- 5.2 Market Challenges

- 5.2.1 Stringent Government Laws and Regulation Toward Plastic

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Polypropylene(PP) (Biaxially Oriented Polypropylene (BOPP),Cast polypropylene (CPP))

- 6.1.2 Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE))

- 6.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

- 6.1.4 Polystyrene

- 6.1.5 Bio-Based

- 6.1.6 PVC, EVOH, PETG, and Other Film Types

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.1.1 Candy and Confectionery

- 6.2.1.2 Frozen Foods

- 6.2.1.3 Fresh Produce

- 6.2.1.4 Dairy Products

- 6.2.1.5 Dry Foods

- 6.2.1.6 Meat, Poultry, andnd Seafood

- 6.2.1.7 Pet Food

- 6.2.1.8 Other Food Products (Seasonings and Spices, Spreadables, Sauces, Condiments, etc.)

- 6.2.2 Healthcare

- 6.2.3 Personal Care and Home Care

- 6.2.4 Industrial Packaging

- 6.2.5 Other End-user Industries (Agricultural, Chemical, Etc.)

- 6.2.1 Food

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 TORAY FILMS EUROPE

- 7.1.2 Innovia Films (CCL Industries Inc.)

- 7.1.3 Berry Global Inc.

- 7.1.4 Klockner Pentaplast

- 7.1.5 SUDPACK Holding GmbH

- 7.1.6 DUO PLAST AG

- 7.1.7 SRF LIMITED

- 7.1.8 Groupe Barbier

- 7.1.9 Surfilm Packaging

- 7.1.10 Trioworld Industrier AB

- 7.1.11 AEP GROUP

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.