PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1537725

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1537725

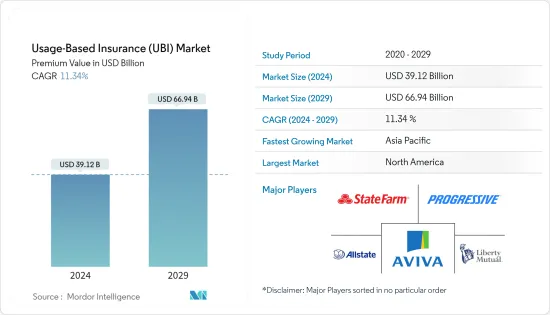

Usage-Based Insurance (UBI) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Usage-Based Insurance Market size in terms of premium value is expected to grow from USD 39.12 billion in 2024 to USD 66.94 billion by 2029, at a CAGR of 11.34% during the forecast period (2024-2029).

The usage-based insurance (UBI) market has witnessed steady growth globally, driven by advancements in telematics technology, increased customer demand for personalized insurance, and the potential for cost savings. Telematics technology plays a crucial role in UBI programs. It involves using devices installed in vehicles or mobile apps that collect driving behavior data, including mileage, speed, acceleration, braking, and location. UBI presents several benefits for insurance companies, including improved risk assessment, better pricing accuracy, reduced claims costs, and enhanced customer engagement. Insurers can leverage UBI data to develop more tailored insurance products and services. UBI programs offer benefits to policyholders as well. Safe drivers with responsible driving habits can receive discounted premiums or other incentives. UBI also allows customers to monitor their driving behavior and make improvements to enhance safety.

Usage-Based Insurance (UBI) Market Trends

Rise in Smartphone Penetration is Fuelling the Market

Mobile telecommunication technology is the latest tool in telematics, with smartphones working as stand-alone devices or linked to vehicle systems to transmit various information to and from the car. Smartphones are an ideal telematics solution as they are typically equipped with multiple relevant sensors, such as GPS, accelerometers, and gyroscopes. They also have extensive data storage capacity, or infinite with the cloud, and superior communication capabilities. There are no device, installation, or data connectivity costs to the insurers with smartphone-based UBI programs. Smartphone computing power allows a big part of the data processing on the device, helping to lower data handling and storage costs. The extensive manufacturing volumes for smartphones exploiting economies of scale make the price-performance metric of the technical capabilities of the smartphone superior to many rivals, and it is still continuously improving over time.

Increasing Usage-based Car Insurance Accelerates in North America

The insurance industry is rapidly shifting from standard auto insurance to premium auto insurance plans driven by telematics data. Usage-based insurance, or UBI, has been gaining support in the US and has recently become increasingly difficult to ignore. About 20 million of the 875 million motor insurance plans in force last year were usage-based, according to Ptolemus, a mobility-focused research and strategic consulting organization with headquarters in Brussels. The auto insurance industry, too, has undergone a transformative shift in the United States with the advent of Usage-Based Insurance (UBI). This innovative approach to underwriting auto policies leverages telematics technology to collect real-time data on individual driving behaviors, allowing insurers to tailor premiums more accurately and reward safe driving habits.

Usage-Based Insurance (UBI) Industry Overview

The Usage-based insurance market is fragmented, with many players. Some of the major players in the global market include Progressive Corporation, Allstate Corporation, Statefarm Insurance, Liberty Mutual Insurance, and Aviva PLC, among others. In the study period, market players were also involved in mergers and acquisitions, and partnerships focused on expanding their presence in the market. The market presents opportunities for growth during the forecast period, which is expected to drive the market competition further. However, with technological advancement and product innovation, mid-size to smaller companies are increasing their market presence by securing new contracts and tapping new markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of Telematics and Connected Cars

- 4.3 Market Restraints

- 4.3.1 Privacy and Data Security is Restraining the Market

- 4.4 Market Opportunities

- 4.4.1 The Insurance Companies to Offer Personalized Premiums Based on Individual Driving Behavior

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Insights on Technological Innovations in the Market

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Package

- 5.1.1 Pay-How-You-Drive

- 5.1.2 Pay-As-You-Drive

- 5.2 By Technology

- 5.2.1 OBD-II

- 5.2.2 Smartphone

- 5.2.3 Black Box

- 5.2.4 Embedded Telematics

- 5.3 By Vehicle Type

- 5.3.1 Passenger Vehicle

- 5.3.2 Commercial Vehicle

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Rest of Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Company Profiles

- 6.2.1 Progressive Corporation

- 6.2.2 Allstate Corporation

- 6.2.3 State Farm Insurance

- 6.2.4 Liberty Mutual Insurance

- 6.2.5 Aviva PLC

- 6.2.6 Generali Group

- 6.2.7 AXA Group

- 6.2.8 Desjardins Insurance

- 6.2.9 MAPFRE SA

- 6.2.10 Zurich Insurance*

7 MARKET FUTURE TRENDS

8 DISCLAIMER AND ABOUT US