PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1639462

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1639462

Philippines Retail Sector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

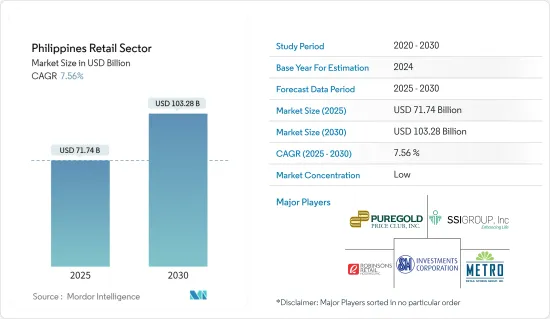

The Philippines Retail Market size is estimated at USD 71.74 billion in 2025, and is expected to reach USD 103.28 billion by 2030, at a CAGR of 7.56% during the forecast period (2025-2030).

The demand for convenience food products is a key driver behind the robust growth of the retail market in the Philippines. These products, requiring minimal preparation, have become popular choices, especially among busy individuals and the rising working female population, who are opting for convenience foods like processed meats and poultry over home-cooked meals.

The retail landscape in the Philippines is witnessing a notable upswing, with industry players capitalizing on the buoyant growth rates across diverse retail segments. Luxury goods, in particular, are poised to be the frontrunners in Southeast Asia, with an estimated growth rate of 30%. Additionally, the retail e-commerce sector in the Philippines is set to outpace its counterparts in Southeast Asia. This retail surge is largely attributed to the expanding supply and distribution networks, facilitating enhanced accessibility to various goods and services for consumers.

Philippines Retail Market Trends

The Philippines' Food and Beverage Sector: A Key Pillar of the Nation's Economy

The food and beverage sector in the Philippines is a vital driver of the nation's economy, accounting for nearly half of its GDP. Within the country's manufacturing landscape, this sector alone contributes to about 25% of the GDP. The Philippines stands out as one of Asia's major food producers. This growth is propelled by the rising disposable incomes of the middle and upper classes. Notably, the 25-34 age group remains a dominant force in discretionary spending, a trend expected to persist for the coming decade. The US Department of Agriculture projects a 6% rise in the industry's revenue, reaching USD 35 billion this year, primarily attributed to an improved labor scenario.

With the proliferation of restaurants, fast food chains, and food delivery apps like Grubhub and Caviar, the demand for food and beverages in the Philippines is poised for significant growth. Moreover, consumers are increasingly recognizing the health benefits of organic, natural, and fresh foods, further fueling this demand.

The Online Distribution Channel is Emerging in the Market

Benefiting from robust internet and smartphone penetration rates, the Philippines stands out as one of Southeast Asia's most rapidly expanding e-commerce markets. The COVID-19 pandemic further catalyzed a pronounced shift in consumer behavior, with a notable preference for online platforms over brick-and-mortar stores. In the Philippines, key players in the online marketplace landscape include Lazada, Shopee, Zalora, Ebay, and Kimstore. Notably, Lazada, backed by Chinese e-commerce titan Alibaba, has been extending its footprint to ASEAN markets via its China-based platform, Taobao. Concurrently, the nation has been witnessing a surge in online grocery shopping, with notable collaborations like Foodpanda's partnership with 7-Eleven stores. As the e-commerce landscape expands, so does the adoption of digital payment services. While a significant portion of shoppers have reverted to in-store purchases, the e-commerce segment for food and beverages, albeit small, showcases a promising potential for product imports.

Philippines Retail Industry Overview

The retail industry in the Philippines is fragmented. There are only a few big players in the retail market. However, the sector itself is experiencing rapid growth, driven by the expansion of existing players and the emergence of new business opportunities. Notably, the retail landscape is shifting, with smaller, unstructured stores making way for larger formats like supermarkets, hypermarkets, and retail chains. This transformation is projected to continue gaining momentum in the coming years. Leading the pack are prominent players such as SM Investments Corp., SSI Group, Puregold Price Club Inc., Metro Retail Stores Group Inc., and Robinsons Retail Holdings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 The Rising Demand for Packaged and Ready to Eat Food is Driving the Market

- 4.2.2 Increase in the Demand for Branded Goods Categories such as Apparel, Cosmetics, Footwear, Watches, Beverages, and Food

- 4.3 Market Restraints/Challenges

- 4.3.1 Changing Consumer Buying Behavior and Rising Brand Consciousness

- 4.4 Market Opportunities

- 4.4.1 Increase in Internet Penetration Leads to Growth in the Market

- 4.4.2 Virtual Sales Assistants and Rising Digital Payment Options

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.7 Consumer Behavior Analysis

- 4.8 Insights into Technological Innovations in the Retail Industry

- 4.9 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Products

- 5.1.1 Food and Beverage

- 5.1.2 Personal and Household Care

- 5.1.3 Apparel

- 5.1.4 Footwear and Accessories

- 5.1.5 Furniture

- 5.1.6 Toys and Hobbies

- 5.1.7 Electronic and Household Appliances

- 5.1.8 Other Products

- 5.2 By Distribution Channel

- 5.2.1 Supermarkets/Hypermarkets

- 5.2.2 Convenience Stores

- 5.2.3 Department Stores

- 5.2.4 Specialty Stores

- 5.2.5 Online

- 5.2.6 Other Distribution Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 SM Investments Corp. (SM Retail Inc.)

- 6.2.2 Puregold Price Club Inc.

- 6.2.3 SSI Group Philippines

- 6.2.4 Metro Retail Sores Group Inc.

- 6.2.5 Robinsons Retail Holdings Inc.

- 6.2.6 Rustan Supercenters Inc.

- 6.2.7 Alfamart

- 6.2.8 7-Eleven

- 6.2.9 Golden ABC Inc.

- 6.2.10 Mercury Drug Corp.*

7 MARKET FUTURE TRENDS

8 DISCLAIMER AND ABOUT US