PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521878

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1521878

Adeno-Associated Virus (AAV) CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

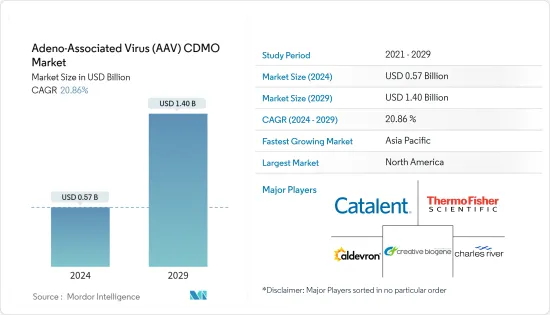

The Adeno-Associated Virus CDMO Market size is estimated at USD 0.57 billion in 2024, and is expected to reach USD 1.40 billion by 2029, growing at a CAGR of 20.86% during the forecast period (2024-2029).

The key factors driving the growth of the adeno-associated virus CDMO market include the increasing use of gene therapy, advancements in AAV vectors, and rising outsourcing of AAV vector manufacturing.

Companies operating in the AAV development field are developing new technologies and engaging in strategic activities that benefit the market. For instance, in November 2022, Thermo Fisher Scientific introduced the Gibco CTS adeno-associated virus (AAV) MAX Helper Free production system, which it claims can save time and reduce costs by 50%. The CTS AAV-MAX system includes several components: mammalian cells, a cell culture medium, a transfection kit, and a buffer.

In February 2022, Mirus Bio launched Transit-VirusGEN SELECT Transfection Kits for large-scale viral vector production for cell and gene therapy applications. The kits support pre-clinical and process development activities and consist of the TransIT-VirusGEN Transfection Reagent, a complex formation solution, and an enhancer. Hence, the introduction of AAV technologies is expected to increase its demand, and production is likely to boost the demand for CDMO services over the forecast period.

Furthermore, growing research identifying the importance of gene therapy in treating life-threatening diseases is propelling market growth. For instance, the study published in the Radiology and Oncology Journal in February 2022 claimed that the use of adeno-associated viral vectors to treat cancer had the potential to change the area of oncology. Virus vectors, in particular, provide a unique mix of effective gene delivery and immune system engagement for anti-tumour responses. Such studies are expected to increase the adoption of AAV contract manufacturing in designing cancer therapies, driving market growth.

However, production capacity challenges and regulatory issues are expected to hinder market growth in the long run.

Adeno-Associated Virus (AAV) CDMO Market Trends

Cell and Gene Therapy Development is Expected to Witness Rapid Growth Over the Forecast Period

Cell and gene therapy development is one of the most rapidly evolving segments. Several developments are occurring in the cell and gene therapy space that are driving segmental growth. For instance, in June 2023, Laurus Labs Ltd, one of the pharma companies in India, inked a memorandum of agreement (MoA) with IIT Kanpur (IITK) for in-licensing novel gene therapy assets using AAV vectors and bringing them to market.

Similarly, in December 2022, Merck partnered with Synplogen, a Kobe University spin-off, to enhance gene therapy development in Japan. This collaboration combined Merck's CTDMO expertise with Synplogen's capabilities, facilitating streamlined processes for gene therapy development, manufacturing, and testing.

In August 2022, Polyplus unveiled its groundbreaking Transgene Plasmid Engineering Services tailored specifically for viral vector production. The expansion of Polyplus' plasmid services provided a comprehensive range of options for next-generation viral vector and gene therapy manufacturing. These services can be utilized independently or in conjunction with the industry-standard PEIpro and FectoVIR-AAV reagents and kits. In May 2022, AGC Biologics expanded its Longmont, Colorado facility, adding viral vector suspension technology and capacity to support the development and manufacturing of gene therapies. These new capabilities, which were launched online in the third quarter of 2022, enhanced the site's existing viral vector and cell therapy services.

Consequently, due to factors such as the burgeoning involvement of companies in cell and gene therapy and robust collaborations among them, the cell and gene therapy segment is poised for significant growth in the future.

North America is Expected to Dominate the Market During the Forecast Period

North America is expected to dominate the market due to factors such as the well-established pharmaceutical and biotechnology industry and the rising focus on contract manufacturing across the region.

The companies are investing in research and development of gene therapy. For instance, in October 2022, Astellas invested USD 50 million in Taysha Gene Therapies Inc. in order to gain access to two of its AAV gene therapy initiatives for Rett syndrome and giant axonal neuropathy (GAN). Similarly, the National Cancer Institute (NIC), based on data updated in March 2022, was given USD 6.9 billion by the Consolidated Appropriations Act 2022. This was a net increase of USD 353 million over FY 2021. The FY 2022 allocation included USD 194 million in funding for the Cancer Moonshot and USD 50 million for the Childhood Cancer Data Initiative. Thus, increasing investments in enabling a precision medicine approach across the country are expected to drive the market during the forecast period.

Companies operating in the area are investing heavily in the research and development of advanced and effective therapeutics for cancer treatment and launching new products, which is expected to further boost the growth of the cancer segment in the market studied.

In November 2022, the US Food and Drug Administration approved Hemgenix, an adeno-associated virus vector-based gene therapy for treating adults with Hemophilia B or life-threatening historical hemorrhage or who have repeated, serious, severe spontaneous bleeding episodes.

The North American market is experiencing growth as a result of increasing investments by companies and the presence of a well-established pharmaceutical industry in the region.

Adeno-Associated Virus (AAV) CDMO Industry Overview

The market for AAV CDMO is moderately competitive, with several companies operating globally. The companies are mainly focusing on strategic activities such as collaboration, mergers, acquisitions, and partnerships to sustain themselves in the market. Some of the key players operating in the market include Thermo Fischer Scientific Inc., Creative Biogene, Catalent Inc., Charles River Laboratories International Inc., and Danaher (Aldevron).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Use of Gene Therapy

- 4.2.2 Advacements in AAV Vector

- 4.2.3 Rising Outsourcing of AAV Vector Manufacturing

- 4.3 Market Restraints

- 4.3.1 Production Capacity Challenges

- 4.3.2 Regultory Issues

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size - Value in USD)

- 5.1 By Workflow

- 5.1.1 Upstream Processing

- 5.1.2 Downstream Processing

- 5.2 By Culture Type

- 5.2.1 Adherent Culture

- 5.2.2 Suspension Culture

- 5.3 By Application

- 5.3.1 Cell & Gene Therapy Development

- 5.3.2 Vaccine Development

- 5.3.3 Biopharmaceutical & Pharmaceutical Discovery

- 5.3.4 Biomedical Research

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biopharmaceutical Companies

- 5.4.2 Academic & Research Institutes

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aldevron

- 6.1.2 Charles River Laboratories Inc.

- 6.1.3 Forge Biologics

- 6.1.4 Creative Biogene

- 6.1.5 Genezen

- 6.1.6 VIRALGEN

- 6.1.7 Catalent Inc.

- 6.1.8 Merck KGaA

- 6.1.9 ViroCell Biologics Ltd

- 6.1.10 Biovian Oy

- 6.1.11 Thermo Fisher Scientific Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS