PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644902

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644902

US FTL Freight Brokerage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

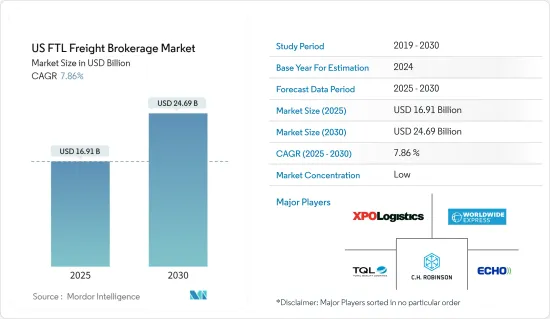

The US FTL Freight Brokerage Market size is estimated at USD 16.91 billion in 2025, and is expected to reach USD 24.69 billion by 2030, at a CAGR of 7.86% during the forecast period (2025-2030).

Key Highlights

- The full truckload freight brokerage market in the United States experienced a strong hit by the pandemic, as the freight transportation and logistics industry slowed down in the country due to pandemic restrictions and the closing of cross-border shipments. The impact of the pandemic has created massive challenges in freight yards and warehouses, where many facilities struggling with COVID-19 conditions have cut their staffing levels and reduced operating hours at loading and receiving docks.

- In recent years, the US has experienced substantial growth in full-truckload (FTL) services owing to the demand from inland freight movement and cross-border trade between the United States, Canada, and Mexico. The increase in year-on-year growth of the United States exports and imports also supports the development of the freight brokerage industry in the nation. The significance of freight brokers is growing owing to their role as intermediaries and facilitating the business of both shippers and carriers. Transport and freight forwarding services are on the rise in the United States due to the number of e-commerce companies emerging globally.

- Full truckload freight brokerage is still in a growth phase and is a major attraction for new shippers looking to penetrate the domestic market. However, established shippers seek long-term contracts with brokerage firms and carriers to gain a leading position in the international freight forwarding industry. FTL brokers facilitate the shipping service for shippers and monitor carriers' shipments. Many freight brokerage firms are strengthening their digital marketplace and are adopting technology, such as automated pricing, application programming interface (API) connectivity, data science, and internally facing technology. Companies are increasing their investments and spending on technologies and innovations as consumer preferences are also changing. With the increasing technological advancements, traditional players face intense competition from startups. For instance, C.H. Robinson, one of the largest freight brokers in North America, announced in 2019 that it would double its technology spending through 2024 to compete with digital startups.

- The market has seen one scenario play out repeatedly. Shippers with less-than-truckload-size loads are paying for full truckload (FTL) service to ensure faster delivery of goods, resulting in space and inefficiencies. Startups have mostly attacked this sector. This is because it is less complex than LTL and parcel and contains a larger piece of the pie. The most funded startups, like Transfix, Convoy, and Uber Freight, focus on freight matching. They are replacing traditional brokers by utilizing mobile technology and automating manual operations.

US FTL Freight Brokerage Market Trends

Fluctuating Fuel prices Hampering the Growth of the Market

Carriers (logistics companies) may charge higher rates if market conditions warrant or cover higher operating costs. As a result, if brokerage firms cannot increase pricing for their customers, revenues, and income from operations may decrease. The increased market demand for FTL services and pending regulatory changes may reduce available capacity and raise carrier pricing. Fuel prices can be volatile and challenging to forecast. Over the last five years, fuel prices have fluctuated dramatically. Clients anticipate that lower prices will pass them on to fuel savings. If carriers do not lower their prices to reflect decreases in fuel costs, shipment volume may suffer as customers seek alternative shipping options.

This volume decrease would harm the brokerage companies' gross profits and operating income. In the event of rising fuel prices, carriers can be expected to charge higher fees to cover higher operating expenses. The gross profit of brokerage firms and income from operations may decrease if they cannot continue to pass through to their clients the total amount of these increased costs. Higher fuel costs could also cause material shifts in the percentage of revenue by transportation mode, as clients may elect to utilize alternative transportation modes. Any material shifts to transportation modes concerning which brokerage firms realize lower gross profit margins could impair operating results. The Ukraine-Russia war also caused a spike in fuel prices as Russia is the third-largest producer of crude oil.

Construction Sector is the Fastest-growng End-user Segment

Despite near-term challenges in certain construction sectors, the medium to long-term growth story in the United States remains intact. The construction industry in the United States is expected to grow steadily over the next four quarters. In the United States, several projects are working their way through the planning phase, whereas others have finally resumed after a year of global pandemic-related delays. Despite the challenges associated with the global supply chain, such as rising raw material prices, shortage of building materials, and lack of skilled labor, the residential construction sector will continue its stable growth over the four to eight quarters.

The residential construction sector largely remains supported by low lending rates, strong demand for bigger homes, and low housing inventory in the United States. Over the next few quarters, the healthcare and education sectors will receive more attention. In November 2021, the US Congress passed a USD 1 trillion infrastructure spending bill.

The infrastructure legislation proposes USD 550 billion in new federal expenditure over the next eight years in the United States for the upgrade of roads, bridges, and highways and modernizing the city transit systems and passenger rail networks. While the new infrastructure spending bill falls short of the original USD 2.3 trillion proposals, the USD 1 trillion spending on various United States infrastructure sectors will keep supporting the growth of the construction industry over the next four to eight quarters in the country.

US FTL Freight Brokerage Industry Overview

The US FTL freight brokerage market is relatively fragmented, with prominent regional, global, and various small- and medium-sized local players. Major players in the industry include CH Robinson, Echo Global Logistics, Worldwide Express, Landstar System Inc., Schneider, SunteckTTS, GlobalTranz, JB Hunt Transport Inc., Hub Group, and BNSF Logistics LLC. New entrants such as Convoy, Uber Freight, uShip, etc., are trying to gain significant market share by offering price transparency, online load boards, and freight marketplaces for booking freight via mobile apps and removing human interaction in the freight booking and payment process.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Background

- 1.2 Study Assumptions and Market Definition

2 RESEARCH AND ENGAGEMENT FRAMEWORKS

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

- 2.5 Project Process and Structure

- 2.6 Engagement Frameworks

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Increasing demand for efficient transportation

- 4.2.1.2 Growing eCommerce industry

- 4.2.2 Market Challenges/Restraints

- 4.2.2.1 Intense competition affecting the market

- 4.2.2.2 Fluctuating fuel prices

- 4.2.3 Market Opportunities

- 4.2.3.1 Adoption of advanced technologies

- 4.2.3.2 Focus on sustainability in logistics

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Industry Value Chain / Supply Chain Analysis

- 4.5 US Logistics Industry (Overview, Trends, R&D, Key Statistics, etc.)

- 4.6 Key Government Regulations and Initiatives

- 4.7 Insights into Freight Rates

- 4.8 Technology Snapshot

- 4.9 Qualitative and Qualitative Insights into the US Customs Clearance Sector

- 4.10 Insights into Chicago and Illinois - FTL Freight Brokerage

- 4.11 Insights into Wages and Pay Structure in the Freight Brokerage Market

- 4.12 Assessment on the Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By End User

- 5.1.1 Manufacturing and Automotive

- 5.1.2 Oil and Gas, Mining, and Quarrying

- 5.1.3 Agriculture Fishing, and Forestry

- 5.1.4 Construction

- 5.1.5 Distributive Trade

- 5.1.6 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Overview

- 6.2 Company Profiles

- 6.2.1 CH Robinson

- 6.2.2 Total Quality Logistics

- 6.2.3 XPO Logistics Inc.

- 6.2.4 Echo Global Logistics

- 6.2.5 Worldwide Express

- 6.2.6 Coyote Logistics

- 6.2.7 Landstar System Inc.

- 6.2.8 Schneider

- 6.2.9 Suntecktts

- 6.2.10 Globaltranz

- 6.2.11 J.B. Hunt Transport Inc.

- 6.2.12 Hub Group

- 6.2.13 BNSF Logistics LLC

- 6.2.14 Kag Logistics Inc.

- 6.2.15 Transplace*

7 FUTURE OF THE MARKET

8 APPENDIX

9 CREDENTIALS

- 9.1 Illustrative List of Clients

- 9.2 Similar Engagements Within the Industry

10 ABOUT US