Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690980

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690980

Europe Animal Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 258 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

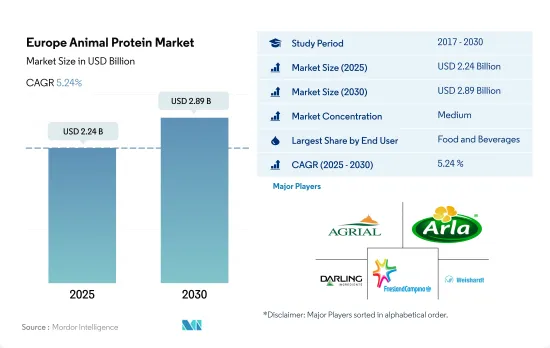

The Europe Animal Protein Market size is estimated at 2.24 billion USD in 2025, and is expected to reach 2.89 billion USD by 2030, growing at a CAGR of 5.24% during the forecast period (2025-2030).

F&B and supplements together accounted for more than 50% of share in 2022 due to rising number of fitness enthusiasts coupled with increasing demand for protein-based food products across the region

- The market has animal protein applications in many end-user segments, primarily driven by the F&B and supplements segments. In 2022, the two segments together held a share of 40% of animal protein volume consumed in Europe. Increased consumption of gelatin as an emulsifier in protein-based products is the major factor driving the market. In 2021, 60% of millennials and Gen Z consumers sought curated baked bakeries that offered functional bakery goods in Europe.

- The supplements have been gaining acceptance among the rising number of fitness enthusiasts in the region. In fact, under the supplements segment, sports/performance nutrition remained the most dominant and yet the fastest-growing sub-segment, with a projected CAGR of 5.40%, by volume, during the forecast period. Over the review period, the number of members in health and fitness clubs in Europe rose by about 12 million. This increase portrays a vast potential for products like protein powders. Top athletes are increasingly influencing millennials worldwide. Due to this, the demand for energizing products and weight management sports nutrition is surging.

- Insect protein dominates the animal feed market and is anticipated to register a CAGR of 2.39%, by value, throughout the forecast period. In Europe, more than USD 1 billion has been invested in this sector since its establishment, and this figure is expected to reach USD 2.95 billion at the end of the forecast period. The use of insect-processed animal proteins (PAPs) in poultry and pig feed was approved by the European Union in 2021, which is expected to create new opportunities, beginning with the introduction of such components into such animals' diets.

Russia holds significant share in 2022 due to strong demand of animal protein from Russian bakeries

- By country, Russia retained its top position in 2022. Food and beverages remained the largest consumer of animal proteins, with the bakery segment accounting for a major volume of 54% during the base year. Animal proteins, such as gelatin and collagen, are widely used in making cakes and pastries. Cakes and pastries make up the second-largest industry, holding 11% of the market shares in the region. An average Russian citizen consumes about 260 pounds of baked goods per year. In 2020, the country had over 690 large bakeries, 4,800 mid-sized enterprises, and more than 7,000 small and micro-bakeries.

- The UK whey protein market holds a share of 26.27% in Europe. It is one of the strongest markets in Europe. Whey protein has increased applications in the supplements and food and beverage industries in the United Kingdom. Almost 3.5 million Britons were recorded to have had type-3 diabetes in 2020. To cope with diabetes, whey protein is effective as it instantly increases the insulin level. The intake of whey protein supplements helps people with type-3 diabetes control their blood sugar levels. As a result, there is a steady increase in the demand for whey protein in the supplements segment.

- Germany holds a significant share of the animal protein market. Gelatin protein (26.85%) and whey protein (20.14%) hold the major market shares in the country. Gelatin protein is dominated by the food and beverage sector, and the beverage sub-segment is the fastest-growing in the market. In 2021, an average German consumed 9.9 liters per capita of fruit juice. Gelatin is effective in removing fruit juice precipitates that might cause haze. Gelatin, when used in doses of 1%-5% concentrations, aids the retention of natural fluids and improves texture and flavor.

Europe Animal Protein Market Trends

The growing consumption of animal protein fuels opportunities for key players in the ingredients category

- In the United Kingdom, from 2016 to 2019, the average daily protein intake of individuals aged 19-64 years was 76 g per person, which was more than the 64 g/day average adult daily requirement. This number was calculated using a reference intake value of 0.83 g/kg of body weight per day. The average daily consumption of animal protein per person is projected to be 39.6 g, with 25.9 g coming from meat and meat products and 9.9 g from milk and milk products. Accordingly, the total domestic milk production has risen. Less than 7% of the domestic production is exported, thereby providing easy access to manufacturers.

- The market for whey protein is mainly driven by the growing popularity of fitness centers and health clubs, leading to a rise in whey consumption. The annual whey protein import increased exponentially by 15.09% in 2021 from 2019. However, with a great focus on overall health and consumers' interest in clean-label products, the sports nutrition industry's demand for natural ingredients has been growing. Ingredients, such as organic and grass-fed whey, have gained prominence due to health and ethical concerns.

- Women seek sports nutrition supplements for lean body, strength, and performance. Encouragement from nutritionists and other fitness experts is also boosting the market sentiment for sports nutrition in the region. Growing veganism, demand for plant-based products, and changing dietary preferences among consumers are being witnessed globally. The low inclination toward meat-based products is visible among consumers, which is a major restraining factor for the animal protein market. The number of vegans in Europe doubled from 1.3 million to 2.6 million, representing 3.2% of the population in 2021.

Meat and milk production contributes majorly in terms of raw material for plant protein manufacturers

- The graph given depicts the production data for raw materials such as meat of cattle, pigs, and chicken (with bone, fresh or chilled), raw milk from cattle and goats, skim milk from cows, and dry whey powder. Germany is the leading producer of milk in the European Union, accounting for more than 21% of milk deliveries in the European Union in 2020. Although the country has been observing a decline in the count of cattle farms, the average size of the farms is witnessing an upsurge. The rise in milk production is attributed to the escalated volume of milk production per cow. Over the years, milk production has been concentrated in the grassland regions of northwestern and southern Germany.

- Milk production is constantly rising in the United Kingdom despite the continuous decline in the number of dairy cows. As of December 2022, the total number of dairy cows in the United Kingdom that were greater than 12 months old stood at 2.66 million heads. In the same year, milk production per cow amounted to 8,169 liters per annum, an increase of 3.5% compared to 7,893 liters in 2017.

- In 2020, there were over 76 million cattle in the European Union (EU), and beef production reached 6.8 million tonnes, making the European Union the world's third-largest producer after the United States and Brazil. The sector is diverse in terms of herd size, farm structure, and geographical distribution of farms in the European Union. Three EU member states alone produce half of the EU's beef: France (21.2%), Germany (17.8%), and Italy (11.1%).

Europe Animal Protein Industry Overview

The Europe Animal Protein Market is moderately consolidated, with the top five companies occupying 40.63%. The major players in this market are Agrial Enterprise, Arla Foods amba, Darling Ingredients Inc., Koninklijke FrieslandCampina NV and SAS Gelatines Weishardt (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90136

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 France

- 3.4.2 Germany

- 3.4.3 Italy

- 3.4.4 United Kingdom

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Protein Type

- 4.1.1 Casein and Caseinates

- 4.1.2 Collagen

- 4.1.3 Egg Protein

- 4.1.4 Gelatin

- 4.1.5 Insect Protein

- 4.1.6 Milk Protein

- 4.1.7 Whey Protein

- 4.1.8 Other Animal Protein

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Belgium

- 4.3.2 France

- 4.3.3 Germany

- 4.3.4 Italy

- 4.3.5 Netherlands

- 4.3.6 Russia

- 4.3.7 Spain

- 4.3.8 Turkey

- 4.3.9 United Kingdom

- 4.3.10 Rest of Europe

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Agrial Enterprise

- 5.4.2 Arla Foods amba

- 5.4.3 Darling Ingredients Inc.

- 5.4.4 Groupe LACTALIS

- 5.4.5 Koninklijke FrieslandCampina NV

- 5.4.6 Lactoprot Deutschland GmbH

- 5.4.7 LAITA

- 5.4.8 SAS Gelatines Weishardt

- 5.4.9 Ynsect

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.