PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1404064

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1404064

Saudi Arabia Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

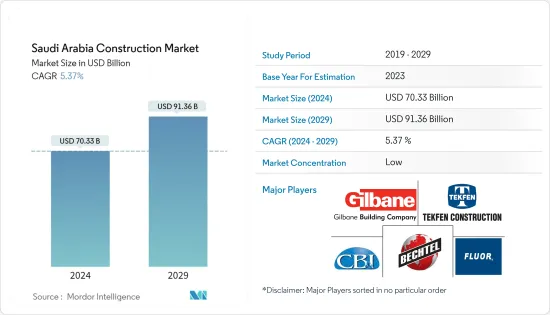

The Saudi Arabia Construction Market size is estimated at USD 70.33 billion in 2024, and is expected to reach USD 91.36 billion by 2029, growing at a CAGR of 5.37% during the forecast period (2024-2029).

Key Highlights

- The market is driven by Riyadh's Vision 2030 national development plan for diversifying and privatizing the huge Saudi economy. This plan includes several huge megaprojects like the Neom Future Cities, Qiddiya Entertainment City, and the Red Sea Project. Saudi Arabia offers the region's biggest pipeline of construction opportunities.

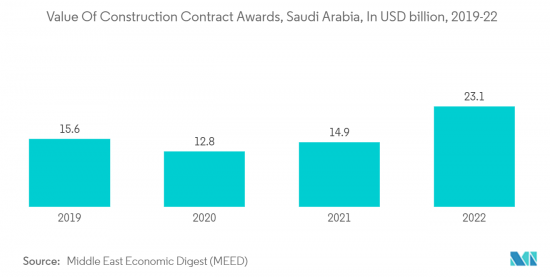

- Due to the COVID-19 pandemic, the Saudi Arabian construction market had to deal with many problems. The pandemic had a big effect on Saudi Arabia's construction industry. The rate at which construction contracts were given out dropped significantly in 2020 and 2021. However, the Kingdom had the highest value of projects awarded in 2022, which showed its commitment to diversifying the economy and changing the country in line with its Vision 2030,

- In 2022, the number of buildings built in the Kingdom grew by 3.2%. Saudi Arabia has been the strongest market in the MENA region for the past four years in a row, with the highest overall value of project awards. As of October 2022, Saudi Arabia had a 35% market share and won contracts worth USD 31 billion compared to USD 87 billion for all of MENA.

Saudi Arabia Construction Market Trends

Increase in the Total Value of Construction Contracts Awarded in Saudi Arabia

Saudi Arabia's pipeline value of unawarded (pre-execution) projects is estimated at USD 1.1 trillion, which includes projects from the study stage through the leading contractor bid. Approximately 70% comprise construction sector projects, with residential, cultural, leisure, and hospitality as sub-sector leaders. This is the driving force behind the Vision 2030 strategy. In the second half of 2022, 13,000 hotel keys were expected to be delivered in Riyadh, Jeddah, and Makkah, accentuating the continuation of the development of the Kingdom's hospitality sector.

The top ten contractors in the Kingdom are responsible for USD 400 billion in projects, which are currently in the execution stage, accounting for 40% of the total future pipeline value of USD 1.1 trillion. According to MEED Projects, the total value of projects awarded in Saudi Arabia between 2021 and 2025 is expected to reach USD 569 billion, with a total of USD 85 billion (15%) awarded to date across 2021 and 2022 (October end).

Global economic volatility in the first two quarters of 2022 created challenges in the local construction market regarding delivery lead times and instant price increases, with suppliers reluctant to guarantee prices for extended periods.

Emergence of Saudi Arabia as a Cultural and Religious Tourism Center is Likely to Promote the Construction Demand

The Kingdom's hotel construction rate is anticipated to nearly triple in 2023, with nearly 50% of the 167 projects on file due for delivery within those 12 months.

Altogether, 56% (35,884) of the 63,753 Saudi Arabian rooms in the database are expected to come online in 2023, dwarfing the 9,207 keys from the 24 projects in 2022. Development is anticipated to return to near this rate in 2024, with 23 projects delivering 9,599 rooms, while 2025 and beyond are likely to see at least another 40 hotels representing 9,063 keys joining the market.

First-class four-star properties account for 77 projects and 30,229 rooms - 46% of the total, with the remaining 54% in the five-star luxury segment, equating to 90 builds comprising 33,524 keys.

A significant proportion of the development wave is due to a number of megaprojects taking shape in Makkah (Mecca). While in terms of pure project totals, the 27 hotels slated for the Islamic religious center only put it third on the top Saudi cities list, the 31,957 keys which are expected to become available in the area are more than three times that of the number one city by project number - which is Riyadh, with 45 hotels totaling 9,302 rooms.

Second in this analysis is Jeddah, with 33 projects delivering 7,148 rooms, while fourth in the list is Al Wajh, representing 12 projects of collectively 4,868 keys.

Saudi Arabia Construction Industry Overview

The Saudi Arabian construction market is fragmented and highly competitive, with the presence of major international players. The Saudi Arabian construction market presents opportunities for growth during the forecast period, which is expected to further drive the competition in the market. With a few players holding a significant market share, the Saudi Arabian construction market has an observable level of consolidation. Some of the key players include JGC Corp., SNC-Lavalin, Fluor Corp., Van Oord Dredging & Marine Contractors BV, and VINCI. The government's focus on the creation of general infrastructure as well as energy and utility construction projects as part of its effort to diversify its economy away from the oil industry is anticipated to help the construction industry's output.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Economic and Construction Market Scenario

- 4.2 Technological Innovations in the Construction Sector

- 4.3 Spotlight on Key Ongoing and Upcoming Projects

- 4.4 Industry Value Chain/Supply Chain Analysis

- 4.5 Impact of Government Regulations and Initiatives on the Industry

- 4.6 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Saudi Arabia Vision 2030

- 5.1.2 Green and Sustainable Building Initiatives

- 5.2 Market Restraints

- 5.2.1 Saudization (Nitaqat) Program

- 5.2.2 Declining Crude Oil Prices

- 5.3 Market Opportunities

- 5.3.1 Increased Foreign Investment

- 5.3.2 Business Tourism

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers/Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Sector

- 6.1.1 Residential

- 6.1.2 Commercial

- 6.1.3 Industrial

- 6.1.4 Infrastructure (Transportation)

- 6.1.5 Energy and Utilities Construction

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Bechtel

- 7.2.2 CB&I LLC

- 7.2.3 Fluor Corp.

- 7.2.4 Tekfen Construction and Installation Co. Inc.

- 7.2.5 Gilbane Building Co.

- 7.2.6 Jacobs

- 7.2.7 AL Jazirah Engineers & Consultants

- 7.2.8 Al Latifa Trading and Contracting

- 7.2.9 Afras Trading and Contracting Company

- 7.2.10 Al-Rashid Trading & Contracting Company*

8 FUTURE OF THE MARKET

9 APPENDIX

- 9.1 Macroeconomic Indicators (GDP Breakdown by Sector, Contribution of Construction to Economy, etc.)

- 9.2 Key Production, Consumption, Export, and Import Statistics of Construction Materials