PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1708241

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1708241

Automotive Pump for Thermal System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

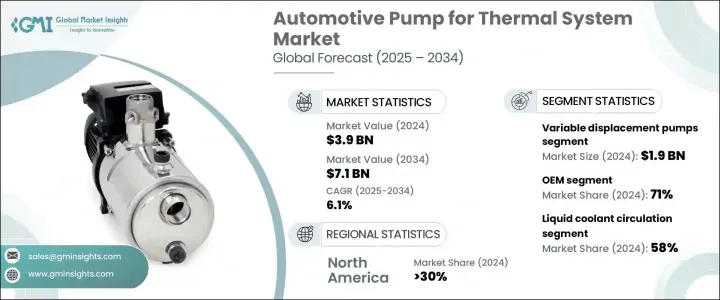

The Global Automotive Pump for Thermal System Market, valued at USD 3.9 billion in 2024, is projected to grow at a CAGR of 6.1% from 2025 to 2034. As the automotive industry shifts towards electric vehicles (EVs) and hybrid electric vehicles (HEVs), the demand for efficient thermal management systems is rising. These systems are crucial for maintaining optimal temperatures in various vehicle components, including batteries and power electronics, which are critical to EV performance. The demand for advanced cooling solutions is growing as these thermal systems help enhance vehicle functionality and battery life by maintaining temperature stability.

A significant factor driving this market is the rise of thermal energy recovery systems (TERS), which are used to capture waste heat produced by engine or exhaust systems. These systems improve overall energy efficiency and further boost the demand for automotive pumps. These pumps play a vital role by circulating coolant through the system, transferring heated liquid energy to operate auxiliary features, or enhancing driving performance. They are essential in the development of modern vehicles, including EVs and HEVs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $7.1 Billion |

| CAGR | 6.1% |

The market is segmented based on pump type, with centrifugal pumps, positive displacement pumps, and variable displacement pumps being the main categories. Variable displacement pumps accounted for USD 1.9 billion of the market in 2024 and are expected to show significant growth over the forecast period. These pumps are preferred for their flexibility and responsiveness in complex thermal systems, where they provide better control under varying driving conditions, such as high-performance driving or in cold weather and heavy traffic situations.

The market is also divided by sales channel into OEM and aftermarket segments. In 2024, the OEM segment held a dominant market share of 71%. OEMs use direct-to-consumer platforms, including e-commerce, to distribute replacement parts and aftermarket pumps. This approach not only improves their market reach but also enhances customer support and feedback.

By refrigerant type, the market is segmented into oil-based, liquid coolant circulation, and air-based refrigerants. The liquid coolant circulation segment held a majority share of 58% in 2024, driven by the growing demand for efficient battery temperature management in electric and hybrid vehicles.

The automotive pump for thermal system market is further categorized by propulsion type, with the internal combustion (IC) engine segment holding the largest share in 2024. Thermal management is particularly crucial in turbocharged engines, where effective cooling systems are required to prevent overheating and ensure long-lasting performance.

In North America, the market was dominated by the U.S., with the region accounting for over 30% of the global market share in 2024. The demand for thermal management systems in EVs is increasing due to advancements in battery technology and the push for more energy-efficient vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material supplier

- 3.2.2 Component supplier

- 3.2.3 Pump assemblers

- 3.2.4 Service provider

- 3.2.5 Technology provider

- 3.2.6 End use

- 3.3 Profit margin analysis

- 3.4 Cost breakdown analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising demand for electric and hybrid vehicles

- 3.8.1.2 Growing adoption of thermal energy recovery systems

- 3.8.1.3 Expansion of aftermarket and replacement demand

- 3.8.1.4 Growth of autonomous and connected vehicles

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High cost of advanced pump technologies

- 3.8.2.2 Complexity in retrofitting advanced thermal pumps

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Pump, 2021 - 2034 ($Mn & Units)

- 5.1 Key trends

- 5.2 Centrifugal pumps

- 5.2.1 Electric water pump

- 5.2.2 Mechanical water pump

- 5.3 Positive displacement pumps

- 5.3.1 Gear pump

- 5.3.2 Vane pump

- 5.3.3 Piston pump

- 5.3.4 Screw pump

- 5.4 Variable displacement pumps

Chapter 6 Market Estimates & Forecast, By Watt, 2021 - 2034 ($Mn & Units)

- 6.1 Key trends

- 6.2 Below 50 W

- 6.3 50W – 100W

- 6.4 100W – 500W

- 6.5 Above 500W

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn & Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 BEV

- 7.4 PHEV

- 7.5 HEV

Chapter 8 Market Estimates & Forecast, By Refrigerant, 2021 - 2034 ($Mn & Units)

- 8.1 Key trends

- 8.2 Oil-based

- 8.3 Liquid Coolant Circulation (LCC)

- 8.4 Air-based

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aisin

- 10.2 BorgWarner

- 10.3 Bosch (Robert Bosch)

- 10.4 Continental

- 10.5 Denso

- 10.6 Eberspaecher

- 10.7 Fluid-o-Tech

- 10.8 Grayson

- 10.9 Hanon Systems

- 10.10 Hitachi Astemo

- 10.11 Infineon Technologies

- 10.12 Johnson Electric Holdings Limited

- 10.13 MAHLE

- 10.14 Marelli

- 10.15 Modine

- 10.16 Nidec Corporation

- 10.17 Rheinmetall AG

- 10.18 Schaeffler

- 10.19 Valeo

- 10.20 ZF