PUBLISHER: Roots Analysis | PRODUCT CODE: 1616883

PUBLISHER: Roots Analysis | PRODUCT CODE: 1616883

ADC Technology Market by Generation of Technology, Type of Conjugation, Type of Linker, Type of Payment Model Adopted and Key Geographical Regions : Industry Trends and Global Forecasts, Till 2035

ADC TECHNOLOGY MARKET (FOCUS ON ADC LINKER & ADC CONJUGATION TECHNOLOGIES): OVERVIEW

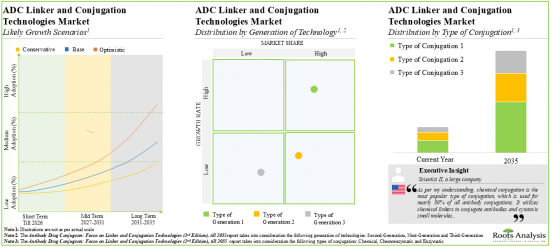

As per Roots Analysis, the global ADC technology market is estimated to grow from USD 1.18 billion in the current year to USD 4.37 billion by 2035, at a CAGR of 11.5% during the forecast period, till 2035.

The market sizing and opportunity analysis has been segmented across the following parameters:

Generation of Technology

- Third-Generation

- Second-Generation

- Next-Generation

Type of Conjugation

- Chemical

- Chemoenzymatic

- Enzymatic

Type of Linker

- Cleavable

- Non-cleavable

Type of Payment Model Adopted

- Upfront Payments

- Milestone Payments

Key Geographical Regions

- North America

- Europe

- Asia-Pacific and Rest of the World

ADC TECHNOLOGY MARKET (FOCUS ON ADC LINKER & ADC CONJUGATION TECHNOLOGIES): GROWTH AND TRENDS

Antibody drug conjugate has emerged as a versatile anti-cancer therapy that has been proven to be more effective and less toxic to patients. Such interventions are designed to identify specific antigens that are expressed on the surface of cancer (target) cells so that the effects of the cytotoxin / drug are focused on the elimination of only the cancerous cells. Over the past few years, more than 20 ADC therapies have been approved by various regulatory agencies. Moreover, over 350 drug therapies are being evaluated in clinical trials across the globe. This demonstrates the extensive development initiatives that are being undertaken by stakeholders in this domain. However, the complex design and structure of ADCs present a significant challenge to the overall tolerability and efficacy of the molecule. Thus, more advanced ADC technology is required to generate the controlled assembly of ADCs while maintaining tolerability and safety profiles. It is worth highlighting that significant investments have been made in the ADC technology market in order to meet the growing demand for antibody drug conjugates. As drug developers invest more in these innovative therapies, the market for ADC technology is likely to witness substantial market growth during the forecast period.

ADC TECHNOLOGY MARKET (FOCUS ON ADC LINKER & ADC CONJUGATION TECHNOLOGIES): KEY INSIGHTS

The report delves into the current state of the ADC technology market and identifies potential growth opportunities within the industry. Some key findings from the report include:

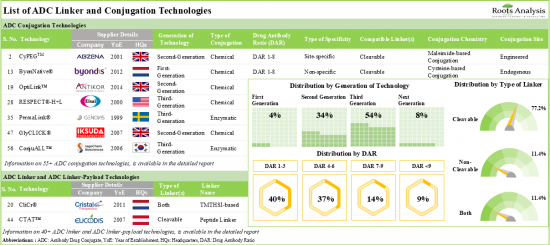

1. At present, over 95 ADC linker and conjugation technologies are being offered by various technology developers across the globe; around 55% of these are third-generation technologies.

2. The current market landscape is highly fragmented, featuring the presence of both new entrants and well-established players across key geographical regions.

3. Over 2,100 patents have been filed / granted for ADC linker and conjugation technologies, by industry and non-industry players, to protect the intellectual property generated within this field.

4. To cater to the increasing demand for homogenous ADC therapies, a number of players have stepped up to introduce technologically advanced platforms and establish a strong brand position in this industry.

5. A considerable increase in partnership activity has been witnessed in this domain; ~70% of the deals were related to licensing of technologies, primarily focused on product development and R&D purposes.

6. ADC drug developers are anticipated to continue to form strategic alliances with ADC linker and conjugation technology providers to further strengthen their respective technology portfolios.

7. Stakeholders have adopted different business models to maximize the gain from ADC technologies; a considerable number of players have signed multiple partnerships to out-license their technologies.

8. In pursuit of gaining a competitive edge, stakeholders are actively enhancing their existing capabilities to improve their respective technology portfolios and compliance with evolving industry standards.

9. At present, over 350 ADC therapeutic candidates are undergoing clinical trials for the treatment of various oncological disorders; majority of these ADCs are being evaluated as monotherapies.

10. With the growing focus on development of efficacious and site-selective drugs, the ADCs linker and conjugation technologies market is anticipated to witness an annualized growth of ~15%, over the next decade.

11. The estimated market opportunity is projected to be well distributed across different types of linkers and key geographical regions.

ADC TECHNOLOGY MARKET (FOCUS ON ADC LINKER & ADC CONJUGATION TECHNOLOGIES): KEY SEGMENTS

Third-Generation Technologies are Likely to Dominate the ADC Technology Market During the Forecast Period

Based on the generation of technology, the market is segmented into second-generation, third-generation and next-generation. It is worth highlighting that majority of the current ADC technology market is captured by third-generation technologies and this trend is likely to remain the same in the forthcoming years.

Currently, Chemical Conjugation Segment Occupies the Largest Share of the ADC Technology Market

Based on the type of conjugation, the market is segmented into chemical, chemoenzymatic and enzymatic. The current market is expected to be driven by chemical conjugators. It is worth highlighting that the chemoenzymatic segment is likely to grow at a relatively higher CAGR, during the forecast period.

Cleavable Segment is Likely to Capture the Largest Share of the ADC Technology Market During the Forecast Period

Based on the type of linker, the market is segmented into cleavable and non-cleavable. It is worth highlighting that majority of the current ADC technology market is captured by cleavable linkers and this trend is unlikely to change in the mid-long term.

North America Accounts for the Largest Share of the Market

Based on key geographical regions, the market is segmented into North America, Europe, and Asia-Pacific and Rest of the World. A significant proportion of the market is expected to be captured by North America and Europe. It is worth highlighting that, over the years, the market in Asia-Pacific and Rest of the World is expected to grow at a higher CAGR.

Example Players in the ADC Technology Market

- Alteogen

- Ambrx

- Antikor

- Catalent Biologics

- Heidelberg Pharma

- Iksuda Therapeutics

- LegoChem Biosciences

- Mersana Therapeutics

- NBE-Therapeutics

- Seattle Genetics

- Sutro Biopharma

Primary Research Overview

The opinions and insights presented in this study were influenced by discussions conducted with multiple stakeholders. The research report features detailed transcripts of interviews held with the following industry stakeholders:

- Scientist, Abzena

- Chief Scientific Officer, MedLink Therapeutics

- Head of Business Development, Merck KGaA

- Board Member, Singzyme

- General Manager, Research and Development, Director of ADC Process Development, Ajinomoto

- Head of Research, Eucodis Bioscience

- Former Chief Business Officer, NBE-Therapeutics

- Chief Executive Officer, Shanghai Miracogen

- Chief Scientific Officer, Synaffix

ADC TECHNOLOGY MARKET (FOCUS ON ADC LINKER & ADC CONJUGATION TECHNOLOGIES): RESEARCH COVERAGE

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the ADC linker and antibody conjugation technologies, focusing on key market segments, including [A] generation of technology, [B] type of conjugation, [C] type of linker, [D] type of payment model adopted and [E] key geographical regions.

- Market Landscape: A comprehensive evaluation of ADC linker and conjugation technologies, considering various parameters, such as [A] type of technology, [B] availability of licensing, [C] generation of ADC technology, [D] site specificity, [E] type of conjugation, [F] drug antibody ratio, [G] compatible linker, [H] conjugation chemistry, [I] conjugation site, [J] type of linker. It also includes information on ADC linker and antibody conjugation technology companies, based on several parameters, such as their [K] year of establishment, [L] company size (based on number of employees) and [M] location of headquarters.

- Technology Competitiveness Analysis: A comprehensive competitive analysis of ADC linker and conjugation technologies, examining factors, such as portfolio strength, technology competitiveness and partnership activity (in terms of number of partnerships). The analysis was designed to enable stakeholder companies to assess their existing capabilities and identify opportunities to achieve a competitive edge in the industry.

- Company Profiles: In-depth profiles of key industry players engaged in the development of ADC linker and ADC conjugation technologies, focusing on [A] company overviews, [B] technology portfolio, [C] insightful recent developments and [D] an informed future outlook.

- Patent Analysis: Detailed analysis of various patents filed / granted related to ADC linker and ADC conjugation technologies based on [A] type of patent, [B] publication year, [C] application year, [D] number of granted patents and patent applications, [E] patent jurisdiction, [F] focus area, [G] CPC symbols, [H] patent age, [I] type of applicant (on the basis of number of patents), and [J] individual patent assignees (in terms of size of intellectual property portfolio). In addition, it includes a patent benchmarking analysis and detailed valuation analysis.

- Partnerships and Collaborations: An analysis of partnerships established in this sector, since 2014, based on several parameters, such as [A] year of partnership, [B] type of partnership, [C] type of partner, [D] generation of technology, [E] type of linker, [F] type of conjugation, [G] target therapeutic area(s), [H] most popular technologies, [I] most active players and [J] geographical location of the companies.

- Business Model Analysis: An insightful analysis on business models adopted by various ADC technology providers engaged in this industry along with the information on parameters, such as [A] year of partnership, [B] purpose of partnership, [C] type of business strategy adopted (technology-out licensing, technology-in licensing, product out-licensing, product in-licensing, collaborative research and others), [D] type of investment, [E] amount invested and [F] most active players.

- Likely Partner Analysis: A detailed evaluation of several antibody drug conjugate therapeutics developers that are most likely to collaborate with ADC linker and conjugation technology companies in the near future. This analysis considers various relevant parameters, including [A] developer strength (in terms of company size and its experience), [B] portfolio strength (based on type of linker and antibody structure), [C] pipeline strength (based on stage of development of a drug and number of pre-clinical molecules) and [D] therapeutic area.

- Brand Positioning Analysis: An insightful brand positioning analysis of prominent antibody conjugation technology providers, highlighting the current perceptions regarding their proprietary technologies by taking into consideration several relevant aspects, such as [A] experience of the technology provider, [B] number of technologies offered, [C] product diversity, [D] number of patents and [E] number of partnerships.

- Case Study: The report includes a case study discussing the overall landscape of the antibody drug conjugates market, based on a number of parameters, such as [A] stage of development, [B] target disease indication, [C] therapeutics area, [D] line of treatment, [E] dosing frequency, [F] type of therapy, [G] target antigen, [H] antibody isotype, [I] payload / cytotoxin / warhead, [J] payload type, [K] type of linker. Further, it highlights information on antibody drug conjugate developers, including details on [L] year of establishment, [M] company size and [N] location of headquarters and [N] most active players in this domain.

KEY QUESTIONS ANSWERED IN THIS REPORT

- How many companies are currently engaged in this market?

- Which are the leading companies in this market?

- What kind of partnership models are commonly adopted by industry stakeholders?

- Which developers are most likely to collaborate with ADC linker and conjugation technology providers?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

- Complimentary PPT Insights Packs

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 10% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Key Market Insights

- 1.3. Scope of the Report

- 1.4. Research Methodology

- 1.5. Frequently Asked Questions

- 1.6. Chapter Outlines

2. EXECUTIVE SUMMARY

3. INTRODUCTION

- 3.1. Chapter Overview

- 3.2. Antibody Drug Conjugates (ADCs)

- 3.2.1. Components of ADCs

- 3.2.1.1. Antibody

- 3.2.1.2. Cytotoxin

- 3.2.1.3. Linker

- 3.2.1. Components of ADCs

- 3.3. Advantages of ADCs Over Conventional Therapeutics

- 3.4. ADC Linker Technologies

- 3.4.1. Non-cleavable Linkers

- 3.4.2. Cleavable Linkers

- 3.4. ADC Conjugation Technologies

- 3.4.1. Chemical Conjugation

- 3.4.2. Enzymatic Conjugation

- 3.5. Future Perspectives

4. ADC LINKER AND CONJUGATION TECHNOLOGIES: MARKET LANDSCAPE

- 4.1. Chapter Overview

- 4.2. ADC Linker and Conjugation Technologies: Overall Market Landscape

- 4.2.1. Analysis by Type of Technology

- 4.2.2. Analysis by Availability of Licensing

- 4.3. ADC Conjugation Technologies

- 4.3.1. Analysis by Generation of Technology

- 4.3.2. Analysis by Site Specificity

- 4.3.3. Analysis by Type of Conjugation

- 4.3.4. Analysis by Drug Antibody Ratio

- 4.3.5. Analysis by Compatible Linker

- 4.3.6. Analysis by Conjugation Chemistry

- 4.3.7. Analysis by Conjugation Site

- 4.4. ADC Linker and ADC Linker-Payload Technologies

- 4.4.1. Analysis by Type of Linker

- 4.5. ADC Linker and Conjugation Technology Providers

- 4.5.1. Analysis by Year of Establishment

- 4.5.2. Analysis by Company Size

- 4.5.3. Analysis by Location of Headquarters

- 4.5.4. Analysis by Year of Establishment and Location of Headquarters

- 4.5.5. Analysis by Company Size and Location of Headquarters

- 4.6. ADC Conjugation Technologies Service Providers

5 TECHNOLOGY COMPETITIVENESS ANALYSIS

- 5.1. Chapter Overview

- 5.2. Assumptions and Key Parameters

- 5.3. Methodology

- 5.4. ADC Linker and Conjugation Technologies: Technology Competitiveness Analysis

- 5.4.1. Technologies Offered by Small Companies

- 5.4.2. Technologies Offered by Mid-sized Companies

- 5.4.3. Technologies Offered by Large Companies

6. COMPANY PROFILES

- 6.1. Chapter Overview

- 6.2. Companies Headquartered in North America

- 6.2.1. Ambrx

- 6.2.1.2. Company Overview

- 6.2.1.3. Financial Information

- 6.2.1.4. Technology Portfolio

- 6.2.1.5. Recent Developments and Future outlook

- 6.2.2. Catalent Biologics

- 6.2.2.1. Company Overview

- 6.2.2.2. Financial Information

- 6.2.2.3. Technology Portfolio

- 6.2.2.4. Recent Developments and Future outlook

- 6.2.3. Mersana Therapeutics

- 6.2.3.1. Company Overview

- 6.2.3.2. Financial Information

- 6.2.3.3. Technology Portfolio

- 6.2.3.4. Recent Developments and Future outlook

- 6.2.4. Seagen

- 6.2.4.1. Company Overview

- 6.2.4.2. Financial Information

- 6.2.4.3. Technology Portfolio

- 6.2.4.4. Recent Developments and Future outlook

- 6.2.5. Sutro Biopharma

- 6.2.5.1. Company Overview

- 6.2.5.2. Financial Information

- 6.2.5.3. Technology Portfolio

- 6.2.5.4. Recent Developments and Future outlook

- 6.2.1. Ambrx

- 6.3. Companies Headquartered in Europe

- 6.3.1. Antikor

- 6.3.1.1. Company Overview

- 6.3.1.2. Technology Portfolio

- 6.3.1.3. Recent Developments and Future outlook

- 6.3.2. Iksuda Therapeutics

- 6.3.2.1. Company Overview

- 6.3.2.2. Technology Portfolio

- 6.3.2.3. Recent Developments and Future outlook

- 6.3.3. Heidelberg Pharma

- 6.3.3.1. Company Overview

- 6.3.3.2. Financial Information

- 6.3.3.3. Technology Portfolio

- 6.3.3.4. Recent Developments and Future outlook

- 6.3.4. LinXis

- 6.3.4.1. Company Overview

- 6.3.4.2. Technology Portfolio

- 6.3.4.3. Recent Developments and Future outlook

- 6.3.5. NBE-Therapeutics

- 6.3.5.1. Company Overview

- 6.3.5.2. Technology Portfolio

- 6.3.5.3. Recent Developments and Future outlook

- 6.3.1. Antikor

- 6.4. Companies Headquartered in Asia-Pacific and Rest of the World

- 6.4.1. Alteogen

- 6.4.1.1. Company Overview

- 6.4.1.2. Technology Portfolio

- 6.4.1.3. Recent Developments and Future outlook

- 6.5.2. LegoChem Biosciences

- 6.5.2.1. Company Overview

- 6.5.2.2. Technology Portfolio

- 6.5.2.3. Recent Developments and Future outlook

- 6.4.1. Alteogen

7. PATENT ANALYSIS

- 7.1. Chapter Overview

- 7.2. Scope and Methodology

- 7.3. ADC Linker and Conjugation Technologies: Patent Analysis

- 7.3.1. Analysis by Publication Year

- 7.3.2. Analysis by Application Year

- 7.3.3. Analysis by Annual Number of Granted Patents and Patent Applications

- 7.3.4. Analysis by Patent Jurisdiction

- 7.3.5. Analysis by CPC Symbols and Sections

- 7.3.6. Analysis by Type of Applicant

- 7.3.7. Leading Industry Players: Analysis by Number of Patents

- 7.3.8. Leading Non-Industry Players: Analysis by Number of Patents

- 7.3.9. Leading Patent Assignees: Analysis by Number of Patents

- 7.4. Patent Benchmarking Analysis

- 7.4.1. Analysis by Patent Characteristics

- 7.5. Patent Valuation

- 7.6. Leading Patents by Number of Citations

8. PARTNERSHIPS AND COLLABORATIONS

- 8.1. Chapter Overview

- 8.2. Partnership Models

- 8.3. ADC Linker and Conjugation Technologies: Partnerships and Collaborations

- 8.3.1. Analysis by Year of Partnership

- 8.3.2. Analysis by Type of Partnership

- 8.3.3. Analysis by Year of Partnership and Type of Partnership

- 8.3.4. Analysis by Type of Partnership and Generation of Technology

- 8.3.5. Analysis by Type of Partnership and Type of Linker

- 8.3.6. Analysis by Type of Partnership and Type of Conjugation

- 8.3.7. Analysis by Type of Partner

- 8.3.8. Analysis by Year of Partnership and Type of Partner

- 8.3.9. Analysis by Type of Partnership and Type of Partner

- 8.3.10. Analysis by Target Therapeutic Area(s)

- 8.3.11. Most Active Players: Analysis by Number of Partnerships

- 8.3.12. Most Popular Technologies: Analysis by Number of Partnerships

- 8.4. Regional Analysis

- 8.4.1. Local and International Agreements

- 8.4.12. Intercontinental and Intracontinental Agreements

9. BUSINESS MODEL ANALYSIS

- 9.1. Chapter Overview

- 9.2. Business Strategies

- 9.3. ADC Linker and Conjugation Technology Providers: Business Strategy Analysis

- 9.3.1. Analysis by Purpose of Partnership

- 9.3.2. Analysis by Year of Partnership and Purpose of Partnership

- 9.3.3. Analysis by Type of Business Strategy Adopted

- 9.3.4. Analysis by Purpose of Partnership and Type of Business Strategy Adopted

- 9.3.5. Analysis by Upfront and Milestone Payments

- 9.3.6. Analysis by Type of Business Strategy Adopted and Deal Value

- 9.4. Most Active Players: Analysis by Number of Partnerships

- 9.4.1. Synaffix

- 9.4.1.1. Analysis by Purpose of Partnership

- 9.4.1.2. Analysis of Technology Out-Licensing Deals by Deal Value

- 9.4.2. LegoChem Biosciences

- 9.4.2.1. Analysis by Purpose of Partnership

- 9.4.2.2. Analysis by Year of Partnership and Business Strategy Adopted

- 9.4.2.3. Analysis of Technology Out-Licensing Deals by Amount of Investment

- 9.4.3. Catalent Biologics

- 9.4.3.1. Analysis by Purpose of Partnership

- 9.4.3.2. Analysis by Year of Partnership and Business Strategy Adopted

- 9.4.4. Sutro Biopharma

- 9.4.4.1. Analysis by Purpose of Partnership

- 9.4.4.2. Analysis by Year of Partnership and Business Strategy Adopted

- 9.4.4.3. Analysis of Technology Out-Licensing Deals by Deal Value

- 9.4.5. Heidelberg Pharma

- 9.4.5.1. Analysis by Purpose of Partnership

- 9.4.5.2. Analysis by Year of Partnership and Business Strategy Adopted

- 9.4.6. Mersana Therapeutics

- 9.4.6.1. Analysis by Purpose of Partnership

- 9.4.6.2. Analysis by Year of Partnership and Business Strategy Adopted

- 9.4.1. Synaffix

- 9.5. Concluding Remarks

10. LIKELY PARTNERS ANALYSIS

- 10.1. Chapter Overview

- 10.2. Assumptions / Key Parameters

- 10.3. Scope and Methodology

- 10.4. Potential Strategic Partners in North America

- 10.4.1. Most Likely Partners

- 10.4.2. Likely Partners

- 10.4.3. Less Likely Partners

- 10.4.4. Least Likely Partners

- 10.5. Potential Strategic Partners in Europe

- 10.5.1. Most Likely Partners

- 10.5.2. Likely Partners

- 10.5.3. Less Likely Partners

- 10.5.4. Least Likely Partners

- 10.6. Potential Strategic Partners in Asia-Pacific and Rest of the World

- 10.6.1. Most Likely Partners

- 10.6.2. Likely Partners

- 10.6.3. Less Likely Partners

- 10.6.4. Least Likely Partners

11. BRAND POSITIONING ANALYSIS

- 11.1. Chapter Overview

- 11.2. Scope and Methodology

- 11.3. Key Parameters

- 11.4. Brand Positioning Matrix: ADC Conjugation Technology Providers

- 11.4.1. Brand Positioning Matrix: Abzena

- 11.4.2. Brand Positioning Matrix: Ambrx

- 11.4.3. Brand Positioning Matrix: Byondis

- 11.4.4. Brand Positioning Matrix: Creative Biolabs

- 11.4.5. Brand Positioning Matrix: Eisai

- 11.4.6. Brand Positioning Matrix: Mersana Therapeutics

- 11.4.7. Brand Positioning Matrix: Sorrento Therapeutics

- 11.4.8. Brand Positioning Matrix: Tubulis

12. CASE STUDY: ANTIBODY DRUG CONJUGATES

- 12.1. Chapter Overview

- 12.2. Antibody Drug Conjugates: Therapies Pipeline

- 12.2.1. Analysis by Stage of Development

- 12.2.2. Analysis by Target Disease Indication(s)

- 12.2.3. Analysis by Therapeutic Area(s)

- 12.2.4. Analysis by Line of Treatment

- 12.2.5. Analysis by Dosing Frequency

- 12.2.6. Analysis by Type of Therapy

- 12.2.7. Analysis by Target Antigen

- 12.2.8. Analysis by Antibody Isotype

- 12.2.9. Analysis by Type of Payload / Cytotoxin / Warhead

- 12.2.10. Analysis by Type of Payload

- 12.2.11. Analysis by Linker

- 12.2.12. Analysis by Type of Linker (Cleavable / Non-Cleavable)

- 12.3. Antibody Drug Conjugate: List of Developers

- 12.3.1. Analysis by Year of Establishment

- 12.3.2. Analysis by Company Size

- 12.3.3. Analysis by Location of Headquarters

- 12.3.4. Analysis by Company size and Location of Headquarters

- 12.3.5. Most Active Players: Analysis by Number of Therapies

13. MARKET SIZING AND OPPORTUNITY ANALYSIS

- 13.1. Chapter Overview

- 13.2. Key Assumptions

- 13.3. Forecast Methodology

- 13.4. Global ADC Linker and Conjugation Technologies Market, Historical, Base and Forecasted Scenario, till 2035

- 13.4.1. ADC Linker and Conjugation Technologies Market: Distribution by Generation of Technology, Current Year and 2035

- 13.4.1.1. ADC Linker and Conjugation Technologies Market for Third-Generation Technologies till 2035

- 13.4.1.2. ADC Linker and Conjugation Technologies Market for Second-Generation Technologies, till 2035

- 13.4.1.3. ADC Linker and Conjugation Technologies Market for Next-Generation Technologies, till 2035

- 13.4.2. ADC Linker and Conjugation Technologies Market: Distribution by Type of Conjugation, Current Year and 2035

- 13.4.2.1. ADC Linker and Conjugation Technologies Market for Chemical Conjugation, till 2035

- 13.4.2.2. ADC Linker and Conjugation Technologies Market for Chemoenzymatic Conjugation, till 2035

- 13.4.2.3. ADC Linker and Conjugation Technologies Market for Enzymatic Conjugation

- 13.4.3. ADC Linker and Conjugation Technologies Market: Distribution by Type of Linker, Current Year and 2035

- 13.4.3.1. ADC Linker and Conjugation Technologies Market for Cleavable Linkers, till 2035

- 13.4.3.2. ADC Linker and Conjugation Technologies Market for Non-Cleavable Linkers, till 2035

- 13.4.4. ADC Linker and Conjugation Technologies Market: Distribution by Type of Payment Model Adopted, Current Year and 2035

- 13.4.4.1. ADC Linker and Conjugation Technologies Market for Upfront Payments, till 2035

- 13.4.4.2. ADC Linker and Conjugation Technologies Market for Milestone Payments, till 2035

- 13.4.5. ADC Linker and Conjugation Technologies Market: Distribution by Key Geographical Regions, Current Year and 2035

- 13.4.5.1. ADC Linker and Conjugation Technologies Market in North America, till 2035

- 13.4.5.1.1. ADC Linker and Conjugation Technologies Market in North America: Distribution by Generation of Technology, till 2035

- 13.4.5.1.2. ADC Linker and Conjugation Technologies Market in North America: Distribution by Type of Conjugation, till 2035

- 13.4.5.1.3. ADC Linker and Conjugation Technologies Market in North America: Distribution by Type Linker, till 2035

- 13.4.5.2. ADC Linker and Conjugation Technologies Market in Europe, till 2035

- 13.4.5.2.1. ADC Linker and Conjugation Technologies Market in Europe: Distribution by Generation of Technology, till 2035

- 13.4.5.2.2. ADC Linker and Conjugation Technologies Market in Europe: Distribution by Type of Conjugation, till 2035

- 13.4.5.2.3. ADC Linker and Conjugation Technologies Market in Europe: Distribution by Type Linker, till 2035

- 13.4.5.3. ADC Linker and Conjugation Technologies Market in Asia-Pacific and Rest of the World, till 2035

- 13.4.5.3.1. ADC Linker and Conjugation Technologies Market in Asia-Pacific and Rest of the World: Distribution by Generation of Technology, till 2035

- 13.4.5.3.2. ADC Linker and Conjugation Technologies Market in Asia-Pacific and Rest of the World: Distribution by Type of Conjugation, till 2035

- 13.4.5.3.3. ADC Linker and Conjugation Technologies Market in Asia-Pacific and Rest of the World: Distribution by Type of Linker, till 2035

- 13.4.5.1. ADC Linker and Conjugation Technologies Market in North America, till 2035

- 13.4.1. ADC Linker and Conjugation Technologies Market: Distribution by Generation of Technology, Current Year and 2035

- 13.5. Concluding Remarks

14. EXECUTIVE INSIGHTS

- 14.1. Chapter Overview

- 14.2. Abzena

- 14.2.1. Company Snapshot

- 14.2.2. Interview Transcript: Saptarshi Ghosh (Scientist II)

- 14.3. MedLink Therapeutics

- 14.3.1. Company Snapshot

- 14.3.2. Interview Transcript: Jiaqiang Cai (Co-Founder and Chief Scientific Officer)

- 14.4. Merck KGaA

- 14.4.1. Company Snapshot

- 14.4.2. Interview Transcript: Kai Uhrig (Head of Strategy and Business Development)

- 14.5. Singzyme

- 14.5.1. Company Snapshot

- 14.5.2. Interview Transcript: Cedric Lizin (Board Member)

- 14.6. Ajinomoto

- 14.6.1. Company Snapshot

- 14.6.2. Interview Transcript: Okuzumi-Tatsuya (General Manager, Research and Development), Brian Mendelsohn (Director of ADC Process Development and Tech Transfer)

- 14.7. Eucodis Bioscience

- 14.7.1. Company Snapshot

- 14.7.2. Interview Transcript: Jan Modregger (Head of Research and Development)

- 14.8. NBE-Therapeutics

- 14.8.1. Company Snapshot

- 14.8.2. Interview Transcript: Wouter Verhoeven (Former Chief Business Officer)

- 14.9. Shanghai Miracogen

- 14.9.1. Company Snapshot

- 14.9.2. Interview Transcript: Mary Chaohong Hu (Chief Executive Officer)

- 14.10. Synaffix

- 14.10.1. Company Snapshot

- 14.10.2. Interview Transcript: Floris van Delft (Chief Scientific Officer)

15. CONCLUDING REMARKS

16. APPENDIX 1: TABULATED DATA

17. APPENDIX 2: LIST OF COMPANIES AND ORGANIZATIONS

List of Tables

- Table 3.1 Commonly Used Cytotoxins in ADC Therapeutics

- Table 3.2 OEL Bands: Guidelines by SafeBridge Consultants

- Table 4.1 ADC Linker and Conjugation Technologies: Overall Market Landscape

- Table 4.2 ADC Conjugation Technologies: Information on Generation of Technology, Site-Specificity, Type of Conjugation and Drug Antibody Ratio

- Table 4.3 ADC Conjugation Technologies: Information on Number of Steps Involved, Compatible Linker, Conjugation Chemistry and Conjugation Site

- Table 4.4 ADC Linker and Linker-Payload Technologies: Information on Type of Linker and Linker Name

- Table 4.5 ADC Linker and Conjugation Technology Providers

- Table 4.6 ADC Conjugation Technologies Service Providers

- Table 6.1 ADC Linkers and Conjugation Technologies: List of Profiled Companies

- Table 6.2 Ambrx: Company Overview

- Table 6.3 Ambrx: ADC Linkers and Conjugation Technologies Portfolio

- Table 6.4 Ambrx: Antibody Drug Conjugates Portfolio

- Table 6.5 Ambrx: Recent Developments and Future Outlook

- Table 6.6 Catalent Biologics: Company Overview

- Table 6.7 Catalent Biologics: ADC Linkers and Conjugation Technologies Portfolio

- Table 6.8 Catalent Biologics: Antibody Drug Conjugates Portfolio

- Table 6.9 Catalent Biologics: Recent Developments and Future Outlook

- Table 6.10 Mersana Therapeutics: Company Overview

- Table 6.11 Mersana Therapeutics: ADC Linkers and Conjugation Technologies Portfolio

- Table 6.12 Mersana Therapeutics: Antibody Drug Conjugates Portfolio

- Table 6.13 Mersana Therapeutics: Recent Developments and Future Outlook

- Table 6.14 Seagen: Company Overview

- Table 6.15 Seagen: ADC Linkers and Conjugation Technologies Portfolio

- Table 6.16 Seagen: Antibody Drug Conjugates Portfolio

- Table 6.17 Seagen: Recent Developments and Future Outlook

- Table 6.18 Sutro Biopharma: Company Overview

- Table 6.19 Sutro Biopharma: ADC Linkers and Conjugation Technologies Portfolio

- Table 6.20 Sutro Biopharma: Antibody Drug Conjugates Portfolio

- Table 6.21. Sutro Biopharma: Recent Developments and Future Outlook

- Table 6.22 Antikor: Company Overview

- Table 6.23 Antikor: ADC Conjugation Technology Portfolio

- Table 6.24 Antikor: Antibody Drug Conjugates Portfolio

- Table 6.25 Antikor: Recent Developments and Future Outlook

- Table 6.26 Iksuda Therapeutics: Company Overview

- Table 6.27 Iksuda Therapeutics: ADC Linkers and Conjugation Technologies Portfolio

- Table 6.28 Iksuda Therapeutics: Antibody Drug Conjugates Portfolio

- Table 6.29 Heidelberg Pharma: Company Overview

- Table 6.30 Heidelberg Pharma: ADC Linkers and Conjugation Technologies Portfolio

- Table 6.31 Heidelberg Pharma: Antibody Drug Conjugates Portfolio

- Table 6.32 Heidelberg Pharma: Recent Developments and Future Outlook

- Table 6.33 LinXis: Company Overview

- Table 6.34 LinXis: ADC Conjugation Technology Portfolio

- Table 6.35 NBE-Therapeutics: Company Overview

- Table 6.36 NBE-Therapeutics: ADC Linkers and Conjugation Technologies Portfolio

- Table 6.37 NBE-Therapeutics: Antibody Drug Conjugates Portfolio

- Table 6.38 Alteogen: Company Overview

- Table 6.39 Alteogen: ADC Linkers and Conjugation Technologies Portfolio

- Table 6.40 Alteogen: Antibody Drug Conjugates Portfolio

- Table 6.41 LegoChem Biosciences: Company Overview

- Table 6.42 LegoChem Biosciences: ADC Linkers and Conjugation Technologies Portfolio

- Table 6.43 LegoChem Biosciences: Antibody Drug Conjugates Portfolio

- Table 6.44 LegoChem Biosciences: Recent Developments and Future Outlook

- Table 7.1 Patent Analysis: Top CPC Sections

- Table 7.2 Patent Analysis: Top CPC Symbols

- Table 7.3 Patent Analysis: Top CPC Codes

- Table 7.4 Patent Analysis: Summary of Benchmarking Analysis

- Table 7.5 Patent Analysis: Categorization based on Weighted Valuation Scores

- Table 7.6 Patent Portfolio: List of Leading Patents (by Number of Citations)

- Table 8.1 ADC Linker and Conjugation Technologies: Partnerships and Collaborations

- Table 8.2 ADC Linker and Conjugation Technologies: Partnerships and Collaborations, Information on Type of Partner, Therapeutic Area(s) and Type of Agreement (Region-wise and Geography-wise)

- Table 9.1 ADC Linker and Conjugation Technologies: Business Model Analysis

- Table 10.1 North America: Most Likely Partners for ADC Linker and Conjugation Technology Providers

- Table 10.2 North America: Likely Partners for ADC Linker and Conjugation Technology Providers

- Table 10.3 North America: Less Likely Partners for ADC Linker and Conjugation Technology Providers

- Table 10.4 North America: Least Likely Partners for ADC Linker and Conjugation Technology Providers

- Table 10.5 Europe: Most Likely Partners for ADC Linker and Conjugation Technology Providers

- Table 10.6 Europe: Likely Partners for ADC Linker and Conjugation Technology Providers

- Table 10.7 Europe: Less Likely Partners for ADC Linker and Conjugation Technology Providers

- Table 10.8 Europe: Least Likely Partners for ADC Linker and Conjugation Technology Providers

- Table 10.9 Asia-Pacific and Rest of the World: Most Likely Partners for ADC Linker and Conjugation Technology Providers

- Table 10.10 Asia-Pacific and Rest of the World: Likely Partners for ADC Linker and Conjugation Technology Providers

- Table 10.11 Asia-Pacific and Rest of the World: Less Likely Partners for ADC Linker and Conjugation Technology Providers

- Table 10.12 Asia-Pacific and Rest of the World: Least Likely Partners for ADC Linker and Conjugation Technology Providers

- Table 12.1 Antibody Drug Conjugates: Information on Drug Candidates, Developer(s), Stage of Development, Target Disease Indication(s) and Therapeutics Area(s)

- Table 12.2 Antibody Drug Conjugates: Information on Drug Candidates, Line of Treatment, Dosage Frequency, Type of Therapy, Target Antigen and Antibody Isotype

- Table 12.3 Antibody Drug Conjugates: Information on Drug Candidates, Payload / Cytotoxin / Warhead, Type of Payload, Linker and Type of Linker (Cleavable and Non-Cleavable)

- Table 12.4 Antibody Drug Conjugate Developers: Information on Year of Establishment, Company Size, Location of Headquarters

- Table 13.1 Technology Licensing Deal: Tranches of Milestone Payments

- Table 13.2 ADC Linker and Conjugation Technologies: Average Upfront Payments and Average Milestone Payments (USD Million)

- Table 14.1 Abzena: Company Snapshot

- Table 14.2 MedLink Therapeutics: Company Snapshot

- Table 14.3 Merck KGaA: Company Snapshot

- Table 14.4 Singzyme: Company Snapshot

- Table 14.5 Ajinomoto: Company Snapshot

- Table 14.6 Eucodis Bioscience: Company Snapshot

- Table 14.7 Shanghai Miracogen: Company Snapshot

- Table 14.8 NBE-Therapeutics: Company Snapshot

- Table 14.9 Synaffix: Company Snapshot

- Table 16.1 ADC Linker and Conjugation Technologies: Distribution by Type of Technology

- Table 16.2 ADC Linker and Conjugation Technologies: Distribution by Availability of Licensing

- Table 16.3 ADC Conjugation Technologies: Distribution by Generation of Technology

- Table 16.4 ADC Conjugation Technologies: Distribution by Site Specificity

- Table 16.5 ADC Conjugation Technologies: Distribution by Type of Conjugation

- Table 16.6 ADC Conjugation Technologies: Distribution by Drug Antibody Ratio

- Table 16.7 ADC Conjugation Technologies: Distribution by Compatible Linker

- Table 16.8 ADC Conjugation Technologies: Distribution by Conjugation Chemistry

- Table 16.9 ADC Conjugation Technologies: Distribution by Conjugation Site

- Table 16.10 ADC Linker and ADC Linker-Payload Technologies: Distribution by Type of Linker

- Table 16.11 ADC Linker and Conjugation Technology Providers: Distribution by Year of Establishment

- Table 16.12 ADC Linker and Conjugation Technology Providers: Distribution by Company Size

- Table 16.13 ADC Linker and Conjugation Technology Providers: Distribution by Location of Headquarters

- Table 16.14 ADC Linker and Conjugation Technology Providers: Distribution by Year of Establishment and Location of Headquarters

- Table 16.15 ADC Linker and Conjugation Technology Providers: Distribution by Company Size and Location of Headquarters

- Table 16.16 Ambrx: Annual Revenues, FY 2020 Onwards (USD Million)

- Table 16.17 Mersana Therapeutics: Annual Revenues, FY 2018 Onwards (USD Million)

- Table 16.18 Seagen: Revenues, FY 2018 Onwards (USD Billion)

- Table 16.19 Sutro Biopharma: Revenues, FY 2018 Onwards (USD Million)

- Table 16.20 Heidelberg Pharma: Annual Revenues, FY 2018 Onwards (EUR Million)

- Table 16.21 Catalent Biologics: Revenues, FY 2018 Onwards (USD Billion)

- Table 16.22 Patent Analysis: Distribution by Type of Patent

- Table 16.23 Patent Analysis: Cumulative Distribution by Publication Year

- Table 16.24 Patent Analysis: Cumulative Distribution by Application Year

- Table 16.25 Patent Analysis: Distribution by Patent Type and Publication Year

- Table 16.26 Patent Analysis: Distribution by Patent Jurisdiction

- Table 16.27 Patent Analysis: Distribution by CPC Symbols and Sections

- Table 16.28 Patent Analysis: Cumulative Year-wise Distribution by Type of Applicant

- Table 16.29 Leading Industry Players: Distribution by Number of Patents

- Table 16.30 Leading Non-Industry Players: Distribution by Number of Patents

- Table 16.31 Leading Individual Assignees: Distribution by Number of Patents

- Table 16.32 Patent Benchmarking Analysis: Distribution of Leading Industry Player by Patent Characteristics (CPC Codes)

- Table 16.33 Patent Analysis: Distribution by Patent Age

- Table 16.34 ADC Linker and Conjugation Technologies: Patent Valuation

- Table 16.35 Partnerships and Collaborations: Distribution by Year of Partnership

- Table 16.36 Partnerships and Collaborations: Distribution by Type of Partnership

- Table 16.37 Partnerships and Collaborations: Distribution by Year of Partnership and Type of Partnership

- Table 16.38 Partnerships and Collaborations: Distribution by Type of Partnership and Generation of Technology

- Table 16.39 Partnerships and Collaborations: Distribution by Type of Partnership and Type of Linker

- Table 16.40 Partnerships and Collaborations: Distribution by Type of Partnership and Type of Conjugation

- Table 16.41 Partnerships and Collaborations: Distribution by Type of Partner

- Table 16.42 Partnerships and Collaborations: Distribution by Year of Partnership and Type of Partner

- Table 16.43 Partnerships and Collaborations: Distribution by Type of Partnership and Type of Partner

- Table 16.44 Partnerships and Collaborations: Distribution by Therapeutic Area(s)

- Table 16.45 Most Active Players: Distribution by Number of Partnerships

- Table 16.46 Most Popular Technologies: Distribution by Number of Partnerships

- Table 16.47 Partnership and Collaborations: Local and International Agreements

- Table 16.48 Partnerships and Collaborations: Intercontinental and Intracontinental Agreements

- Table 16.49 Business Models Analysis: Distribution by Purpose of Partnership

- Table 16.50 Business Models Analysis: Distribution by Year of Partnership and Purpose of Partnership

- Table 16.51 Business Models Analysis: Distribution by Type of Business Strategy Adopted

- Table 16.52 Business Models Analysis: Distribution by Purpose of Partnership and Type of Business Strategy Adopted

- Table 16.53 Business Models Analysis: Distribution by Upfront and Milestone Payments

- Table 16.54 Business Models Analysis: Distribution by Type of Business Model Adopted and Deal Value

- Table 16.55 Synaffix: Distribution by Purpose of Partnership

- Table 16.56 Synaffix: Technology Out-Licensing Deals by Deal Value

- Table 16.57 LegoChem Biosciences: Distribution by Purpose of Partnership

- Table 16.58 LegoChem Biosciences: Distribution by Year of Partnership and Business Strategy Adopted

- Table 16.59 LegoChem Biosciences: Distribution of Technology Out-Licensing Deals by Deal Value

- Table 16.60 Catalent Biologics: Distribution by Purpose of Partnership

- Table 16.61 Catalent Biologics: Distribution by Year of Partnership and Business Strategy Adopted

- Table 16.62 Sutro Biopharma: Distribution by Purpose of Partnership

- Table 16.63 Sutro Biopharma: Distribution by Year of Partnership and Business Strategy Adopted

- Table 16.64 Sutro Biopharma: Distribution of Technology Out-Licensing Deals by Deal Value

- Table 16.65 Heidelberg Pharma: Distribution by Purpose of Partnership

- Table 16.66 Heidelberg Pharma: Distribution by Year of Partnership and Business Strategy Adopted

- Table 16.67 Mersana Therapeutics: Distribution by Purpose of Partnership

- Table 16.68 Mersana Therapeutics: Distribution by Year of Partnership and Business Strategy Adopted

- Table 16.69 Antibody Drug Conjugates: Distribution by Stage of Development

- Table 16.70 Antibody Drug Conjugates: Distribution by Target Disease Indication

- Table 16.71 Antibody Drug Conjugates: Distribution by Therapeutic Area(s)

- Table 16.72 Antibody Drug Conjugates: Distribution by Line of Treatment

- Table 16.73 Antibody Drug Conjugates: Distribution by Dosing Frequency

- Table 16.74 Antibody Drug Conjugates: Distribution by Type of Therapy

- Table 16.75 Antibody Drug Conjugates: Distribution by Target Antigen

- Table 16.76 Antibody Drug Conjugates: Distribution by Antibody Isotype

- Table 16.77 Antibody Drug Conjugates: Distribution by Type of Cytotoxin / Warhead

- Table 16.78 Antibody Drug Conjugates: Distribution by Type of Payload

- Table 16.79 Antibody Drug Conjugates: Distribution by Linker

- Table 16.80 Antibody Drug Conjugates: Distribution by Type of Linker

- Table 16.81 Antibody Drug Conjugate Developers: Distribution by Year of Establishment

- Table 16.82 Antibody Drug Conjugates Developers: Distribution by Company Size

- Table 16.83 Antibody Drug Conjugates Developers: Distribution by Location of Headquarters

- Table 16.84 Antibody Drug Conjugates Developers: Distribution by Company Size and Location of Headquarters

- Table 16.85 Most Active Players: Distribution by Number of Antibody Drug Conjugates

- Table 16.86 Global ADC Linker and Conjugation Technologies Market, Conservative, Base and Optimistic Scenarios, till 2035 (USD Million)

- Table 16.87 ADC Linker and Conjugation Technologies Market: Distribution by Generation of Technology, Current Year and 2035

- Table 16.88 ADC Linker and Conjugation Technologies Market for Third-Generation Technologies, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.89 ADC Linker and Conjugation Technologies Market for Second-Generation Technologies, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.90 ADC Linker and Conjugation Technologies Market for Next-Generation Technologies, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.91 ADC Linker and Conjugation Technologies Market: Distribution by Type of Conjugation, Current Year and 2035

- Table 16.92 ADC Linker and Conjugation Technologies Market for Chemical Conjugation, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.93 ADC Linker and Conjugation Technologies Market for Chemoenzymatic Conjugation, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.94 ADC Linker and Conjugation Technologies Market for Enzymatic Conjugation, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.95 ADC Linker and Conjugation Technologies Market: Distribution by Type of Linker, Current Year and 2035

- Table 16.96 ADC Linker and Conjugation Technologies Market for Cleavable Linkers, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.97 ADC Linker and Conjugation Technologies Market for Non-Cleavable Linkers, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.98 ADC Linker and Conjugation Technologies Market: Distribution by Type of Payment Model Adopted, Current Year and 2035

- Table 16.99 ADC Linker and Conjugation Technologies Market for Upfront Payments, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.100 ADC Linker and Conjugation Technologies Market for Milestone Payments, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.101 ADC Linker and Conjugation Technologies Market: Distribution by Key Geographical Regions, Current Year and 2035

- Table 16.102 ADC Linker and Conjugation Technologies Market in North America, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.103 ADC Linker and Conjugation Technologies Market in North America: Distribution by Generation of Technology, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.104 ADC Linker and Conjugation Technologies Market in North America: Distribution by Type of Conjugation, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.105 ADC Linker and Conjugation Technologies Market in North America: Distribution by Type Linker till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.106 ADC Linker and Conjugation Technologies Market in Europe, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.107 ADC Linker and Conjugation Technologies Market in Europe: Distribution by Generation of Technology, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.108 ADC Linker and Conjugation Technologies Market in Europe: Distribution by Type of Conjugation, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.109 ADC Linker and Conjugation Technologies Market in Europe: Distribution by Type Linker till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.110 ADC Linker and Conjugation Technologies Market in Asia-Pacific and Rest of the World, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.111 ADC Linker and Conjugation Technologies Market in Asia-Pacific and Rest of the World: Distribution by Generation of Technology, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.112 ADC Linker and Conjugation Technologies Market in Asia-Pacific and Rest of the World: Distribution by Type of Conjugation, till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

- Table 16.113 ADC Linker and Conjugation Technologies Market in Asia-Pacific and Rest of the World: Distribution by Type Linker till 2035, Conservative, Base and Optimistic Scenarios (USD Million)

List of Figures

- Figure 2.1 Executive Summary: Current Market Landscape of ADC Linker and Conjugation Technologies

- Figure 2.2 Executive Summary: Patent Analysis

- Figure 2.3 Executive Summary: Partnerships and Collaborations

- Figure 2.4 Executive Summary: Business Model Analysis

- Figure 2.5 Executive Summary: Case Study on ADC Therapeutics

- Figure 2.6 Executive Summary: Market Sizing and Opportunity Analysis

- Figure 3.1 Components of ADCs

- Figure 3.2 Types of Linkers

- Figure 4.1 ADC Linker and Conjugation Technologies: Distribution by Type of Technology

- Figure 4.2 ADC Linker and Conjugation Technologies: Distribution by Availability of Licensing

- Figure 4.3 ADC Conjugation Technologies: Distribution by Generation of Technology

- Figure 4.4 ADC Conjugation Technologies: Distribution by Site Specificity

- Figure 4.5 ADC Conjugation Technologies: Distribution by Type of Conjugation

- Figure 4.6 ADC Conjugation Technologies: Distribution by Drug Antibody Ratio

- Figure 4.7 ADC Conjugation Technologies: Distribution by Compatible Linker

- Figure 4.8 ADC Conjugation Technologies: Distribution by Conjugation Chemistry

- Figure 4.9 ADC Conjugation Technologies: Distribution by Conjugation Site

- Figure 4.10 ADC Linker and ADC Linker-Payload Technologies: Distribution by Type of Linker

- Figure 4.11 ADC Linker and Conjugation Technology Providers: Distribution by Year of Establishment

- Figure 4.12 ADC Linker and Conjugation Technology Providers: Distribution by Company Size

- Figure 4.1. ADC Linker and Conjugation Technology Providers: Distribution by Location of Headquarters

- Figure 4.14 ADC Linker and Conjugation Technology Providers: Distribution by Year of Establishment and Location of Headquarters

- Figure 4.15 ADC Linker and Conjugation Technology Providers: Distribution by Company Size and Location of Headquarters

- Figure 5.1 Technology Competitiveness Analysis: Distribution of Technologies Offered by Small Companies

- Figure 5.2 Technology Competitiveness Analysis: Distribution of Technologies Offered by Mid-sized Companies

- Figure 5.3 Technology Competitiveness Analysis: Distribution of Technologies Offered by Large Companies

- Figure 6.1 Ambrx: Annual Revenues, FY 2020 Onwards (USD Million)

- Figure 6.2 Catalent Biologics: Revenues, FY 2018 Onwards (USD Billion)

- Figure 6.3 Mersana Therapeutics: Annual Revenues, FY 2018 Onwards (USD Million)

- Figure 6.4 Seagen: Revenues, FY 2018 Onwards (USD Billion)

- Figure 6.5 Sutro Biopharma: Revenues, FY 2018 Onwards (USD Million)

- Figure 6.6 Heidelberg Pharma: Annual Revenues, FY 2018 Onwards (EUR Million)

- Figure 7.1 Patent Analysis: Distribution by Type of Patent

- Figure 7.2 Patent Analysis: Cumulative Distribution by Publication Year

- Figure 7.3 Patent Analysis: Cumulative Distribution by Application Year

- Figure 7.4 Patent Analysis: Year-wise Distribution of Granted Patents and Patent Applications

- Figure 7.5 Patent Analysis: Distribution by Patent Jurisdiction

- Figure 7.6 Patent Analysis: Distribution by CPC Symbols and Sections

- Figure 7.7 Patent Analysis: Cumulative Year-wise Distribution by Type of Applicant

- Figure 7.9 Leading Industry Players: Distribution by Number of Patents

- Figure 7.10 Leading Non-Industry Players: Distribution by Number of Patents

- Figure 7.11 Leading Patent Assignees: Distribution by Number of Patents

- Figure 7.12 Patent Benchmarking Analysis: Distribution of Leading Industry Player by Patent Characteristics (CPC Codes)

- Figure 7.13 Patent Analysis: Distribution by Patent Age

- Figure 7.14 ADC Linker and Conjugation Technologies: Patent Valuation

- Figure 8.1 Partnerships and Collaborations: Distribution by Year of Partnership

- Figure 8.2 Partnerships and Collaborations: Distribution by Type of Partnership

- Figure 8.3 Partnerships and Collaborations: Distribution by Year of Partnership and Type of Partnership

- Figure 8.4 Partnerships and Collaborations: Distribution by Type of Partnership and Generation of Technology

- Figure 8.5 Partnerships and Collaborations: Distribution by Type of Partnership and Type of Linker

- Figure 8.6 Partnerships and Collaborations: Distribution by Type of Partnership and Type of Conjugation

- Figure 8.7 Partnerships and Collaborations: Distribution by Type of Partner

- Figure 8.8 Partnerships and Collaborations: Distribution by Year of Partnership and Type of Partner

- Figure 8.9 Partnerships and Collaborations: Distribution by Type of Partnership and Type of Partner

- Figure 8.10 Partnerships and Collaborations: Distribution by Therapeutic Area(s)

- Figure 8.11 Most Active Players: Distribution by Number of Partnerships

- Figure 8.12 Most Popular Technologies: Distribution by Number of Partnerships

- Figure 8.13 Partnerships and Collaborations: Local and International Agreements

- Figure 8.14 Partnerships and Collaborations: Intercontinental and Intracontinental Agreements

- Figure 9.1 Business Models Analysis: Distribution by Purpose of Partnership

- Figure 9.2 Business Models Analysis: Year-wise Distribution by Purpose of Partnership

- Figure 9.3 Business Models Analysis: Distribution by Type of Business Strategy Adopted

- Figure 9.4 Business Models Analysis: Distribution by Purpose of Partnership and Type of Business Strategy Adopted

- Figure 9.5 Business Models Analysis: Distribution by Upfront and Milestone Payments

- Figure 9.6 Business Models Analysis: Distribution by Type of Business Strategy Adopted and Deal Value

- Figure 9.7 Synaffix: Distribution by Purpose of Partnership

- Figure 9.8 Synaffix: Distribution of Technology Out-Licensing Deals by Deal Value

- Figure 9.9 LegoChem Biosciences: Distribution by Purpose of Partnership

- Figure 9.10 LegoChem Biosciences: Distribution by Year of Partnership and Business Strategy Adopted

- Figure 9.11 LegoChem Biosciences: Distribution of Technology Out-Licensing Deals by Deal Value

- Figure 9.12 Catalent Biologics: Distribution by Purpose of Partnership

- Figure 9.13 Catalent Biologics: Distribution by Year of Partnership and Business Strategy Adopted

- Figure 9.14 Sutro Biopharma: Distribution by Purpose of Partnership

- Figure 9.15 Sutro Biopharma: Distribution by Year of Partnership and Business Strategy Adopted

- Figure 9.16 Sutro Biopharma: Distribution of Technology Out-Licensing Deals by Deal Value

- Figure 9.17 Heidelberg Pharma: Distribution by Purpose of Partnership

- Figure 9.18 Heidelberg Pharma: Distribution by Year of Partnership and Business Strategy Adopted

- Figure 9.19 Mersana Therapeutics: Distribution by Purpose of Partnership

- Figure 9.20 Mersana Therapeutics: Distribution by Year of Partnership and Business Strategy Adopted

- Figure 11.1 Brand Positioning Analysis: Competitive Advantage

- Figure 11.2 Brand Positioning Analysis: Reasons to Believe

- Figure 11.3 Brand Positioning Matrix: Abzena

- Figure 11.4 Brand Positioning Matrix: Ambrx

- Figure 11.5 Brand Positioning Matrix: Byondis

- Figure 11.6. Brand Positioning Matrix: Creative Biolabs

- Figure 11.7 Brand Positioning Matrix: Eisai

- Figure 11.8 Brand Positioning Matrix: Mersana Therapeutics

- Figure 11.9 Brand Positioning Matrix: Sorrento Therapeutics

- Figure 11.10 Brand Positioning Matrix: Tubulis

- Figure 12.1 Antibody Drug Conjugates: Distribution by Stage of Development

- Figure 12.2 Antibody Drug Conjugates: Distribution by Target Disease Indication(s)

- Figure 12.3 Antibody Drug Conjugates: Distribution by Therapeutic Area(s)

- Figure 12.4 Antibody Drug Conjugates: Distribution by Line of Treatment

- Figure 12.5 Antibody Drug Conjugates: Distribution by Dosing Frequency

- Figure 12.6 Antibody Drug Conjugates: Distribution by Type of Therapy

- Figure 12.7 Antibody Drug Conjugates: Distribution by Target Antigen

- Figure 12.8 Antibody Drug Conjugates: Distribution by Antibody Isotype

- Figure 12.9 Antibody Drug Conjugates: Distribution by Type of Payload / Cytotoxin / Warhead

- Figure 12.10 Antibody Drug Conjugates: Distribution by Type of Payload

- Figure 12.11 Antibody Drug Conjugates: Distribution by Linker

- Figure 12.12 Antibody Drug Conjugates: Distribution by Type of Linker

- Figure 12.13 Antibody Drug Conjugate Developers: Distribution by Year of Establishment

- Figure 12.14 Antibody Drug Conjugates Developers: Distribution by Company Size

- Figure 12.15 Antibody Drug Conjugates Developers: Distribution by Location of Headquarters

- Figure 12.16 Antibody Drug Conjugates Developers: Distribution by Company Size and Location of Headquarters

- Figure 12.17 Most Active Players: Distribution by Number of Therapies

- Figure 13.1 Licensing Agreements: Distribution of Financial Components

- Figure 13.2 Technology Licensing Deal: Payment Structure

- Figure 13.3 Global ADC Linker and Conjugation Technologies Market, Historical, Base and Forecasted Scenario, till 2035 (USD Million)

- Figure 13.4 ADC Linker and Conjugation Technologies Market: Distribution by Generation of Technology, Current Year and 2035

- Figure 13.5 ADC Linker and Conjugation Technologies Market for Third-Generation Technologies, till 2035 (USD Million)

- Figure 13.6 ADC Linker and Conjugation Technologies Market for Second-Generation Technologies, till 2035 (USD Million)

- Figure 13.7 ADC Linker and Conjugation Technologies Market for Next-Generation Technologies, till 2035 (USD Million)

- Figure 13.8 ADC Linker and Conjugation Technologies Market: Distribution by Type of Conjugation, Current Year and 2035

- Figure 13.9 ADC Linker and Conjugation Technologies Market for Chemical Conjugation, till 2035 (USD Million)

- Figure 13.10 ADC Linker and Conjugation Technologies Market for Chemoenzymatic Conjugation, till 2035 (USD Million)

- Figure 13.11 ADC Linker and Conjugation Technologies Market for Enzymatic Conjugation, till 2035 (USD Million)

- Figure 13.12 ADC Linker and Conjugation Technologies Market: Distribution by Type of Linker, Current Year and 2035

- Figure 13.13 ADC Linker and Conjugation Technologies Market for Cleavable Linkers, till 2035 (USD Million)

- Figure 13.14 ADC Linker and Conjugation Technologies Market for Non-Cleavable Linkers, till 2035 (USD Million)

- Figure 13.15 ADC Linker and Conjugation Technologies Market: Distribution by Type of Payment Model Adopted, Current Year and 2035

- Figure 13.16 ADC Linker and Conjugation Technologies Market for Upfront Payments, till 2035 (USD Million)

- Figure 13.17 ADC Linker and Conjugation Technologies Market for Milestone Payments, till 2035 (USD Million)

- Figure 13.18 ADC Linker and Conjugation Technologies Market: Distribution by Key Geographical Regions, Current Year and 2035

- Figure 13.19 ADC Linker and Conjugation Technologies Market in North America, till 2035 (USD Million)

- Figure 13.20 ADC Linker and Conjugation Technologies Market in North America: Distribution by Generation of Technology, till 2035 (USD Million)

- Figure 13.21 ADC Linker and Conjugation Technologies Market in North America: Distribution by Type of Conjugation, till 2035 (USD Million)

- Figure 13.22 ADC Linker and Conjugation Technologies Market in North America: Distribution by Type Linker, till 2035 (USD Million)

- Figure 13.23 ADC Linker and Conjugation Technologies Market in Europe, till 2035 (USD Million)

- Figure 13.24 ADC Linker and Conjugation Technologies Market in Europe: Distribution by Generation of Technology, till 2035 (USD Million)

- Figure 13.25 ADC Linker and Conjugation Technologies Market in Europe: Distribution by Type of Conjugation, till 2035 (USD Million)

- Figure 13.26 ADC Linker and Conjugation Technologies Market in Europe: Distribution by Type Linker, till 2035 (USD Million)

- Figure 13.27 ADC Linker and Conjugation Technologies Market in Asia-Pacific and Rest of the World, till 2035 (USD Million)

- Figure 13.28 ADC Linker and Conjugation Technologies Market in Asia-Pacific and Rest of the World: Distribution by Generation of Technology, till 2035 (USD Million)

- Figure 13.29 ADC Linker and Conjugation Technologies Market in Asia-Pacific and Rest of the World: Distribution by Type of Conjugation, till 2035 (USD Million)

- Figure 13.30 ADC Linker and Conjugation Technologies Market in Asia-Pacific and Rest of the World: Distribution by Type Linker, till 2035 (USD Million)

- Figure 15.1 Concluding Remarks: Current Market Landscape of ADC Linker and Conjugation Technologies

- Figure 15.2 Concluding Remarks: Current Market Landscape of ADC Linker and Conjugation Technology Providers

- Figure 15.3 Concluding Remarks: Patent Analysis

- Figure 15.4 Concluding Remarks: Partnerships and Collaborations

- Figure 15.5 Concluding Remarks: Business Model Analysis

- Figure 15.6 Concluding Remarks: Case Study on Antibody Drug Conjugates

- Figure 15.7 Concluding Remarks: Market Sizing and Opportunity Analysis