Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693836

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693836

Asia-Pacific Polycarbonate (PC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

PUBLISHED:

PAGES: 183 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

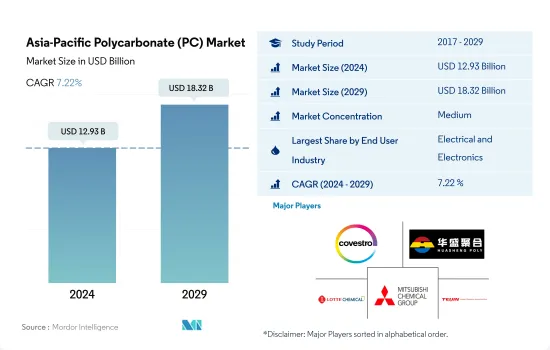

The Asia-Pacific Polycarbonate (PC) Market size is estimated at 12.93 billion USD in 2024, and is expected to reach 18.32 billion USD by 2029, growing at a CAGR of 7.22% during the forecast period (2024-2029).

Electrical and electronics industry to maintain its dominance

- Polycarbonates are widely utilized in various industries due to their versatile and durable nature. They find applications in refrigerators, agricultural houses, industrial and public buildings, facades, surgical instruments, drug delivery systems, hemodialysis membranes, blood reservoirs, and blood filters. The electrical and electronics industry has been the largest consumer of polycarbonate in the region, and it accounted for over 45% of the market share in 2022.

- Between 2017 and 2019, polycarbonate demand experienced steady growth, with Y-o-Y rates of 5.14% and 3.53%, respectively. The increasing production in the electronics industry primarily drove this growth.

- In 2020, the COVID-19 pandemic led to operational, travel, and trade restrictions, resulting in a decline in the demand for polycarbonates by 3.71% compared to the previous year. The automotive and industrial machinery industries were particularly affected, experiencing declines of 12.52% and 16.65% in their 2019 volumes, respectively. However, as the restrictions eased, the demand for polycarbonates gradually recovered, with China and India playing a significant role in driving the growth.

- The growing trend of substituting traditional acrylics and glass with polycarbonates is expected to drive the demand for the material in the forecast period. Among all end-user industries in the Asia-Pacific region, the electrical and electronics industry in India is projected to witness the highest growth, with a CAGR of 7.63% in terms of volume during the forecast period. Overall, the regional demand for polycarbonates is expected to record a CAGR of 5.66% in volume terms and 7.22% in value terms throughout the forecast period.

China to maintain its dominance both in terms of volume and value

- The Asia-Pacific region is the largest consumer of polycarbonates globally, occupying a share of over 63.07% in 2022. In the Asia-Pacific region, polycarbonates find various applications in the electrical and electronics, automotive, aerospace components manufacturing, and healthcare devices manufacturing industries.

- During 2017-2019, the demand for polycarbonates witnessed steady growth, mainly driven by the rapid growth in the plastic packaging industry in countries like China and India. In 2020, various restraining factors, like worker unavailability and raw material shortages caused by operational and trade restrictions during the pandemic, severely affected various end-user industries, thereby negatively affecting the polycarbonate demand in the region. Among all countries, the polycarbonate demand in Australia was affected severely. In 2020, the country's Y-o-Y demand volume declined by 40.96%, whereas the regional Y-o-Y decline was 3.71%.

- In 2021, as the restrictions eased, the polycarbonate demand rose back to its pre-pandemic level. This growth was majorly driven by the rapid growth in industrial activities in countries like India. This growth trend is expected to continue throughout the forecast period, with India witnessing the highest growth in polycarbonate demand among all countries. Overall, the polycarbonate demand in the Asia-Pacific region is expected to record a CAGR of 5.60% (in volume) during the forecast period.

Asia-Pacific Polycarbonate (PC) Market Trends

Rapid growth in ASEAN countries to foster electronics production

- The Asia-Pacific region saw an increase in electrical and electronics production revenue by 13.9% from 2020 to 2021. The electronics sector accounts for 20-50% of the total value of most Asian countries' exports. Consumer electronics such as televisions, radios, computers, and cellular phones are largely manufactured in the ASEAN region.

- ASEAN leads the production of hard drives, with over 80% of hard drives being manufactured in the region. Overall, the electrical and electronics (E&E) industry in ASEAN relies more on foreign inputs and technology than other industries, with 53% of E&E exports arising from foreign value added (FVA) or foreign inputs integrated into ASEAN's E&E exports.

- Countries like Thailand and Malaysia lead in the production of electronics in the region. Thailand, home to one of the largest electronics assembly bases in Southeast Asia, leads in the production of hard drives, integrated circuits, and semiconductors. It ranks second in manufacturing air conditioning units and fourth in the global refrigerators market.

- The electronics industry has greatly benefitted from ASEAN's integrated production networks, which foster improved trade with larger Asian economies like China and Japan.

- China held an 11.2% share of global exports in electrical products and registered a growth of 5.8% in the export of digital products from 2019 to 2020. According to the Asian Development Bank, China provides a large market for electronics in the region. Countries such as Thailand, Japan, China, Malaysia, India, and the Philippines continue to lead the region in the production of electronics.

Asia-Pacific Polycarbonate (PC) Industry Overview

The Asia-Pacific Polycarbonate (PC) Market is moderately consolidated, with the top five companies occupying 59.21%. The major players in this market are Covestro AG, Hainan Huasheng New Material Technology Co., Ltd., Lotte Chemical, Mitsubishi Chemical Corporation and Teijin Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 5000174

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Polycarbonate (PC) Trade

- 4.3 Price Trends

- 4.4 Form Trends

- 4.5 Recycling Overview

- 4.5.1 Polycarbonate (PC) Recycling Trends

- 4.6 Regulatory Framework

- 4.6.1 Australia

- 4.6.2 China

- 4.6.3 India

- 4.6.4 Japan

- 4.6.5 Malaysia

- 4.6.6 South Korea

- 4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Country

- 5.2.1 Australia

- 5.2.2 China

- 5.2.3 India

- 5.2.4 Japan

- 5.2.5 Malaysia

- 5.2.6 South Korea

- 5.2.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 CHIMEI

- 6.4.2 Covestro AG

- 6.4.3 Formosa Plastics Group

- 6.4.4 Hainan Huasheng New Material Technology Co., Ltd.

- 6.4.5 LG Chem

- 6.4.6 Lotte Chemical

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 Sinochem

- 6.4.9 Sinopec SABIC Tianjin Petrochemical Company (SSTPC)

- 6.4.10 Teijin Limited

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.