Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693758

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693758

Europe Biocontrol Agents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 188 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

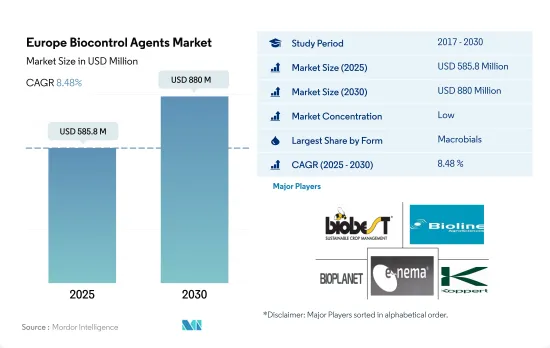

The Europe Biocontrol Agents Market size is estimated at 585.8 million USD in 2025, and is expected to reach 880 million USD by 2030, growing at a CAGR of 8.48% during the forecast period (2025-2030).

- Macrobial biocontrol agents dominate the market, with a value of about USD 458.8 million in 2022. Their dominance is mainly due to their ability to effectively control a wide range of pests without causing harm to the environment.

- Among macrobial biocontrol agents, predators dominate the market and are valued at USD 399.9 million in 2022. The predators' segment's dominance in the overall biocontrol agents market is due to their ability to attack different life stages of pests and even different pest species. They are voracious feeders compared to other biocontrol agents.

- Row crops dominate the macrobial biocontrol agents market, mainly due to their large cultivation area in the region. The consumption value of macrobial biocontrol agents in row crops is anticipated to reach USD 695.3 million by 2029.

- The market share of microbial biocontrol agents is limited compared to macrobial biocontrol agents due to various factors such as limited availability, less awareness about the utilization mechanism among farmers, and complex registration and commercialization processes.

- Bacterial biocontrol agents dominated the microbial market and accounted for about 89.0% of its value in 2022. Bacterial biocontrol agents are mainly dominant due to their ability to control various diseases and pests.

- However, integrated pest management programs promote the use of macrobial biocontrol agents such as predators and parasitoids. The European Commission promotes integrated pest management tools that can assist farmers and advisors, which may drive the macrobial biocontrol agents market value between 2023 and 2029.

- Microorganisms have become an increasingly popular alternative to chemical plant protection products, providing farmers with effective tools to control pests and diseases in their crops while reducing the environmental impact. The European biocontrol agents market witnessed steady growth in 2022 as four legal acts were endorsed by the Member States of the European Commission that simplify the approval and authorization process of microorganism-containing biological plant protection products. The objective is to provide farmers with effective tools to substitute chemical plant protection products and deliver on the objectives of the Farm-to-Fork Strategy.

- Russia currently occupies the largest share in the European biocontrol agents market, with a value share of 55.5% and a volume share of 21.2% in 2022. The increasing cultivation of horticultural crops and the discovery of new pests attacking crops are expected to drive further growth in the Russian market, with a projected CAGR of 8.3% between 2023 and 2029.

- Organic farming is a key industry of the EU agricultural sector, with nearly 330,000 organic farmers in the European Union in 2019, representing up to 20% of the farming area in the Member States. One of the targets of the Farm-to-Fork Strategy is to increase the total farmland under organic farming in the European Union, with plans for at least 25% of the EU's agricultural land to be under organic farming by 2030.

- The new regulations are expected to make it easier for EU organic farmers to access microorganisms used in biological plant protection products. This will provide them with new sustainable alternatives for controlling plant pests, contributing to a more environmentally friendly and sustainable approach to farming.

Europe Biocontrol Agents Market Trends

European green deal is majorly contributing for increasing organic cultivation across the region

- European countries are increasingly promoting organic farming, and the amount of land categorized as organic has significantly increased over the last 10 years. In March 2021, the European Commission launched an organic action plan to achieve the European Green Deal target of ensuring that 25% of agricultural land is under organic farming by 2030. Austria, Italy, Spain, and Germany are among the leading countries for organic cultivation in the European region. Italy has 15.0% of its agricultural area under organic farming, which is higher than the EU average of 7.5%.

- In 2021, organic land in the European Union was recorded at 14.7 million hectares. The agricultural production area is divided into three main types of use: arable land crops (mainly cereals, root crops, and fresh vegetables), permanent grassland, and permanent crops. The area of organic arable land was 6.5 million hectares in 2021, the equivalent of 46% of the European Union's total organic agricultural area.

- The organic cultivation area of cereals, oilseeds, protein crops, and pulses in the European Union increased by 32.6% between 2017 and 2021, amounting to more than 1.6 million hectares. With 1.3 million hectares in production, perennial crops accounted for 15% of the organic land in 2020. Olives, grapes, almonds, and citrus fruits are a few examples of crops in this group. Spain, Italy, and Greece are significant growers of organic olive trees, with 197,000, 179,000, and 47,000 hectares, respectively, in recent years. Both olives and grapes are crucial for the European agricultural industry because they can be turned into specialty products that are in demand locally and globally. The increasing organic acreage in the region is expected to strengthen the organic agricultural industry in Europe.

Growing demand and rising the per capita spending on organic products in the region

- European consumers are increasingly purchasing goods made using natural materials and methods. Even though organic food still only makes up a fraction of the European Union's overall agricultural production, it is no longer a niche industry. The European Union represents the second-largest single market for organic goods internationally, with an average per capita spending of USD 74.8 annually. The per capita spending on organic food in Europe has doubled in the last decade. In 2020, Swiss and Danish consumers spent the most on organic food (USD 494.09 and USD 453.90 per capita, respectively).

- Germany is the largest organic food market in Europe and the second largest market in the world after the United States, with a market size of USD 6.3 billion in 2021 and a per capita consumption of USD 75.6, as per Global Organic Trade data. The country accounted for 10.0% of the global organic food demand and is estimated to record a CAGR of 2.7% between 2021 and 2026.

- The organic food market in France witnessed strong growth, with a 12.6% rise in retail sales in 2021. The country's per capita spending on organic food was recorded at USD 88.8 in 2021, as per Global Organic Trade data. In 2018, as recorded by the Agence BIO/Spirit Insight Barometer, 88% of French people declared having consumed organic products. The preservation of health, environment, and animal welfare are the primary justifications for consuming organic foods in France. The organic market has begun to grow in several other nations, including Spain, the Netherlands, and Sweden, with the opening of organic stores. Organic food sales grew during and post the COVID-19 pandemic as consumers began paying more attention to health issues and learned the adverse effects of conventionally grown food.

Europe Biocontrol Agents Industry Overview

The Europe Biocontrol Agents Market is fragmented, with the top five companies occupying 27.60%. The major players in this market are Biobest Group NV, Bioline AgroSciences Ltd, Bioplanet France, E-NEMA GmbH and Koppert Biological Systems Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 500018

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 Turkey

- 4.3.8 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Macrobials

- 5.1.1.1 By Organism

- 5.1.1.1.1 Entamopathogenic Nematodes

- 5.1.1.1.2 Parasitoids

- 5.1.1.1.3 Predators

- 5.1.2 Microbials

- 5.1.2.1 By Organism

- 5.1.2.1.1 Bacterial Biocontrol Agents

- 5.1.2.1.2 Fungal Biocontrol Agents

- 5.1.2.1.3 Other Microbials

- 5.1.1 Macrobials

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Russia

- 5.3.6 Spain

- 5.3.7 Turkey

- 5.3.8 United Kingdom

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Andermatt Group AG

- 6.4.2 Biobest Group NV

- 6.4.3 Bioline AgroSciences Ltd

- 6.4.4 Bioplanet France

- 6.4.5 Dragonfli

- 6.4.6 E-NEMA GmbH

- 6.4.7 If Tech

- 6.4.8 Koppert Biological Systems Inc.

- 6.4.9 OpenNatur

- 6.4.10 VIRIDAXIS SA

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.